|

市场调查报告书

商品编码

1685124

热水器市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Water Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

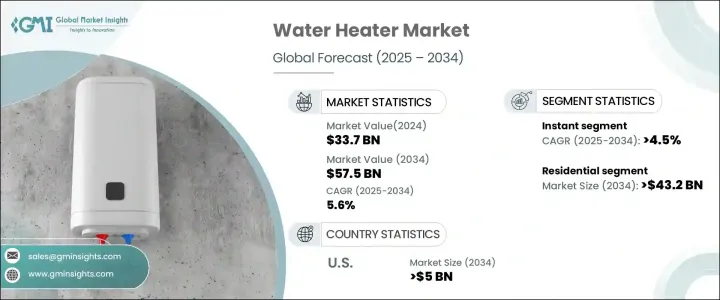

2024 年全球热水器市场规模达到 337 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.6%。作为将水加热到所需温度的必备设备,热水器广泛应用于住宅、商业和工业环境。它们使用电力、天然气、石油或再生能源等能源运作。对节能和永续技术的需求不断增长,推动了市场大幅扩张。消费者越来越重视那些能源消耗最小、碳足迹减少、且符合严格环境法规的产品。随着政府政策和激励措施推动绿色能源解决方案,环保热水器的采用正在加速。

智慧技术整合和自动化正在彻底改变产业,使用户能够透过行动应用程式控制温度设定、监控能源使用情况并优化效率。领先的製造商正在响应这一趋势,开发具有 Wi-Fi 连接、洩漏检测和能源使用追踪等功能的先进热水器。都市化进程的加快,加上可支配所得的增加,也在市场扩张中扮演至关重要的角色。随着房屋自有率的上升,特别是在新兴经济体,对高性能、高性价比的热水解决方案的需求正在激增。此外,永续基础设施和绿色建筑计划的持续推动为製造商创造了丰厚的利润机会。由于高度重视创新、有竞争力的定价和环境责任,全球热水器市场将在未来十年稳步成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 337亿美元 |

| 预测值 | 575亿美元 |

| 复合年增长率 | 5.6% |

预计到 2034 年,住宅领域将创收 432 亿美元,主要得益于新建住宅和装修对节能热水器的需求不断增加。房主正在寻求紧凑、易于安装的系统,能够提供持续的热水且无需过多的能源消耗。随着现代住房的空间限制越来越普遍,消费者开始转向具有高效率和先进控制功能的无水箱和智慧热水器。此外,遵守能源法规和永续性标准的需求促使更多买家选择环保且经济高效的解决方案。

预计到 2034 年,即热式热水器市场将以 4.5% 的复合年增长率扩张,这得益于其紧凑的设计、更长的使用寿命和卓越的能源效率。与传统储水式热水器不同,即热式或无水箱热水器可按需加热水,消除待机热量损失并降低整体能耗。这些加热器在优先考虑空间优化的现代住宅和商业房地产中尤其受欢迎。智慧技术的整合进一步增强了它们的吸引力,使用户能够远端控制温度设定并有效管理能源使用。

随着消费者对绿色认证和节能电器的兴趣日益浓厚,美国热水器市场规模预计到 2034 年将达到 50 亿美元。越来越多的买家愿意对能够长期节能、减少环境影响的热水器进行更高的初始投资。政府激励措施,包括联邦和州退税计划,在推动节能热水系统方面发挥着至关重要的作用。美国能源部(DOE)推出的新效率标准正在进一步加速以现代、高性能替代品取代过时的模型。此外,利用多种能源来优化效率和可靠性的混合热水器的日益普及也促进了市场扩张。

目录

第 1 章:方法论与范围

- 市场定义

- 基础估算与计算

- 预测计算

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 战略仪表板

- 创新与技术格局

- 公司市占率

第 5 章:市场规模及预测:依产品,2021 – 2034 年

- 主要趋势

- 立即的

- 贮存

第六章:市场规模及预测:依产能,2021 – 2034 年

- 主要趋势

- 30公升以下

- 30 – 100 公升

- 100 – 250 公升

- 250 – 400 公升

- >400 公升

第 7 章:市场规模与预测:按应用,2021 – 2034 年

- 主要趋势

- 住宅

- 商业的

- 学院/大学

- 办公室

- 政府/建筑

- 其他的

第 8 章:市场规模与预测:按燃料,2021 – 2034 年

- 主要趋势

- 电的

- 气体

- 天然气

- 液化石油气

第 9 章:市场规模与预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 奥地利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 科威特

- 阿曼

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

- 墨西哥

第十章:公司简介

- AERCO

- AO Smith

- Ariston Holding NV

- Bosch Thermotechnology

- Bradford White Corporation

- GE Appliances

- Groupe Atlantic

- Heatrae Sadia

- Haier

- Havells India

- Jaquar India

- Joven Electric

- Orbital Horizon

- Panasonic Philippines

- Racold

- Rheem Manufacturing Company

- Rinnai Corporation

- Stiebel Eltron

- State Industries

- Thermex Corporation

- Thermann

- Toshiba Lifestyle Products and Services Corporation

- Vaillant Group International

- Viessmann

The Global Water Heater Market reached USD 33.7 billion in 2024 and is projected to grow at a CAGR of 5.6% between 2025 and 2034. As essential appliances for heating water to desired temperatures, water heaters are widely used in residential, commercial, and industrial settings. They operate using energy sources such as electricity, gas, oil, or renewable energies. Rising demand for energy-efficient and sustainable technologies is driving significant market expansion. Consumers are increasingly prioritizing products that minimize energy consumption, reduce carbon footprints, and comply with stringent environmental regulations. With government policies and incentives promoting green energy solutions, the adoption of eco-friendly water heaters is gaining momentum.

Smart technology integration and automation are revolutionizing the industry, allowing users to control temperature settings, monitor energy usage, and optimize efficiency through mobile applications. Leading manufacturers are responding to this trend by developing advanced water heaters with features such as Wi-Fi connectivity, leak detection, and energy usage tracking. The rise in urbanization, coupled with growing disposable income, is also playing a crucial role in market expansion. As homeownership rates rise, particularly in emerging economies, demand for high-performance and cost-effective water heating solutions is surging. Additionally, the ongoing push for sustainable infrastructure and green building initiatives is creating lucrative opportunities for manufacturers. With a strong emphasis on innovation, competitive pricing, and environmental responsibility, the global water heater market is poised for steady growth over the next decade.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $33.7 Billion |

| Forecast Value | $57.5 Billion |

| CAGR | 5.6% |

The residential segment is expected to generate USD 43.2 billion by 2034, fueled by increasing demand for energy-efficient water heaters in new home constructions and renovations. Homeowners are seeking compact, easy-to-install systems that provide continuous hot water without excessive energy consumption. As space constraints become more prevalent in modern housing, consumers are shifting toward tankless and smart water heaters that offer high efficiency and advanced control features. Additionally, the demand for compliance with energy regulations and sustainability standards is leading more buyers to opt for eco-friendly and cost-effective solutions.

The instant water heater segment is projected to expand at a CAGR of 4.5% through 2034, driven by its compact design, longer lifespan, and superior energy efficiency. Unlike traditional storage water heaters, instant or tankless models heat water on demand, eliminating standby heat loss and reducing overall energy consumption. These heaters are particularly popular in modern residential and commercial properties where space optimization is a priority. The integration of smart technology further enhances their appeal, allowing users to control temperature settings remotely and manage energy usage efficiently.

The U.S. water heater market is expected to reach USD 5 billion by 2034, driven by increasing consumer interest in green certifications and energy-efficient appliances. More buyers are willing to make higher initial investments in water heaters that offer long-term energy savings and reduced environmental impact. Government incentives, including federal and state rebate programs, are playing a crucial role in promoting the adoption of energy-efficient water heating systems. New efficiency standards introduced by the U.S. Department of Energy (DOE) are further accelerating the replacement of outdated models with modern, high-performance alternatives. Additionally, the rising popularity of hybrid water heaters, which utilize multiple energy sources to optimize efficiency and reliability, is contributing to the market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

- 4.4 Company market share

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Instant

- 5.3 Storage

Chapter 6 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Below 30 liters

- 6.3 30 – 100 liters

- 6.4 100 – 250 liters

- 6.5 250 – 400 liters

- 6.6 >400 liters

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 Residential

- 7.3 Commercial

- 7.3.1 College/university

- 7.3.2 Offices

- 7.3.3 Government/building

- 7.3.4 Others

Chapter 8 Market Size and Forecast, By Fuel, 2021 – 2034 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 Electric

- 8.3 Gas

- 8.3.1 Natural gas

- 8.3.2 LPG

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 France

- 9.3.3 Germany

- 9.3.4 Italy

- 9.3.5 Austria

- 9.3.6 Spain

- 9.3.7 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Australia

- 9.4.3 India

- 9.4.4 Japan

- 9.4.5 South Korea

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Kuwait

- 9.5.5 Oman

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

- 9.6.3 Chile

- 9.6.4 Mexico

Chapter 10 Company Profiles

- 10.1 AERCO

- 10.2 A. O. Smith

- 10.3 Ariston Holding N.V.

- 10.4 Bosch Thermotechnology

- 10.5 Bradford White Corporation

- 10.6 GE Appliances

- 10.7 Groupe Atlantic

- 10.8 Heatrae Sadia

- 10.9 Haier

- 10.10 Havells India

- 10.11 Jaquar India

- 10.12 Joven Electric

- 10.13 Orbital Horizon

- 10.14 Panasonic Philippines

- 10.15 Racold

- 10.16 Rheem Manufacturing Company

- 10.17 Rinnai Corporation

- 10.18 Stiebel Eltron

- 10.19 State Industries

- 10.20 Thermex Corporation

- 10.21 Thermann

- 10.22 Toshiba Lifestyle Products and Services Corporation

- 10.23 Vaillant Group International

- 10.24 Viessmann

瓦斯热水器市场:依产品类型、技术、燃料类型、安装类型、容量、应用、通路划分,全球预测(2026-2032年)房车无水箱热水器市场按燃料类型、房车类型、安装类型、容量范围、技术类型、销售管道和最终用户划分,全球预测,2026-2032年

瓦斯热水器市场:依产品类型、技术、燃料类型、安装类型、容量、应用、通路划分,全球预测(2026-2032年)房车无水箱热水器市场按燃料类型、房车类型、安装类型、容量范围、技术类型、销售管道和最终用户划分,全球预测,2026-2032年 工业热水器市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型划分房车热水器市场按类型、燃料类型、车辆类型和分销管道划分-2026-2032年全球预测

工业热水器市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、最终用户、功能、安装类型划分房车热水器市场按类型、燃料类型、车辆类型和分销管道划分-2026-2032年全球预测 储水式热水器市场机会、成长要素、产业趋势分析及2026年至2035年预测

储水式热水器市场机会、成长要素、产业趋势分析及2026年至2035年预测 全球热水器市场(2025 年)

全球热水器市场(2025 年) 日本热水器市场规模、份额、趋势及预测(按产品类型、应用和地区划分,2026-2034年)

日本热水器市场规模、份额、趋势及预测(按产品类型、应用和地区划分,2026-2034年) 热水器市场规模、份额和成长分析(按类型、技术、产品类型、容量、应用和地区划分)-2026-2033年产业预测

热水器市场规模、份额和成长分析(按类型、技术、产品类型、容量、应用和地区划分)-2026-2033年产业预测 储水式热水器市场规模、份额和成长分析(按能源来源、水箱容量、材质、最终用户和地区划分)—2026-2033年产业预测

储水式热水器市场规模、份额和成长分析(按能源来源、水箱容量、材质、最终用户和地区划分)—2026-2033年产业预测 瓦斯热水器市场规模、份额及成长分析(按类型、瓦斯类型、点火方式、容量、效率及地区划分)-2026-2033年产业预测

瓦斯热水器市场规模、份额及成长分析(按类型、瓦斯类型、点火方式、容量、效率及地区划分)-2026-2033年产业预测