|

市场调查报告书

商品编码

1698569

电动车充电站市场机会、成长动力、产业趋势分析及 2025-2034 年预测Electric Vehicle Charging Station Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

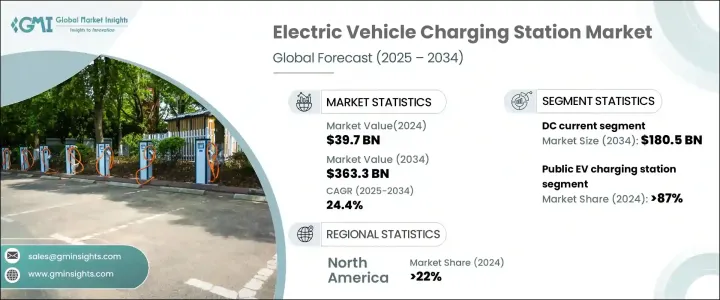

2024 年全球电动车充电站市场规模达 397 亿美元,预计 2025 年至 2034 年的复合年增长率为 24.4%。电动车的快速普及、政府的支持性政策以及充电技术的进步是这项成长的主要驱动力。对快速充电基础设施的需求不断增长,促使汽车製造商和能源供应商合作建造大规模充电网路。

世界各国政府正在扩大激励措施和补贴以加速部署。监管倡议正在透过强制要求广泛建设充电基础设施来塑造该行业。物联网和人工智慧的融合优化了负载管理并增强了电网整合。然而,由于不同地区的收费标准和协议不同,互通性仍然是一项重大挑战。该行业也正在向再生能源整合转变,许多充电站都采用太阳能和电池储存来提高永续性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 397亿美元 |

| 预测值 | 3633亿美元 |

| 复合年增长率 | 24.4% |

电动车充电站市场规模在 2022 年为 257 亿美元,2023 年为 307 亿美元,2024 年将达到 397 亿美元。该领域包括交流充电和直流充电,其中直流充电占据主导地位,预计到 2034 年将超过 1805 亿美元。向直流快速充电的转变正在加速,尤其是在商业和高速公路应用领域。这些充电器大大缩短了充电时间,使其成为长途旅行和商业车队的理想选择。然而,由于昂贵的设备、先进的电网整合和基础设施要求,部署直流快速充电器的高成本仍然是一个障碍。单一直流快速充电站的预计投资额在 62,160 美元至 248,640 美元之间。

交流充电虽然速度较慢,但由于价格低廉且广泛可用,对于住宅和工作场所使用仍然至关重要。大约 80% 的电动车充电都在家中进行,因此交流充电器对于日常通勤至关重要。 1级和2级交流充电器广泛应用于家庭、办公室和公共区域。公共交流充电站必须满足 7.4 kW 的最低输出功率要求。

2024 年,公共充电站占据了超过 87% 的市场份额,预计到 2034 年将以每年超过 26% 的速度成长。扩建工作主要集中在城市地区、高速公路和商业中心,以支援日益增长的电动车队。近年来,充电桩安装数量激增,缓解了里程焦虑,方便了长途旅行。公共充电基础设施的融资格局正在发生变化,政府和私人实体都投入了大量资金。美国政府承诺投入 50 亿美元,在 2026 年扩大电动车充电基础设施。

儘管取得了这些进步,但挑战依然存在,包括高昂的安装成本、土地征用费用以及电网容量限制。快速充电站的安装成本在 20,836 美元到 104,180 美元之间。由于成本效益,住宅和工作场所充电仍然是首选,家庭充电比公共充电站便宜 50%。持续的技术进步,包括自动计费、智慧电网整合和互通性要求,将提高电动车充电网路的效率。到 2025 年,所有公共充电站都必须遵守互通性法规,确保电动车用户的无缝存取。

2024 年,北美占据了超过 22% 的市场收入,预计到 2034 年将进一步增加。美国电动车充电站市场规模从 2022 年的 4 亿美元成长到 2023 年的 5 亿美元,再到 2024 年达到 7 亿美元。联邦和州一级的资助计划正在推动这一增长。国家电动车基础设施公式计划拨款 50 亿美元,用于在所有州建立互联充电网路。美国政府承诺投入 75 亿美元在全国建设 50 万个充电桩的电动车充电基础设施,确保为电动车用户提供强大且可存取的网路。

目录

第一章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依当前,2021 – 2034 年

- 主要趋势

- 交流电

- 1级

- 2级

- 直流

- 直流快速

- 其他的

第六章:市场规模及预测:依充电站点划分,2021 年至 2034 年

- 主要趋势

- 民众

- 私人的

第七章:市场规模及预测:依地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 挪威

- 德国

- 法国

- 荷兰

- 英国

- 瑞典

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 新加坡

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- ABB

- Blink Charging

- CHAEVI

- ChargePoint

- Delta Electronics

- Eaton

- Elli

- EVBox

- GreenWay Infrastructure

- Hyundai Motor

- Leviton Manufacturing

- NIO

- Nissan Motor

- Schneider Electric

- Siemens

- SK Signet

- Tesla

- VinFast

- Volta

- Zunder

The Global Electric Vehicle Charging Station Market reached USD 39.7 billion in 2024 and is projected to grow at a CAGR of 24.4% from 2025 to 2034. The rapid adoption of electric vehicles, supportive government policies, and advancements in charging technologies are key drivers of this growth. Increasing demand for fast-charging infrastructure is prompting automakers and energy providers to collaborate on large-scale charging networks.

Governments worldwide are expanding incentives and subsidies to accelerate deployment. Regulatory initiatives are shaping the industry by mandating widespread charging infrastructure. The integration of IoT and artificial intelligence optimizes load management and enhances grid integration. However, interoperability remains a significant challenge due to diverse charging standards and protocols across different regions. The industry is also shifting toward renewable energy integration, with many charging stations incorporating solar power and battery storage to improve sustainability.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39.7 Billion |

| Forecast Value | $363.3 Billion |

| CAGR | 24.4% |

The market for electric vehicle charging stations stood at USD 25.7 billion in 2022 and USD 30.7 billion in 2023 before reaching USD 39.7 billion in 2024. The segment includes AC and DC charging, with DC charging dominating the market and expected to surpass USD 180.5 billion by 2034. The transition toward DC fast charging is accelerating, particularly in commercial and highway applications. These chargers significantly reduce charging time, making them ideal for long-distance travel and commercial fleets. However, the high cost of deploying DC fast chargers remains a barrier due to expensive equipment, advanced grid integration, and infrastructure requirements. The estimated investment for a single DC fast charging station ranges between USD 62,160 and USD 248,640.

AC charging, while slower, remains crucial for residential and workplace use due to affordability and widespread availability. Approximately 80% of electric vehicle charging occurs at home, making AC chargers essential for daily commuting. Level 1 and Level 2 AC chargers are widely used in households, offices, and public areas. Public AC charging stations must meet a minimum output power requirement of 7.4 kW.

Public charging stations accounted for over 87% of the market share in 2024 and are expected to grow at more than 26% annually until 2034. Expansion efforts are particularly focused on urban areas, highways, and commercial centers to support the increasing EV fleet. Charging point installations have surged in recent years, alleviating range anxiety and facilitating long-distance travel. The funding landscape for public charging infrastructure is evolving, with significant investments from both governments and private entities. The U.S. government has committed USD 5 billion to expand EV charging infrastructure through 2026.

Despite these advancements, challenges persist, including high installation costs, land acquisition expenses, and grid capacity limitations. Installation costs for fast-charging stations vary between USD 20,836 and USD 104,180. Residential and workplace charging remains the preferred choice due to cost-effectiveness, with home charging being up to 50% cheaper than public stations. Ongoing technological advancements, including automated billing, smart grid integration, and interoperability requirements, will enhance the efficiency of EV charging networks. By 2025, all public charging stations will be required to comply with interoperability regulations, ensuring seamless access for EV users.

North America held over 22% of the market revenue in 2024, with its share expected to increase further by 2034. The U.S. EV charging station market grew from USD 400 million in 2022 to USD 500 million in 2023 and USD 700 million in 2024. Federal and state-level funding initiatives are fueling this growth. The National Electric Vehicle Infrastructure Formula Program allocates USD 5 billion to develop an interconnected charging network across all states. The U.S. government has committed USD 7.5 billion to building a nationwide EV charging infrastructure of 500,000 chargers, ensuring a robust and accessible network for electric vehicle users.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Current, 2021 – 2034 (Units, USD Billion)

- 5.1 Key trends

- 5.2 AC

- 5.2.1 Level 1

- 5.2.2 Level 2

- 5.3 DC

- 5.3.1 DC Fast

- 5.3.2 Others

Chapter 6 Market Size and Forecast, By Charging Site, 2021 – 2034 (Units, USD Billion)

- 6.1 Key trends

- 6.2 Public

- 6.3 Private

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (Units, USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Norway

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Netherlands

- 7.3.5 UK

- 7.3.6 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 India

- 7.4.4 South Korea

- 7.4.5 Singapore

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Blink Charging

- 8.3 CHAEVI

- 8.4 ChargePoint

- 8.5 Delta Electronics

- 8.6 Eaton

- 8.7 Elli

- 8.8 EVBox

- 8.9 GreenWay Infrastructure

- 8.10 Hyundai Motor

- 8.11 Leviton Manufacturing

- 8.12 NIO

- 8.13 Nissan Motor

- 8.14 Schneider Electric

- 8.15 Siemens

- 8.16 SK Signet

- 8.17 Tesla

- 8.18 VinFast

- 8.19 Volta

- 8.20 Zunder

电动车充电站能源基础设施市场规模、份额和成长分析(按充电器类型、应用、连接器类型、充电等级和地区划分)-2026-2033年产业预测

电动车充电站能源基础设施市场规模、份额和成长分析(按充电器类型、应用、连接器类型、充电等级和地区划分)-2026-2033年产业预测 2025年全球储能充电能源管理平台市场报告

2025年全球储能充电能源管理平台市场报告 电动车充电站原料市场:依材料种类、充电站类型、功率等级、应用、国家及地区划分-全球产业分析、市场规模、市场份额及2025-2032年预测

电动车充电站原料市场:依材料种类、充电站类型、功率等级、应用、国家及地区划分-全球产业分析、市场规模、市场份额及2025-2032年预测 液冷式电动车充电线缆市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

液冷式电动车充电线缆市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 动态电动车充电网路市场预测至2032年:按充电技术、车辆类型、部署环境、基础设施所有权模式、功率等级和区域分類的全球分析电动车充电站市场预测至2032年:按充电器类型、充电等级、连接器类型、安装类型、充电模式、最终用户和地区分類的全球分析2032 年超快速电动车充电市场预测:按充电标准、部署模式、安装类型、技术、应用、最终用户和地区进行的全球分析

动态电动车充电网路市场预测至2032年:按充电技术、车辆类型、部署环境、基础设施所有权模式、功率等级和区域分類的全球分析电动车充电站市场预测至2032年:按充电器类型、充电等级、连接器类型、安装类型、充电模式、最终用户和地区分類的全球分析2032 年超快速电动车充电市场预测:按充电标准、部署模式、安装类型、技术、应用、最终用户和地区进行的全球分析 商用车辆充电站市场按车辆类型、充电器输出功率、充电技术、终端用户产业和所有权类型划分-2025-2032年全球预测2032 年电动车充电站设备市场预测:按充电站类型、功率输出、组件、安装类型、供应商类型、连接器类型、最终用户和地区进行的全球分析电动车充电站市场(按充电类型、连接器类型、营运、经营模式和最终用途)—2025-2030 年全球预测

商用车辆充电站市场按车辆类型、充电器输出功率、充电技术、终端用户产业和所有权类型划分-2025-2032年全球预测2032 年电动车充电站设备市场预测:按充电站类型、功率输出、组件、安装类型、供应商类型、连接器类型、最终用户和地区进行的全球分析电动车充电站市场(按充电类型、连接器类型、营运、经营模式和最终用途)—2025-2030 年全球预测