|

市场调查报告书

商品编码

1685205

静电放电封装市场机会、成长动力、产业趋势分析与 2025 - 2034 年预测Electrostatic Discharge Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

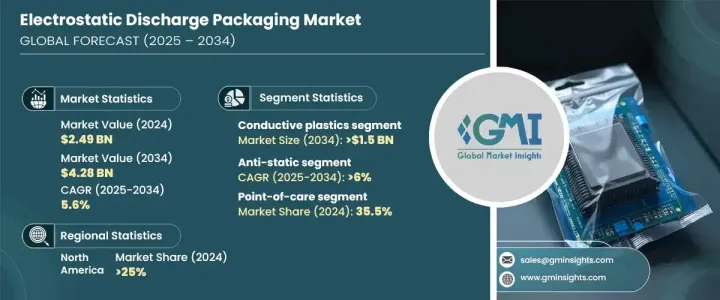

2024 年全球静电放电 (ESD) 封装市场价值为 24.9 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.6%。随着产业更加重视永续性,向环保材料的转变在推动市场成长方面发挥着至关重要的作用。越来越多的公司采用再生材料和资源高效的解决方案来遵守环境法规和企业永续发展目标。对更环保的 ESD 保护产品的需求不断增长,这促进了创新,鼓励了既环保又高效的新包装解决方案。随着技术的快速进步以及保护敏感电子元件免受静电损坏的需求不断增长,ESD 封装市场将在未来十年内大幅扩张。

ESD 包装内的细分市场包括导电塑胶、金属、耗散塑胶和其他材料。特别是导电塑胶领域,预计到 2034 年将达到 15 亿美元。这些材料由注入导电填料的聚合物基物质製成,确保静电保护、耐用性和成本效益的最佳平衡。它们重量轻但坚固,为保护半导体和电子等领域的敏感元件提供了重要解决方案,因为即使是微小的静电放电也可能导致代价高昂的故障。导电塑胶的需求不断增长,证明了其在保护贵重电子产品方面的多功能性和有效性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 24.9 亿美元 |

| 预测值 | 42.8亿美元 |

| 复合年增长率 | 5.6% |

市场也分为防静电、导电和静电耗散类别。防静电领域预计将以最快的速度成长,预计 2025 年至 2034 年的复合年增长率为 6%。防静电材料因其价格低廉和用途广泛而受到青睐,成为多个行业的热门选择。这些材料可以防止静电积聚,这对于包装各种电子元件和消费品至关重要。随着企业不断寻求经济高效、可靠的解决方案来降低静电放电的风险,防静电材料的采用预计将激增。

2024 年,北美占据全球静电放电封装市场的 25%。尤其是美国,对 ESD 封装解决方案的需求显着成长。中国不断扩张的电子、半导体和製造业是这一趋势的主要驱动力。作为全球技术和创新的领导者,美国电子元件的生产和分销量很大,因此需要强有力的 ESD 保护措施。严格的行业法规和对防止静电相关损害的日益关注进一步促进了北美 ESD 包装市场的快速扩张。

目录

第 1 章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第 2 章:执行摘要

第 3 章:产业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 重要新闻及倡议

- 监管格局

- 衝击力

- 成长动力

- 电子产品和零件需求不断成长

- ESD 封装材料的进步

- 更加重视产品保护

- 越来越重视永续环保材料

- 电子商务扩张推动包装需求

- 产业陷阱与挑战

- 先进 ESD 材料成本高昂

- 防静电包装回收基础设施有限

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL 分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第 5 章:市场估计与预测:依材料类型,2021-2034 年

- 主要趋势

- 导电塑料

- 金属

- 耗散塑料

- 其他的

第 6 章:市场估计与预测:按产品类型,2021-2034 年

- 主要趋势

- 袋子和小袋

- 托盘

- 盒子和容器

- 胶带和标籤

- 泡棉

- 其他的

第 7 章:市场估计与预测:依 ESD 分类,2021 年至 2034 年

- 主要趋势

- 防静电

- 静电耗散

- 导电

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 积体电路

- 印刷电路板 (PCB)

- 电动车 (EV) 零件

- 医疗设备

- 航太零件

- 感测器和模组

- 其他的

第 9 章:市场估计与预测:按最终用途产业,2021 年至 2034 年

- 主要趋势

- 航太和国防

- 汽车

- 消费性电子产品

- 卫生保健

- 工业机械

- 半导体

- 其他的

第 10 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 中东及非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- ACL

- Botron Company

- Conductive Containers

- Delphon

- Desco Industries

- Dou Yee Enterprises

- DS Smith

- Elcom

- GWP Conductive

- Indepak

- Nefab Group

- Novapor Hans Lau

- PoliCell

- Protective Packaging

- RS Components and Controls

- Smurfit Kappa

- Statclean Technology

- Swissplast

- Tegatai

- Teknis

- TRICOR

- XpertPack

The Global Electrostatic Discharge (ESD) Packaging Market was valued at USD 2.49 billion in 2024 and is projected to grow at a CAGR of 5.6% from 2025 to 2034. As industries focus more on sustainability, the shift toward eco-friendly materials is playing a crucial role in driving market growth. Companies are increasingly adopting recycled materials and resource-efficient solutions to comply with environmental regulations and corporate sustainability goals. This growing demand for greener ESD protection products is fostering innovation, encouraging new packaging solutions that are both environmentally responsible and highly effective. With the rapid advancements in technology and the rising need to protect sensitive electronic components from static damage, the ESD packaging market is set for significant expansion over the coming decade.

Market segments within ESD packaging include conductive plastics, metal, dissipative plastics, and other materials. The conductive plastics segment, in particular, is expected to reach USD 1.5 billion by 2034. These materials are made from polymer-based substances infused with conductive fillers, ensuring an optimal balance of electrostatic protection, durability, and cost efficiency. They are lightweight yet robust, offering an essential solution for protecting sensitive components in sectors such as semiconductors and electronics, where even a small electrostatic discharge can lead to costly failures. The growing demand for conductive plastics is a testament to their versatility and effectiveness in safeguarding valuable electronics.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.49 Billion |

| Forecast Value | $4.28 Billion |

| CAGR | 5.6% |

The market is also divided into anti-static, conductive, and static dissipative categories. The anti-static segment is expected to grow at the fastest rate, with a projected CAGR of 6% from 2025 to 2034. Anti-static materials are favored for their affordability and versatility, making them a popular choice across multiple industries. These materials prevent static buildup, which is essential for packaging a wide range of electronic components and consumer goods. As businesses continue to look for cost-effective, reliable solutions to mitigate the risks of electrostatic discharge, the adoption of anti-static materials is expected to surge.

North America held a 25% share of the global electrostatic discharge packaging market in 2024. The United States, in particular, is experiencing significant growth in demand for ESD packaging solutions. The country's expanding electronics, semiconductor, and manufacturing industries are key drivers of this trend. As a global leader in technology and innovation, the U.S. has high production and distribution volumes of electronic components, necessitating robust ESD protection measures. Stringent industry regulations and an increasing focus on preventing static-related damage are further contributing to the rapid expansion of the ESD packaging market in North America.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2022-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Key news & initiatives

- 3.3 Regulatory landscape

- 3.4 Impact forces

- 3.4.1 Growth drivers

- 3.4.1.1 Rising demand for electronics and components

- 3.4.1.2 Advancements in ESD packaging materials

- 3.4.1.3 Increased focus on product protection

- 3.4.1.4 Increasing emphasis on sustainable and eco-friendly materials

- 3.4.1.5 Expansion of e-commerce drives packaging needs

- 3.4.2 Industry pitfalls & challenges

- 3.4.2.1 High costs of advanced ESD materials

- 3.4.2.2 Limited recycling infrastructure for ESD packaging

- 3.4.1 Growth drivers

- 3.5 Growth potential analysis

- 3.6 Porter’s analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Million & Kilo Tons)

- 5.1 Key trends

- 5.2 Conductive plastics

- 5.3 Metal

- 5.4 Dissipative plastics

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Million & Kilo Tons)

- 6.1 Key trends

- 6.2 Bags and pouches

- 6.3 Trays

- 6.4 Boxes and containers

- 6.5 Tapes and labels

- 6.6 Foams

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By ESD Classification, 2021-2034 (USD Million & Kilo Tons)

- 7.1 Key trends

- 7.2 Anti-static

- 7.3 Static dissipative

- 7.4 Conductive

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Million & Kilo Tons)

- 8.1 Key trends

- 8.2 Integrated circuits

- 8.3 Printed circuit boards (PCBs)

- 8.4 Electric vehicle (EV) components

- 8.5 Medical devices

- 8.6 Aerospace components

- 8.7 Sensors and modules

- 8.8 Others

Chapter 9 Market Estimates & Forecast, By End Use Industry, 2021-2034 (USD Million & Kilo Tons)

- 9.1 Key trends

- 9.2 Aerospace and defense

- 9.3 Automotive

- 9.4 Consumer electronics

- 9.5 Healthcare

- 9.6 Industrial machinery

- 9.7 Semiconductors

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million & Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ACL

- 11.2 Botron Company

- 11.3 Conductive Containers

- 11.4 Delphon

- 11.5 Desco Industries

- 11.6 Dou Yee Enterprises

- 11.7 DS Smith

- 11.8 Elcom

- 11.9 GWP Conductive

- 11.10 Indepak

- 11.11 Nefab Group

- 11.12 Novapor Hans Lau

- 11.13 PoliCell

- 11.14 Protective Packaging

- 11.15 RS Components and Controls

- 11.16 Smurfit Kappa

- 11.17 Statclean Technology

- 11.18 Swissplast

- 11.19 Tegatai

- 11.20 Teknis

- 11.21 TRICOR

- 11.22 XpertPack