|

市场调查报告书

商品编码

1699297

宠物配件市场机会、成长动力、产业趋势分析及 2025-2034 年预测Pet Accessories Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

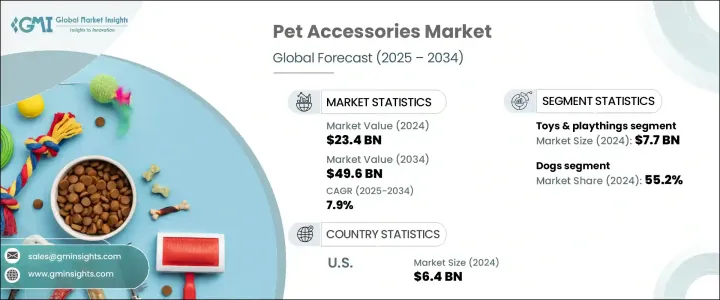

2024 年全球宠物配件市场规模达到 234 亿美元,预计 2025 年至 2034 年的复合年增长率将达到 7.9%。市场成长的动力包括宠物拥有量的增加、消费者对高端产品的支出增加以及将宠物视为家庭成员的转变。宠物主人优先考虑高品质、注重健康且创新的配件,以提高宠物的舒适度、安全性和整体健康。永续和环保产品越来越受到青睐,反映出消费者越来越倾向于选择对环境负责的产品。随着科技越来越融入宠物照护日常,对智慧宠物配件(包括 GPS 项圈、自动餵食器和健康监测设备)的需求也不断增长。

此外,宠物主人越来越被符合他们个人生活方式偏好的可客製化且美观的配件所吸引。推动这一快速扩张的因素包括消费者偏好的不断变化、宠物产品的高端化以及推广时尚和实用的宠物配件的社交媒体趋势的日益增强的影响力。各大品牌正利用这一趋势,推出以设计师宠物服装、豪华宠物床和手工美容必需品为特色的高端系列产品。直接面向消费者 (DTC) 品牌的兴起进一步改变了市场,实现了个人化产品供应和基于订阅的模式,以满足寻求便利性和独特性的宠物主人的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 234亿美元 |

| 预测值 | 496亿美元 |

| 复合年增长率 | 7.9% |

该行业根据宠物类型分为狗、猫、鸟、鱼和水生宠物、爬行动物等。 2024 年,狗类市场占据了 55.2% 的份额,预计 2025 年至 2034 年期间的复合年增长率为 8.1%。随着宠物收养率的提高和人们对犬类健康意识的增强,对高级项圈、牵引绳、服装和美容必需品等配件的需求不断增长。主人优先考虑注重健康的产品,包括矫形床、宠物健身追踪器以及旨在延长寿命和增强活力的营养补充剂。

根据产品类型,市场包括服装和服饰、床和家具、玩具和玩物、美容产品、餵食和饮水配件、健康和保健产品等。 2024 年,玩具和玩乐类别的估值达到 77 亿美元,位居榜首,预计 2025 年至 2034 年期间的复合年增长率为 8.3%。製造商正在推出支持宠物智力刺激和身体参与的互动和认知玩具,以满足消费者对宠物丰富化日益增长的关注。人们对宠物心理健康的认识不断提高,加剧了对先进且引人入胜的产品的需求。

2024 年美国宠物配件市场价值为 64 亿美元,预计在整个预测期内复合年增长率为 8.4%。受生活方式的改变和电子商务的兴起的影响,城市市场的购买行为正在转变。可支配收入的增加和对高品质、耐用产品的偏好正在推动市场成长。消费者越来越倾向于永续的高科技宠物护理解决方案,环保材料和智慧配件塑造了行业趋势。网上购物的便利,加上专业宠物零售商的不断涌现,进一步加速了美国各地对优质宠物配件的采用

目录

第一章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 技术概述

- 监管格局

- 衝击力

- 成长动力

- 宠物主人数量不断增加

- 宠物人性化趋势日益明显

- 消费者在宠物照护方面的支出增加

- 产业陷阱与挑战

- 宠物服装和配件的季节性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 服饰

- 毛衣

- T恤

- 夹克

- 其他(雨衣、靴子等)

- 床和家具

- 宠物床

- 沙发

- 其他(沙发、垫子等)

- 玩具和玩物

- 咀嚼玩具

- 球

- 绒毛玩具

- 其他(拼图等)

- 餵食及饮水配件

- 碗

- 自动餵食器

- 饮水机

- 其他(餵食垫、食物储存容器等)

- 美容产品

- 刷子

- 碗

- 洗髮精

- 其他(指甲刀、牙齿护理产品等)

- 健康与保健产品

- 补充品

- 维生素

- 镇静剂

- 其他(蜱虫控制产品等)

- 其他(训练和行为配件、身份标籤和宠物安全配件等)

第六章:市场估计与预测:依宠物类型,2021-2034

- 主要趋势

- 狗

- 猫

- 鸟类

- 鱼类和水生宠物

- 爬虫类

- 其他(哺乳动物、兔子、仓鼠等)

第七章:市场估计与预测:依价格区间,2021-2034

- 主要趋势

- 低的

- 中等的

- 高的

第八章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 在线的

- 电子商务

- 公司网站

- 离线

- 超市和大卖场

- 宠物专卖店

- 其他零售商店(宠物医院等)

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

- MEA 其余地区

第十章:公司简介

- Central Garden & Pet Company

- Coastal Pet Products, Inc.

- Ferplast SpA

- Hartz Mountain Corporation

- Jollyes Pet Superstores

- KONG Company

- Merrick Pet Care, Inc.

- MidWest Homes for Pets

- Nestlé Purina PetCare

- Pets at Home Group Plc

The Global Pet Accessories Market reached USD 23.4 billion in 2024 and is projected to expand at a CAGR of 7.9% from 2025 to 2034. The market growth is driven by increasing pet ownership, rising consumer spending on premium products, and a shift toward treating pets as family members. Pet owners are prioritizing high-quality, health-focused, and innovative accessories that enhance their pets' comfort, safety, and overall well-being. Sustainable and eco-friendly products are gaining traction, reflecting a broader consumer shift toward environmentally responsible choices. The demand for smart pet accessories, including GPS-enabled collars, automated feeders, and health monitoring devices, is also on the rise as technology becomes more integrated into pet care routines.

Additionally, pet parents are increasingly drawn to customizable and aesthetically appealing accessories that align with their personal lifestyle preferences. The rapid expansion is fueled by evolving consumer preferences, the premiumization of pet products, and the increasing influence of social media trends that promote stylish and functional pet accessories. Brands are capitalizing on this trend by launching high-end collections featuring designer pet apparel, luxury pet beds, and artisanal grooming essentials. The rise of direct-to-consumer (DTC) brands has further transformed the market, enabling personalized product offerings and subscription-based models that cater to pet owners seeking convenience and exclusivity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.4 Billion |

| Forecast Value | $49.6 Billion |

| CAGR | 7.9% |

The industry is segmented by pet type into dogs, cats, birds, fish and aquatic pets, reptiles, and others. The dogs segment held a 55.2% share in 2024 and is anticipated to grow at a CAGR of 8.1% between 2025 and 2034. Increased pet adoption and heightened awareness of canine well-being are driving demand for accessories such as premium collars, leashes, clothing, and grooming essentials. Owners are prioritizing health-conscious products, including orthopedic beds, pet fitness trackers, and nutritional supplements designed to enhance longevity and vitality.

By product type, the market includes apparel and clothing, beds and furniture, toys and playthings, grooming products, feeding and drinking accessories, health and wellness products, and others. In 2024, the toys and playthings category led with a valuation of USD 7.7 billion and is projected to register a CAGR of 8.3% between 2025 and 2034. Manufacturers are introducing interactive and cognitive playthings that support pets' mental stimulation and physical engagement, catering to a growing consumer focus on pet enrichment. The increasing awareness of pets' psychological well-being has intensified the demand for advanced and engaging products.

The U.S. pet accessories market was worth USD 6.4 billion in 2024 and is anticipated to grow at a CAGR of 8.4% throughout the forecast period. Urban markets are witnessing a shift in purchasing behaviors influenced by evolving lifestyles and the surge of e-commerce. Expanding disposable incomes and a preference for high-quality, durable products are propelling market growth. Consumers are gravitating toward sustainable, high-tech pet care solutions, with eco-friendly materials and smart accessories shaping industry trends. The convenience of online shopping, coupled with the growing presence of specialized pet retailers, is further accelerating the adoption of premium pet accessories across the U.S.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factors affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technological overview

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing number of pet owners

- 3.6.1.2 Growing trend of pet humanization

- 3.6.1.3 Higher consumer spending on pet care

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Seasonality in pet clothing & accessories

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2023

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Apparel and clothing

- 5.2.1 Sweaters

- 5.2.2 T-shirts

- 5.2.3 Jackets

- 5.2.4 Others (raincoats, boots, etc.)

- 5.3 Beds and furniture

- 5.3.1 Pet beds

- 5.3.2 Sofas

- 5.3.3 Others (couches, cushions, etc.)

- 5.4 Toys and playthings

- 5.4.1 Chew toys

- 5.4.2 Balls

- 5.4.3 Plush toys

- 5.4.4 Others (puzzles, etc.)

- 5.5 Feeding and drinking accessories

- 5.5.1 Bowls

- 5.5.2 Automatic feeders

- 5.5.3 Water dispensers

- 5.5.4 Others (feeding mats, food storage containers, etc.)

- 5.6 Grooming products

- 5.6.1 Brushes

- 5.6.2 Bowls

- 5.6.3 Shampoo

- 5.6.4 Others (nail clippers, dental care products, etc.)

- 5.7 Health and wellness products

- 5.7.1 Supplements

- 5.7.2 Vitamins

- 5.7.3 Calming aids

- 5.7.4 Others (tick control products, etc.)

- 5.8 Others (training and behavior accessories, ID tags and pet safety accessories, etc.)

Chapter 6 Market Estimates & Forecast, By Pet type, 2021-2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Dogs

- 6.3 Cats

- 6.4 Birds

- 6.5 Fish & aquatic pets

- 6.6 Reptiles

- 6.7 Others (mammals, rabbits, hamsters, etc.)

Chapter 7 Market Estimates & Forecast, By Price range, 2021-2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Low

- 7.3 Medium

- 7.4 High

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Online

- 8.2.1 E-commerce

- 8.2.2 Company website

- 8.3 Offline

- 8.3.1 Supermarkets and hypermarkets

- 8.3.2 Pet specialty stores

- 8.3.3 Other retail stores (pet hospitals, etc.)

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

- 9.6.4 Rest of MEA

Chapter 10 Company Profiles

- 10.1 Central Garden & Pet Company

- 10.2 Coastal Pet Products, Inc.

- 10.3 Ferplast S.p.A.

- 10.4 Hartz Mountain Corporation

- 10.5 Jollyes Pet Superstores

- 10.6 KONG Company

- 10.7 Merrick Pet Care, Inc.

- 10.8 MidWest Homes for Pets

- 10.9 Nestlé Purina PetCare

- 10.10 Pets at Home Group Plc