|

市场调查报告书

商品编码

1685157

自动驾驶汽车市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Autonomous Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

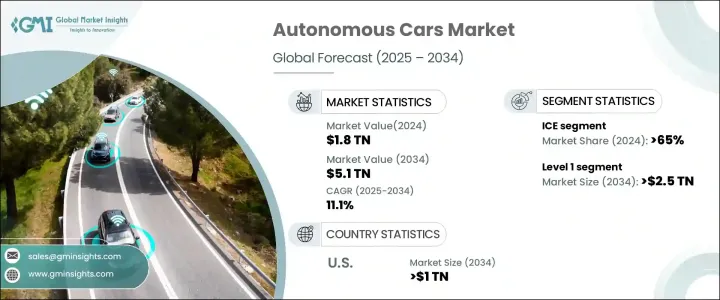

到 2024 年,全球自动驾驶汽车市场规模将达到 1.8 兆美元,预计到 2034 年将以 11.1% 的复合年增长率成长。这一成长主要得益于人工智慧 (AI) 和机器学习的突破,这些突破正在增强汽车的自主性。光达和摄影机等感测器技术的最新进展使得车辆能够更可靠地与周围环境互动,从而增强了消费者对采用自动驾驶汽车的信心。这些技术改进不仅改变了车辆的性能,而且还改善了即时决策,从而增强了安全性并优化了路线效率。随着对连网和自动驾驶汽车的需求不断增长,这些技术对于满足日益增长的消费者兴趣和期望变得至关重要。

促成市场扩张的另一个因素是人们对交通安全的日益重视。自动驾驶汽车旨在减少人为错误,因为人为错误是造成大量道路交通事故的根源。碰撞侦测、自适应巡航控制和自动煞车等自动安全系统的实施提高了安全性并加速了市场的成长。政府和产业机构透过优惠法规支援这些系统的开发和部署,进一步推动市场扩张。随着自动驾驶技术的不断发展,预计它们将对道路安全和效率产生更大的影响。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.8兆美元 |

| 预测值 | 5.1兆美元 |

| 复合年增长率 | 11.1% |

市场按自动化程度细分,包括 1 级、2 级、3 级和 4 级。截至 2024 年,1 级自动化占据超过 55% 的市场份额,预计这一地位将保持到 2034 年,预计价值将超过 2.5 兆美元。这一级别由于其多功能性和成本效益而特别具有吸引力,因为它可以融入到各种各样的车辆中而不需要对基础设施进行重大的改变。车道维持辅助和自适应巡航控制等功能不仅可以提高驾驶者的安全性,还可以满足那些不愿意完全接受自动驾驶系统的消费者的需求。

燃料类型在市场中也发挥着重要作用,其中内燃机 (ICE)、电动和混合动力发动机构成主要部分。 2024年,内燃机汽车占65%以上的市占率。内燃机汽车的广泛使用,加上其相对较低的成本,确保了其在市场上继续占据主导地位。 ICE 汽车与现有的燃料基础设施相容,从而增强了其实用性和对消费者的吸引力。

从地理上看,美国引领北美市场,2024 年占据该地区 90% 以上的份额,预计到 2034 年将超过 1 兆美元。美国是自动驾驶汽车技术的中心,这得益于其强大的技术基础设施和在人工智慧、机器学习和感测器技术方面的大量投资。此外,美国还受益于支持性监管框架,有利于自动驾驶汽车的测试和部署。电动和自动驾驶汽车的强劲需求,加上配套基础设施的快速发展,预计将在未来几年进一步推动市场成长。

目录

第 1 章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估计和计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 供应商概况

- 零件供应商

- 自动驾驶汽车製造商

- 技术提供者

- 经销商

- 最终用户

- 利润率分析

- 价格趋势

- 成本明细

- 技术与创新格局

- 重要新闻及倡议

- 专利分析

- 监管格局

- 衝击力

- 成长动力

- 环保交通方式日益普及

- 自动驾驶汽车新创企业不断壮大

- 北美越来越多地采用自动驾驶技术

- 政府对自动驾驶技术的支援法规

- 产业陷阱与挑战

- 不断提高技术进步

- 自动驾驶汽车初期投资高

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依自主性,2021 - 2034 年

- 主要趋势

- 1级

- 2 级

- 3 级

- 4 级

第六章:市场估计与预测:按燃料,2021 - 2034 年

- 主要趋势

- 冰

- 电的

- 杂交种

第 7 章:市场估计与预测:按最终用途,2021 - 2034 年

- 主要趋势

- 个人的

- 共享出行

第 8 章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东及非洲

- 阿联酋

- 南非

- 沙乌地阿拉伯

第九章:公司简介

- Aptiv

- Aurora Innovation

- Baidu Apollo

- BMW Group

- Ford Motor

- General Motors

- Honda Motor

- Hyundai Motor

- Mercedes-Benz

- Mobileye

- NIO

- Nissan Motor

- Rivian Automotive

- Stellantis NV

- Tesla

- Toyota Motor

- Volkswagen Group

- Volvo Cars

- Waymo

- Zoox

The Global Autonomous Cars Market reached USD 1.8 trillion by 2024 and is anticipated to grow at a CAGR of 11.1% through 2034. This surge is primarily driven by breakthroughs in artificial intelligence (AI) and machine learning, which are enhancing vehicle autonomy. Recent advancements in sensor technologies, such as LiDAR and cameras, have enabled vehicles to interact with their surroundings more reliably, leading to increased consumer confidence in adopting autonomous vehicles. These technological improvements are not only transforming vehicle capabilities but also improving real-time decision-making, which bolsters safety and optimizes routing efficiency. As the demand for connected and autonomous vehicles rises, these technologies are becoming essential to meet the growing consumer interest and expectations.

Another factor contributing to market expansion is the growing emphasis on traffic safety. Autonomous vehicles aim to reduce human error, which is responsible for a significant number of road accidents. The implementation of automated safety systems such as collision detection, adaptive cruise control, and automatic braking enhances safety and accelerates the market's growth. Governments and industry bodies are supporting the development and deployment of these systems through favorable regulations, further fueling market expansion. As autonomous technologies continue to evolve, they are expected to make an even greater impact on road safety and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Trillion |

| Forecast Value | $5.1 Trillion |

| CAGR | 11.1% |

The market is segmented by levels of automation, including Level 1, Level 2, Level 3, and Level 4. As of 2024, Level 1 automation commands over 55% of the market share, a position it is expected to maintain through 2034, with projections to exceed USD 2.5 trillion. This level is particularly attractive due to its versatility and cost-effectiveness, as it can be incorporated into a wide range of vehicles without requiring major infrastructure changes. Features such as lane-keeping assistance and adaptive cruise control not only improve driver safety but also cater to consumers who are hesitant to fully embrace autonomous systems.

Fuel type also plays a significant role in the market, with internal combustion engines (ICE), electric, and hybrid engines making up the major segments. In 2024, ICE vehicles accounted for more than 65% of the market. The widespread use of ICE vehicles, coupled with their relatively lower cost, ensures their continued dominance in the market. ICE vehicles are compatible with existing fuel infrastructure, which enhances their practicality and appeal to consumers.

Geographically, the United States leads the North American market, holding more than 90% of the regional share in 2024, with projections to surpass USD 1 trillion by 2034. The U.S. is a hub for autonomous car technology, thanks to its robust technological infrastructure and significant investments in AI, machine learning, and sensor technologies. Additionally, the U.S. benefits from a supportive regulatory framework that facilitates testing and deployment of autonomous vehicles. The strong demand for electric and self-driving vehicles, coupled with the rapid development of supporting infrastructure, is expected to further drive market growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Autonomous car manufacturers

- 3.2.3 Technology providers

- 3.2.4 Distributors

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Price trend

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Patent analysis

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising adoption of eco-friendly transportation

- 3.10.1.2 Growing autonomous car startups

- 3.10.1.3 Increasing adoption of self-driving technologies in North America

- 3.10.1.4 Supportive government regulations for autonomous driving technology

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Increasing technological advancements

- 3.10.2.2 High initial investments in autonomous cars

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Autonomy, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Level 1

- 5.3 Level 2

- 5.4 Level 3

- 5.5 Level 4

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Personal

- 7.3 Shared mobility

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Aptiv

- 9.2 Aurora Innovation

- 9.3 Baidu Apollo

- 9.4 BMW Group

- 9.5 Ford Motor

- 9.6 General Motors

- 9.7 Honda Motor

- 9.8 Hyundai Motor

- 9.9 Mercedes-Benz

- 9.10 Mobileye

- 9.11 NIO

- 9.12 Nissan Motor

- 9.13 Rivian Automotive

- 9.14 Stellantis N.V.

- 9.15 Tesla

- 9.16 Toyota Motor

- 9.17 Volkswagen Group

- 9.18 Volvo Cars

- 9.19 Waymo

- 9.20 Zoox

自动驾驶汽车软体站市场预测至2032年:按软体类型、车辆类型、自动驾驶等级、部署模式、应用、最终用户和地区分類的全球分析

自动驾驶汽车软体站市场预测至2032年:按软体类型、车辆类型、自动驾驶等级、部署模式、应用、最终用户和地区分類的全球分析 2025年全球自主河川测量船市场报告自动驾驶汽车技术市场预测至2032年:按组件、车辆类型、自动驾驶等级、动力系统、应用、最终用户和地区分類的全球分析

2025年全球自主河川测量船市场报告自动驾驶汽车技术市场预测至2032年:按组件、车辆类型、自动驾驶等级、动力系统、应用、最终用户和地区分類的全球分析 自动驾驶汽车处理器市场:2025-2032年全球预测(按处理器类型、应用、车辆类型和销售管道)自动驾驶汽车市场按组件、自动驾驶等级、燃料类型、技术、应用、车辆类型和最终用户划分-2025-2032年全球预测自动驾驶汽车市场(按车辆类型、系统元件、自主等级、推进力、技术和最终用户划分)—2025-2032 年全球预测

自动驾驶汽车处理器市场:2025-2032年全球预测(按处理器类型、应用、车辆类型和销售管道)自动驾驶汽车市场按组件、自动驾驶等级、燃料类型、技术、应用、车辆类型和最终用户划分-2025-2032年全球预测自动驾驶汽车市场(按车辆类型、系统元件、自主等级、推进力、技术和最终用户划分)—2025-2032 年全球预测 自动驾驶汽车市场-全球产业规模、份额、趋势、机会和预测,按自动化程度、移动性、车辆、地区和竞争情况细分,2020-2030 年预测重型自动驾驶汽车市场:按型号、组件、车辆类型、自动驾驶等级、应用和动力传动系统划分-2025年至2032年全球预测

自动驾驶汽车市场-全球产业规模、份额、趋势、机会和预测,按自动化程度、移动性、车辆、地区和竞争情况细分,2020-2030 年预测重型自动驾驶汽车市场:按型号、组件、车辆类型、自动驾驶等级、应用和动力传动系统划分-2025年至2032年全球预测 自动驾驶晶片市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

自动驾驶晶片市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 自动驾驶汽车的崛起:它将如何影响能源市场?

自动驾驶汽车的崛起:它将如何影响能源市场?