|

市场调查报告书

商品编码

1685190

仪表电缆市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Instrumentation Cable Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

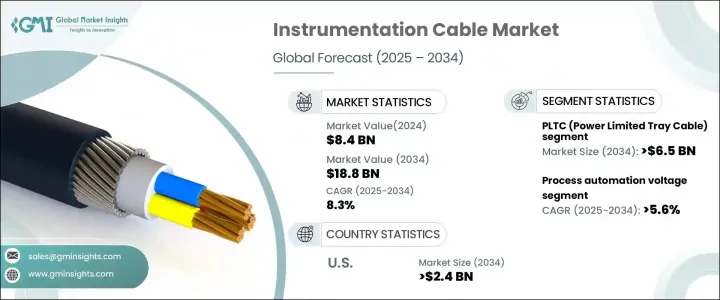

2024 年全球仪器电缆市场价值为 84 亿美元,预计 2025 年至 2034 年的复合年增长率为 8.3%。这一令人印象深刻的扩张归因于工业自动化和製程控制系统对精确讯号传输的需求激增。仪器电缆以其可靠性和效率而闻名,在石油和天然气、发电、製造和再生能源等行业中变得至关重要。这些行业越来越依赖先进的布线解决方案来优化营运、最大限度地减少停机时间并确保在苛刻的条件下实现无缝性能。

此外,全球对再生能源专案和智慧电网基础设施投资的推动进一步推动了对仪器电缆的需求。亚太地区和中东地区的新兴经济体是特别值得关注的市场,这些市场受到重大基础设施发展措施的推动。同时,随着製造商优先考虑环保解决方案(包括低烟、无卤电缆),以满足严格的法规并符合全球永续发展目标,该行业正在经历快速创新。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 84亿美元 |

| 预测值 | 188亿美元 |

| 复合年增长率 | 8.3% |

技术进步正在改变仪器电缆市场,使这些产品更加耐用、紧凑和多功能。这些创新为各产业的扩展应用打开了大门。对基础设施现代化和自动化技术的日益关注进一步加速了市场的成长。在工业环境中,可靠、高效的仪器电缆对于精确传输资料和讯号、确保有效的监控和控制是必不可少的。物联网(IoT)和人工智慧(AI)等尖端技术的整合正在推动对高效能布线系统的大量投资,为长期产业扩张奠定了基础。

按产品类型划分,限功率托盘电缆 (PLTC) 正获得广泛关注,预计到 2034 年将产生 65 亿美元的产值。 PLTC 专为满足限功率电路的需求而设计,可在工业环境中提供卓越的安全性和效能。这些电缆表现出卓越的耐湿气、耐化学品和其他恶劣条件的能力,使其成为关键应用的理想选择。它们严格遵守安全标准,在提高可靠性的同时最大程度地降低了风险,而其简单的安装过程则为大型基础设施专案提供了经济高效的解决方案。

受各行各业自动化技术日益普及的推动,到 2034 年,製程自动化电压领域预计将实现 5.6% 的稳定复合年增长率。这些电缆透过确保无缝监控、控制和资料传输,在维持复杂工业过程中的效率和准确性方面发挥关键作用。随着公司越来越多地实施物联网和人工智慧驱动的解决方案,对可靠仪器电缆的需求正在激增,支援向自动化操作的持续转变。

在美国,随着多个行业广泛采用先进技术,仪器电缆市场预计到 2034 年将达到 24 亿美元。工业和商业应用对高效监控和控制系统的需求不断增长,推动了对高品质布线解决方案的需求。此外,对基础设施升级的大量投资,特别是能源领域的投资,对市场扩张发挥关键作用。这一上升趋势凸显了仪表电缆在支援全球技术进步和现代基础设施发展方面发挥的重要作用。

目录

第 1 章:方法论与范围

- 市场定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 战略仪表板

- 创新与永续发展格局

第 5 章:市场规模及预测:依产品,2021 – 2034 年

- 主要趋势

- PLTC电缆

- ITC电缆

- TC电缆

- 其他的

第 6 章:市场规模与预测:按最终用户,2021 – 2034 年

- 主要趋势

- 石油和天然气

- 化学

- 流程自动化

- 製造业

- 其他的

第 7 章:市场规模及预测:按地区,2021 – 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 义大利

- 俄罗斯

- 西班牙

- 亚太地区

- 中国

- 澳洲

- 印度

- 日本

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 土耳其

- 南非

- 埃及

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- Belden

- CommScope

- Elsewedy Electric

- Fujikura

- Furukawa Electric

- Helukabel

- Hellenic Group

- Kabelwerk Eupen

- Lapp Group

- Leoni

- LS Cable & Systems

- Nexans

- NKT

- Polycab

- Prysmian Group

- Shawcor

- Sumitomo

- Technikabel

- TFKable

The Global Instrumentation Cable Market, valued at USD 8.4 billion in 2024, is poised for robust growth, with a projected CAGR of 8.3% from 2025 to 2034. This impressive expansion is attributed to the surging demand for precise signal transmission in industrial automation and process control systems. Instrumentation cables, known for their reliability and efficiency, are becoming essential in industries such as oil and gas, power generation, manufacturing, and renewable energy. These sectors increasingly rely on advanced cabling solutions to optimize operations, minimize downtime, and ensure seamless performance under demanding conditions.

Moreover, the global push toward renewable energy projects and smart grid infrastructure investments is further driving the demand for instrumentation cables. Emerging economies in Asia-Pacific and the Middle East are particularly noteworthy markets fueled by significant infrastructure development initiatives. Meanwhile, the sector is witnessing rapid innovation as manufacturers prioritize environmentally friendly solutions, including low-smoke, halogen-free cables, to meet stringent regulations and align with global sustainability goals.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $18.8 Billion |

| CAGR | 8.3% |

Technological advancements are transforming the instrumentation cable market, making these products more durable, compact, and versatile. These innovations are opening doors to expanded applications across a variety of industries. The increasing focus on modernizing infrastructure and adopting automation technologies is further accelerating market growth. In industrial settings, reliable and efficient instrumentation cables are indispensable for transmitting data and signals with precision, ensuring effective monitoring and control. The integration of cutting-edge technologies like the Internet of Things (IoT) and artificial intelligence (AI) is driving significant investment in high-performance cabling systems, setting the stage for long-term industry expansion.

By product type, Power Limited Tray Cable (PLTC) is gaining substantial traction and is forecasted to generate USD 6.5 billion by 2034. PLTC is specifically engineered to meet the demands of power-limited circuits, delivering superior safety and performance in industrial environments. These cables exhibit exceptional resistance to moisture, chemicals, and other harsh conditions, making them an ideal choice for critical applications. Their adherence to safety standards enhances reliability while minimizing risks, and their straightforward installation process offers cost-effective solutions for large-scale infrastructure projects.

The process automation voltage segment is projected to experience a steady CAGR of 5.6% through 2034, driven by the growing adoption of automation technologies across industries. These cables play a pivotal role in maintaining efficiency and accuracy in complex industrial processes by ensuring seamless monitoring, control, and data transmission. As companies increasingly implement IoT and AI-driven solutions, the demand for reliable instrumentation cables is skyrocketing, supporting the ongoing shift toward automated operations.

In the United States, the instrumentation cable market is expected to reach USD 2.4 billion by 2034, driven by the widespread adoption of advanced technologies across multiple industries. The rising need for efficient monitoring and control systems in industrial and commercial applications is fueling demand for high-quality cabling solutions. Additionally, significant investments in upgrading infrastructure, particularly within the energy sector, are playing a critical role in the market's expansion. This upward trajectory underscores the instrumental role instrumentation cables play in supporting technological advancement and modern infrastructure development worldwide.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 5.1 Key trends

- 5.2 PLTC cable

- 5.3 ITC cable

- 5.4 TC cable

- 5.5 Others

Chapter 6 Market Size and Forecast, By End User, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 6.1 Key trends

- 6.2 Oil & gas

- 6.3 Chemical

- 6.4 Process automation

- 6.5 Manufacturing

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, ‘000 Tonnes)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Italy

- 7.3.5 Russia

- 7.3.6 Spain

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 India

- 7.4.4 Japan

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Turkey

- 7.5.4 South Africa

- 7.5.5 Egypt

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Belden

- 8.2 CommScope

- 8.3 Elsewedy Electric

- 8.4 Fujikura

- 8.5 Furukawa Electric

- 8.6 Helukabel

- 8.7 Hellenic Group

- 8.8 Kabelwerk Eupen

- 8.9 Lapp Group

- 8.10 Leoni

- 8.11 LS Cable & Systems

- 8.12 Nexans

- 8.13 NKT

- 8.14 Polycab

- 8.15 Prysmian Group

- 8.16 Shawcor

- 8.17 Sumitomo

- 8.18 Technikabel

- 8.19 TFKable