|

市场调查报告书

商品编码

1699239

车辆健康监测市场机会、成长动力、产业趋势分析及 2025-2034 年预测Vehicle Health Monitoring Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

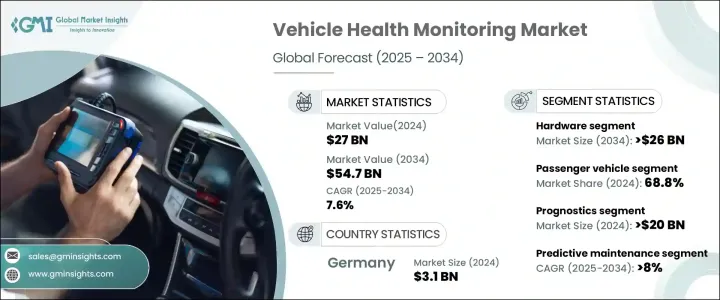

2024 年全球车辆健康监测市场价值为 270 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 7.6%。即时诊断工具的采用率不断提高、物联网感测器、远端资讯处理和人工智慧驱动的分析技术的进步正在推动市场成长。这些技术增强了车辆监控,改善了预测性维护,并减少了意外故障。车辆健康监测系统持续评估引擎、变速箱、煞车和电池等关键零件,确保最佳性能并防止故障。

云端运算和边缘处理可以为驾驶员、车队营运商和服务供应商提供即时资料回馈,从而提高车辆可靠性并最大限度地减少故障。连网和自动驾驶汽车的日益普及进一步推动了对先进诊断的需求。汽车製造商和科技公司正在整合人工智慧预测分析、远端诊断和 OTA(无线)更新,以优化车辆维护。即时监控电池电量可提高能源效率并延长电池寿命。政府强制实施车载诊断 (OBD) 和排放监测的政策进一步刺激了对车辆健康监测解决方案的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 270亿美元 |

| 预测值 | 547亿美元 |

| 复合年增长率 | 7.6% |

即时诊断在预测性维护、最大限度地减少车队停机时间和改善路线管理方面发挥着至关重要的作用。这些技术与商业车队营运的整合正在改变远端资讯处理行业。保险公司也利用车辆健康资料进行基于使用情况的保险(UBI),根据驾驶行为和车辆状况调整保费。人工智慧和 5G 网路的发展有望提高车辆的安全性、效率并节省营运成本。

车辆健康监测市场分为硬体、软体解决方案和服务。硬体部分占了超过 50% 的市场份额,预计到 2034 年将超过 260 亿美元。此部分包括感测器、GPS 和 OBD 端口,用于捕获车辆资料以优化性能。感测器监测引擎温度、轮胎压力、燃料消耗和排放,而 GPS 增强车队跟踪,OBD 端口实现远端诊断。车辆自动化和连接性的不断提高正在推动对先进硬体解决方案的需求。政府规定透过 OBD 进行排放监测,进一步鼓励汽车製造商为车辆配备高精度感测器和诊断系统。

市场也按车辆类型分类,包括乘用车和商用车。 2024 年,乘用车占据了 68.8% 的市场份额,而商用车则因客製化维修服务需求的不断增长而显着增长。

根据健康管理,市场分为诊断和预测。预测领域在 2024 年将达到 200 多亿美元,占据领先地位。汽车製造商和车队营运商越来越多地采用预测解决方案,这些解决方案使用即时资料分析来提前预测故障。现代车辆配备了基于云端的分析、支援物联网的感测器和数位孪生技术,用于监控关键系统。 5G与边缘运算的结合,进一步提高了诊断的准确性和效率。与传统的维护检查不同,预测系统分析即时感测器资料和人工智慧模型,以检测组件退化的早期迹象,从而及时采取维护措施。

市场根据应用细分为预测性维护、道路救援、即时车辆诊断、排放监测、车队管理以及车辆安全保障。预计预测期内预测性维护的最高复合年增长率将超过 8%。人工智慧、物联网和即时资料运算正在推动预测性维护解决方案的发展,使感测器能够持续追踪车辆的重要部件。透过分析即时资料和维护历史,预测性维护解决方案可以减少停机时间和维修成本。边缘运算和基于云端的分析的采用进一步提高了这些系统的效率。汽车製造商和车队营运商越来越多地使用预测性维护来提高车辆性能和耐用性,同时最大限度地降低营运费用。

2024 年,德国引领欧洲车辆健康监测市场,创造约 31 亿美元的收入。该国在物联网预测、基于人工智慧的诊断和智慧车辆健康监测系统方面处于领先地位。凭藉强大的研发投入和智慧汽车技术的快速应用,德国仍然是塑造连网汽车诊断未来的关键参与者。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 零件供应商

- 技术提供者

- 系统整合商

- 最终用途景观

- 配销通路分析

- 利润率分析

- 供应商格局

- 技术与创新格局

- 专利分析

- 监管格局

- 成本細項分析

- 案例研究

- 衝击力

- 成长动力

- 全球电动车采用趋势的转变

- 北美和欧洲商用车需求增加

- 亚太地区网路普及率和智慧型手机连线率不断提高

- 拉丁美洲对乘用车的需求很高

- 产业陷阱与挑战

- 与车辆健康监测系统相关的网路安全威胁

- 缺乏互联基础设施

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 感应器

- GPS 系统

- OBD埠

- 其他的

- 软体

- 服务

- 维护和维修服务

- 咨询与整合服务

第六章:市场估计与预测:按健康管理,2021 - 2034 年

- 主要趋势

- 预测

- 诊断

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型商用车(LCV)

- 重型商用车(HCV)

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 预测性维护

- 即时车辆诊断

- 道路救援

- 排放监测

- 车队管理

- 车辆安全与保障

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 西班牙

- 义大利

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第十章:公司简介

- Bosch

- Car Media Lab

- Continental

- Delphi

- Denso

- Garrett Advancing Motion

- Harman International

- Intangles Lab

- Intellicar

- iotaSmart Labs

- KPIT Technologies

- Luxoft

- Octo Group

- Onstar

- Taabi

- TATA Elxsi

- Vector Informatik

- Visteon

- ZF Friedrichshafen

- Zubie

The Global Vehicle Health Monitoring Market was valued at USD 27 billion in 2024 and is projected to expand at a CAGR of 7.6% from 2025 to 2034. Increasing adoption of real-time diagnostic tools, advancements in IoT sensors, telematics, and AI-driven analytics are driving market growth. These technologies enhance vehicle monitoring, improve predictive maintenance, and reduce unexpected failures. Vehicle health monitoring systems continuously assess key components such as the engine, transmission, brakes, and battery, ensuring optimal performance and preventing malfunctions.

Cloud computing and edge processing enable real-time data feedback for drivers, fleet operators, and service providers, enhancing vehicle reliability and minimizing breakdowns. The increasing deployment of connected and autonomous vehicles further boosts demand for advanced diagnostics. Automakers and tech firms are integrating AI-powered predictive analytics, remote diagnostics, and OTA (over-the-air) updates to optimize vehicle maintenance. Monitoring battery charge levels in real time enhances energy efficiency and extends battery life. Government policies mandating real-time On-Board Diagnostics (OBD) and emissions monitoring further fuel demand for vehicle health monitoring solutions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $27 Billion |

| Forecast Value | $54.7 Billion |

| CAGR | 7.6% |

Real-time diagnostics play a crucial role in predictive maintenance, minimizing fleet downtime and improving route management. The integration of these technologies into commercial fleet operations is transforming the telematics industry. Insurance companies are also leveraging vehicle health data for usage-based insurance (UBI), adjusting premiums based on driving behavior and vehicle condition. The evolution of AI and 5G networks is expected to enhance vehicle safety, efficiency, and operational cost savings.

The vehicle health monitoring market is segmented into hardware, software solutions, and services. The hardware segment captured over 50% of the market share and is projected to exceed USD 26 billion by 2034. This segment includes sensors, GPS, and OBD ports, which capture vehicle data to optimize performance. Sensors monitor engine temperature, tire pressure, fuel consumption, and emissions, while GPS enhances fleet tracking and OBD ports enable remote diagnostics. The increasing automation and connectivity of vehicles are driving demand for advanced hardware solutions. Government regulations mandating emission monitoring through OBD further encourage automakers to equip vehicles with high-precision sensors and diagnostic systems.

The market is also categorized by vehicle type, including passenger and commercial vehicles. Passenger vehicles held a 68.8% market share in 2024, while commercial vehicles are seeing significant growth due to rising demand for tailored maintenance services.

Based on health management, the market is divided into diagnostics and prognostics. The prognostics segment led with over USD 20 billion in 2024. Automakers and fleet operators are increasingly adopting prognostic solutions, which use real-time data analytics to predict malfunctions in advance. Modern vehicles are equipped with cloud-based analytics, IoT-enabled sensors, and digital twin technology for monitoring critical systems. The integration of 5G with edge computing is further refining diagnostic accuracy and efficiency. Unlike traditional maintenance inspections, prognostic systems analyze real-time sensor data and AI models to detect early signs of component degradation, enabling timely maintenance actions.

The market is segmented by application into predictive maintenance, roadside assistance, real-time vehicle diagnostics, emission monitoring, fleet management, and vehicle safety and security. Predictive maintenance is expected to register the highest CAGR of over 8% during the forecast period. AI, IoT, and real-time data computing are advancing predictive maintenance solutions, allowing sensors to continuously track essential vehicle components. By analyzing real-time data and maintenance history, predictive maintenance solutions reduce downtime and repair costs. The adoption of edge computing and cloud-based analytics further enhances the efficiency of these systems. Automakers and fleet operators are increasingly using predictive maintenance to improve vehicle performance and durability while minimizing operational expenses.

Germany led the European vehicle health monitoring market in 2024, generating around USD 3.1 billion in revenue. The country is at the forefront of IoT-enabled prognostics, AI-based diagnostics, and smart vehicle health monitoring systems. With strong R&D investments and rapid adoption of intelligent vehicle technologies, Germany remains a key player in shaping the future of connected car diagnostics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Component suppliers

- 3.1.1.2 Technology providers

- 3.1.1.3 System integrators

- 3.1.1.4 End use landscape

- 3.1.1.5 Distribution channel analysis

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Case study

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Shifting trends towards adoption of electric vehicles across the globe

- 3.7.1.2 Increase in the demand for commercial vehicles in North America and Europe

- 3.7.1.3 Growing internet penetration and smart phone connectivity in Asia Pacific

- 3.7.1.4 High demand for passenger cars in Latin America

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Cyber security threats related to vehicle health monitoring systems

- 3.7.2.2 Lack of connected infrastructure

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 GPS systems

- 5.2.3 OBD port

- 5.2.4 Others

- 5.3 Software

- 5.4 Services

- 5.4.1 Maintenance & repair services

- 5.4.2 Consulting & integration services

Chapter 6 Market Estimates & Forecast, By Health Management, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Prognostics

- 6.3 Diagnostics

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light commercial vehicles (LCV)

- 7.3.2 Heavy commercial vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Predictive maintenance

- 8.3 Real-time vehicle diagnostics

- 8.4 Roadside assistance

- 8.5 Emission monitoring

- 8.6 Fleet management

- 8.7 Vehicle safety & security

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Bosch

- 10.2 Car Media Lab

- 10.3 Continental

- 10.4 Delphi

- 10.5 Denso

- 10.6 Garrett Advancing Motion

- 10.7 Harman International

- 10.8 Intangles Lab

- 10.9 Intellicar

- 10.10 iotaSmart Labs

- 10.11 KPIT Technologies

- 10.12 Luxoft

- 10.13 Octo Group

- 10.14 Onstar

- 10.15 Taabi

- 10.16 TATA Elxsi

- 10.17 Vector Informatik

- 10.18 Visteon

- 10.19 ZF Friedrichshafen

- 10.20 Zubie

汽车主动健康监测系统市场:2026-2032年全球市场预测(按车辆类型、系统类型、销售管道、应用和最终用户划分)

汽车主动健康监测系统市场:2026-2032年全球市场预测(按车辆类型、系统类型、销售管道、应用和最终用户划分) 2026年全球汽车主动健康监测系统市场报告胎压监测系统(TPMS)轮胎压力感知器晶片市场按类型、应用、车辆类型和通讯频率划分,全球预测(2026-2032年)

2026年全球汽车主动健康监测系统市场报告胎压监测系统(TPMS)轮胎压力感知器晶片市场按类型、应用、车辆类型和通讯频率划分,全球预测(2026-2032年) 汽车主动健康监测系统市场规模、份额和成长分析(按系统位置、组件、车辆类型、部署类型、应用和地区划分)-2026-2033年产业预测

汽车主动健康监测系统市场规模、份额和成长分析(按系统位置、组件、车辆类型、部署类型、应用和地区划分)-2026-2033年产业预测 车载健康监测系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

车载健康监测系统市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 全球综合车辆健康管理市场规模、份额及产业分析报告(按通路、产品、最终用途、应用、区域展望及预测,2025 - 2032 年)

全球综合车辆健康管理市场规模、份额及产业分析报告(按通路、产品、最终用途、应用、区域展望及预测,2025 - 2032 年) 综合车辆健康管理市场规模、份额、趋势分析报告:按产品、通路、最终用途、应用、地区、细分市场预测,2025 年至 2030 年综合车辆健康管理 (IVHM) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

综合车辆健康管理市场规模、份额、趋势分析报告:按产品、通路、最终用途、应用、地区、细分市场预测,2025 年至 2030 年综合车辆健康管理 (IVHM) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 汽车用活性健康监控系统的全球市场:产业分析,规模,占有率,成长,趋势,预测(2025年~2032年)

汽车用活性健康监控系统的全球市场:产业分析,规模,占有率,成长,趋势,预测(2025年~2032年) 汽车主动健康监测系统市场 - 全球规模、份额、趋势分析、机会、预测,2019-2030

汽车主动健康监测系统市场 - 全球规模、份额、趋势分析、机会、预测,2019-2030