|

市场调查报告书

商品编码

1699247

智慧交通市场机会、成长动力、产业趋势分析及 2025-2034 年预测Smart Transportation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

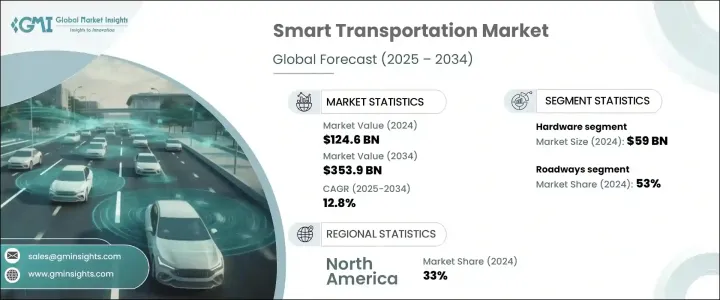

2024 年全球智慧交通市场价值为 1,246 亿美元,预计 2025 年至 2034 年的复合年增长率为 12.8%。随着全球各个城市都在寻求先进的移动解决方案以减少延误、降低排放并提高整体运输效率,快速的城市化和日益严重的交通拥堵是推动市场扩张的关键因素。连网和自动驾驶汽车 (CAV) 的日益普及正在显着影响市场成长,人工智慧、物联网和 5G 等技术在即时交通管理和车对万物 (V2X) 通讯中发挥着至关重要的作用。

这些进步有助于优化道路安全、简化交通流量并透过与智慧城市基础设施结合来增强交通网路。政府和交通部门正在大力投资智慧交通系统 (ITS),支援智慧讯号、自动收费和车辆追踪等措施。随着自动驾驶和电动车变得越来越主流,对人工智慧移动解决方案的需求持续上升,从而加强了智慧交通产业的扩张。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1246亿美元 |

| 预测值 | 3539亿美元 |

| 复合年增长率 | 12.8% |

市场根据组件分为硬体、软体和服务。硬体产业在 2024 年处于领先地位,创造了 590 亿美元的收入,预计在预测期内的复合年增长率约为 13.2%。关键硬体元素包括 GPS、物联网感测器、RFID 晶片、监视摄影机、自动售检票系统和 V2X 通讯设备。这些技术对于即时交通监控、连网汽车系统和智慧交通解决方案至关重要。对城市交通嵌入式系统的投资,包括电子收费和人工智慧驱动的交通管理,进一步加强了对硬体解决方案的需求。

根据运输方式,市场分为公路运输、铁路运输、航空运输和海运。 2024 年,公路占了 53% 的市场份额,预计到 2034 年将以超过 13% 的复合年增长率成长。不断扩大的城市道路网络以及电动和自动驾驶汽车的日益普及,正在推动对先进交通控制和预测系统的需求。叫车服务和共享出行平台也在加速智慧道路解决方案的发展,促进该产业的发展。

在解决方案方面,市场细分为交通管理、智慧票务、停车管理、乘客资讯系统和货运管理。由于道路上车辆数量的增加、城市交通拥堵的加剧以及对有效移动解决方案的需求,交通管理领域占据主导地位。正在实施人工智慧驱动的交通管制、自适应号誌和拥塞收费策略,以优化道路性能,同时最大限度地减少延误和环境影响。即时交通追踪、自动事件侦测和预测分析进一步提高了道路安全性和效率。

从地区来看,北美在 2024 年占据市场主导地位,占全球份额的 33% 左右,创造了 420 亿美元的收入。美国仍处于领先地位,强而有力的政府措施、技术进步和城市发展推动市场扩张。促进 ITS、互联移动和人工智慧交通解决方案的联邦资助计画和政策正在加速各大都会区智慧交通基础设施的采用。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场估计的主要趋势

- 预测模型

- 初步研究与验证

- 主要来源

- 资料探勘来源

- 市场定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 技术提供者

- 系统整合商

- 交通基础设施提供者

- 汽车和车辆製造商

- 数据和服务提供者

- 利润率分析

- 技术与创新格局

- 专利分析

- 用例

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 全球都市化进程加快,交通壅塞加剧

- 对高效率、永续交通运输的需求不断增长

- 物联网、人工智慧和巨量资料分析的技术进步

- 政府措施和投资不断增加

- 对连网和自动驾驶汽车的需求不断增长

- 产业陷阱与挑战

- 初期投资成本高

- 资料隐私和安全问题

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 感应器

- 相机

- RFID 晶片

- GPS 装置

- 其他的

- 软体

- 交通管理系统

- 车队管理软体

- 其他的

- 服务

- 咨询

- 部署与集成

- 支援与维护

第六章:市场估计与预测:依运输方式,2021 - 2034 年

- 主要趋势

- 道路

- 铁路

- 航空

- 海上

第七章:市场估计与预测:按解决方案,2021 - 2034 年

- 主要趋势

- 交通管理

- 智慧票务

- 停车管理

- 乘客资讯系统

- 货运管理

第八章:市场估计与预测:依技术分类,2021 - 2034 年

- 主要趋势

- 物联网

- 人工智慧与机器学习

- 巨量资料分析

- 云端运算

- 区块链

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 政府机构

- 商业企业

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Alstom

- Bentley

- Cisco

- Conduent

- Cubic

- Hitachi

- Huawei Technologies

- IBM

- Indra Sistema

- Kapsch TrafficCom

- Lyft

- NEC

- Qualcomm

- Robert Bosch

- SAP

- Siemens Mobility

- Thales

- TomTom

- Trimble

- Uber Technologies

The Global Smart Transportation Market was valued at USD 124.6 billion in 2024 and is expected to grow at a CAGR of 12.8% from 2025 to 2034. Rapid urbanization and rising traffic congestion are key factors driving market expansion as cities worldwide seek advanced mobility solutions to reduce delays, lower emissions, and enhance overall transportation efficiency. The growing adoption of connected and autonomous vehicles (CAVs) is significantly influencing market growth, with technologies like AI, IoT, and 5G playing a crucial role in real-time traffic management and vehicle-to-everything (V2X) communication.

These advancements help optimize road safety, streamline traffic flow, and enhance transport networks by integrating with smart city infrastructure. Governments and transport authorities are heavily investing in intelligent transportation systems (ITS), supporting initiatives such as smart signals, automated tolling, and vehicle tracking. As self-driving and electric vehicles become more mainstream, demand for AI-powered mobility solutions continues to rise, reinforcing the expansion of the smart transportation industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $124.6 Billion |

| Forecast Value | $353.9 Billion |

| CAGR | 12.8% |

The market is segmented based on components into hardware, software, and services. The hardware segment led in 2024, generating USD 59 billion in revenue, and is projected to grow at a CAGR of approximately 13.2% during the forecast period. Key hardware elements include GPS, IoT sensors, RFID chips, surveillance cameras, automated fare collection systems, and V2X communication devices. These technologies are critical for real-time traffic monitoring, connected vehicle systems, and intelligent transport solutions. Investment in embedded systems for urban mobility, including electronic toll collection and AI-driven traffic management, is further strengthening the demand for hardware solutions.

By transportation mode, the market is divided into roadways, railways, airways, and maritime. Roadways accounted for 53% of the market share in 2024 and are anticipated to grow at a CAGR of over 13% through 2034. Expanding urban road networks and the increasing adoption of electric and autonomous vehicles are boosting the need for advanced traffic control and forecasting systems. Ride-hailing services and shared mobility platforms are also accelerating the development of smart roadway solutions, contributing to the sector's growth.

In terms of solutions, the market is segmented into traffic management, smart ticketing, parking management, passenger information systems, and freight management. The traffic management segment dominates due to the rising number of vehicles on roads, increasing urban congestion, and the need for effective mobility solutions. AI-driven traffic control, adaptive signaling, and congestion pricing strategies are being implemented to optimize road performance while minimizing delays and environmental impact. Real-time traffic tracking, automatic incident detection, and predictive analytics are further enhancing road safety and efficiency.

Regionally, North America led the market in 2024, accounting for around 33% of the global share and generating USD 42 billion in revenue. The United States remains at the forefront, with strong government initiatives, technological advancements, and urban development fueling market expansion. Federal funding programs and policies promoting ITS, connected mobility, and AI-powered transportation solutions are accelerating the adoption of smart transport infrastructure across major metropolitan areas.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Technology providers

- 3.2.2 System integrators

- 3.2.3 Transportation infrastructure providers

- 3.2.4 Automotive & vehicle manufacturers

- 3.2.5 Data & service providers

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Use cases

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rapid urbanization and congestion in cities across the world

- 3.9.1.2 Growing demand for efficient and sustainable transportation

- 3.9.1.3 Technological advancements in IoT, AI, and big data analytics

- 3.9.1.4 Rising government initiatives and investments

- 3.9.1.5 Growing demand for connected and autonomous vehicles

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial investment costs

- 3.9.2.2 Data privacy and security concerns

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.2.1 Sensors

- 5.2.2 Cameras

- 5.2.3 RFID chips

- 5.2.4 GPS device

- 5.2.5 Others

- 5.3 Software

- 5.3.1 Traffic management systems

- 5.3.2 Fleet management software

- 5.3.3 Others

- 5.4 Services

- 5.4.1 Consulting

- 5.4.2 Deployment & integration

- 5.4.3 Support & maintenance

Chapter 6 Market Estimates & Forecast, By Transportation Mode, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Roadways

- 6.3 Railways

- 6.4 Airways

- 6.5 Maritime

Chapter 7 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Traffic management

- 7.3 Smart ticketing

- 7.4 Parking management

- 7.5 Passenger information systems

- 7.6 Freight management

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 IoT

- 8.3 AI & machine learning

- 8.4 Big data analytics

- 8.5 Cloud computing

- 8.6 Blockchain

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 Government agencies

- 9.3 Commercial businesses

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Alstom

- 11.2 Bentley

- 11.3 Cisco

- 11.4 Conduent

- 11.5 Cubic

- 11.6 Hitachi

- 11.7 Huawei Technologies

- 11.8 IBM

- 11.9 Indra Sistema

- 11.10 Kapsch TrafficCom

- 11.11 Lyft

- 11.12 NEC

- 11.13 Qualcomm

- 11.14 Robert Bosch

- 11.15 SAP

- 11.16 Siemens Mobility

- 11.17 Thales

- 11.18 TomTom

- 11.19 Trimble

- 11.20 Uber Technologies

全球智慧交通市场规模、份额、趋势和成长分析报告(2026-2034)

全球智慧交通市场规模、份额、趋势和成长分析报告(2026-2034) 智慧交通市场-全球产业规模、份额、趋势、机会及预测(依应用、产品类型、地区及竞争格局划分,2021-2031年)

智慧交通市场-全球产业规模、份额、趋势、机会及预测(依应用、产品类型、地区及竞争格局划分,2021-2031年) 2026-2030年全球智慧交通市场

2026-2030年全球智慧交通市场 日本智慧交通市场规模、份额、趋势及预测(按解决方案和服务、交通方式、应用和地区划分),2026-2034年

日本智慧交通市场规模、份额、趋势及预测(按解决方案和服务、交通方式、应用和地区划分),2026-2034年 智慧交通市场规模、份额和成长分析(按交通方式、技术、连接技术、部署方式、应用、最终用户和地区划分)-2026-2033年产业预测

智慧交通市场规模、份额和成长分析(按交通方式、技术、连接技术、部署方式、应用、最终用户和地区划分)-2026-2033年产业预测 智慧交通:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

智慧交通:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 全球智慧运输市场(2025-2030年):依技术、解决方案类型、运输方式、商业模式和车辆类型

全球智慧运输市场(2025-2030年):依技术、解决方案类型、运输方式、商业模式和车辆类型 智慧交通市场按模式、最终用户和地区划分 - 预测至 2029 年

智慧交通市场按模式、最终用户和地区划分 - 预测至 2029 年 智慧交通技术:各种技术与市场

智慧交通技术:各种技术与市场