|

市场调查报告书

商品编码

1699330

冷凝食品加工锅炉市场机会、成长动力、产业趋势分析及 2025-2034 年预测Condensing Food Processing Boiler Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

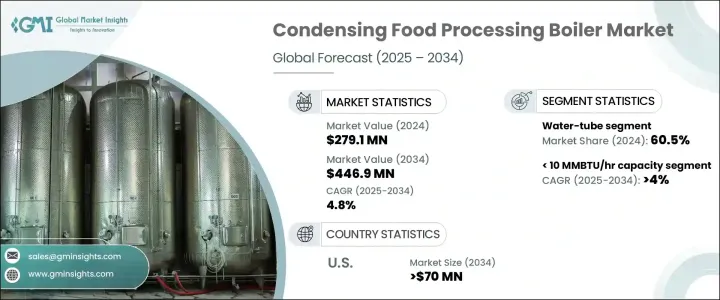

全球冷凝食品加工锅炉市场在 2024 年的价值为 2.791 亿美元,预计在 2025 年至 2034 年期间将以 4.8% 的复合年增长率扩张,这得益于对能源效率、可持续性和严格的监管要求的日益重视。随着工业化、城市化进程加快以及消费者对包装和加工食品的需求不断增长,食品加工行业正在经历快速转型。随着製造商优先考虑营运效率和减少碳足迹,冷凝锅炉正在成为首选的加热解决方案,提供卓越的热效率,同时最大限度地减少排放。

暖气技术的进步和智慧控制系统的整合进一步增强了这些锅炉的吸引力,实现了精确的温度调节和优化的燃料消耗。政府推行的清洁能源使用政策和对节能工业设备的财政激励措施也促进了市场扩张。此外,食品加工厂的持续现代化,特别是在新兴经济体,正在为市场参与者创造有利可图的机会。对永续性的高度关注,加上节能供暖系统的长期成本效益,正在推动更多公司投资冷凝锅炉。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 2.791亿美元 |

| 预测值 | 4.469亿美元 |

| 复合年增长率 | 4.8% |

市场依产品类型分为火管锅炉和水管锅炉。 2024年水管锅炉占据产业主导地位,占总收入的60.5%。它们的需求不断增长,与自动化和大容量食品加工系统的日益普及有关,而这些系统需要先进的蒸汽生成能力。向现代化製造设施的转变,加上消费者饮食习惯的不断变化,推动了食品生产工厂采用高效的加热解决方案。此外,严格的食品安全法规要求稳定可靠的蒸汽供应,促使製造商选择高性能冷凝锅炉,以提高生产率并满足合规标准。

根据燃料类型,冷凝食品加工锅炉市场分为天然气、石油、煤炭和其他。受天然气基础设施扩张、锅炉效率技术创新以及对环保替代品日益增长的青睐的推动,天然气市场规模预计到 2034 年将达到 1.5 亿美元。天然气锅炉能够稳定地生产蒸汽和热水,同时降低营运成本,因此成为食品加工设施的理想选择。随着能源法规的收紧,向清洁燃料的转变正在加速,进一步推动市场成长。

在美国,冷凝式食品加工锅炉市场在 2024 年创造了 4,530 万美元的产值,预计到 2034 年将达到 7,000 万美元。这一增长主要得益于职业安全与健康管理局 (OSHA) 和环境保护署 (EPA) 等机构实施的严格排放法规。这些法规鼓励食品加工产业采用先进的低排放加热系统。随着合规要求越来越严格,食品製造商正在转向高效冷凝锅炉,以满足环境标准,同时确保最佳生产效率。随着技术的不断进步和监管压力的不断增加,未来几年市场将稳步扩张。

目录

第一章:方法论与范围

- 市场范围和定义

- 市场估计和预测参数

- 预测计算

- 资料来源

- 基本的

- 次要

- 有薪资的

- 民众

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略展望

- 创新与永续发展格局

第五章:市场规模及预测:依产能,2021 年至 2034 年

- 主要趋势

- < 10 百万英热单位/小时

- 10 - 25 百万英热单位/小时

- 25 - 50 百万英热单位/小时

- 50 - 75 百万英热单位/小时

- 75 - 100 百万英热单位/小时

- 100 - 175 百万英热单位/小时

- 175 - 250 百万英热单位/小时

- > 250 百万英热单位/小时

第六章:市场规模及预测:依产品,2021 年至 2034 年

- 主要趋势

- 火管

- 水管

第七章:市场规模及预测:依燃料,2021 年至 2034 年

- 主要趋势

- 天然气

- 油

- 煤炭

- 其他的

第八章:市场规模及预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 法国

- 英国

- 波兰

- 义大利

- 西班牙

- 奥地利

- 德国

- 瑞典

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 菲律宾

- 日本

- 韩国

- 澳洲

- 印尼

- 中东和非洲

- 沙乌地阿拉伯

- 伊朗

- 阿联酋

- 奈及利亚

- 南非

- 拉丁美洲

- 阿根廷

- 智利

- 巴西

第九章:公司简介

- ALFA LAVAL

- Babcock & Wilcox Enterprises

- Babcock Wanson

- BM GreenTech

- Bosch Industriekessel

- Clayton Industries

- Cleaver-Brooks

- Cochran

- Forbes Marshall

- Hurst Boiler

- Miura America

- Rentech Boiler Systems

- Thermax

- Thermodyne Boilers

- Viessmann

The Global Condensing Food Processing Boiler Market, valued at USD 279.1 million in 2024, is projected to expand at a CAGR of 4.8% between 2025 and 2034, driven by a rising emphasis on energy efficiency, sustainability, and stringent regulatory requirements. The food processing sector is witnessing a rapid transformation, fueled by increasing industrialization, urbanization, and growing consumer demand for packaged and processed foods. As manufacturers prioritize operational efficiency and carbon footprint reduction, condensing boilers are emerging as a preferred heating solution, delivering superior thermal efficiency while minimizing emissions.

Advancements in heating technology and the integration of smart control systems further enhance the appeal of these boilers, enabling precise temperature regulation and optimized fuel consumption. Government policies promoting cleaner energy adoption and financial incentives for energy-efficient industrial equipment are also contributing to market expansion. In addition, the ongoing modernization of food processing plants, particularly in emerging economies, is creating lucrative opportunities for market players. The heightened focus on sustainability, coupled with the long-term cost benefits of energy-efficient heating systems, is pushing more companies to invest in condensing boilers.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $279.1 Million |

| Forecast Value | $446.9 Million |

| CAGR | 4.8% |

The market is segmented by product type into fire-tube and water-tube boilers. Water-tube boilers dominated the industry in 2024, accounting for 60.5% of total revenue. Their rising demand is linked to the increased adoption of automated and high-capacity food processing systems, which require advanced steam generation capabilities. The shift toward modernized manufacturing facilities, coupled with evolving consumer eating habits, is fueling the adoption of efficient heating solutions across food production plants. Additionally, strict food safety regulations necessitate consistent and reliable steam supply, prompting manufacturers to opt for high-performance condensing boilers that enhance productivity while meeting compliance standards.

Based on fuel type, the condensing food processing boiler market is categorized into natural gas, oil, coal, and others. The natural gas segment is projected to reach USD 150 million by 2034, driven by expanding gas infrastructure, technological innovations in boiler efficiency, and the rising preference for eco-friendly alternatives. Natural gas boilers offer consistent steam and hot water production with reduced operational costs, making them an attractive choice for food processing facilities. As energy regulations tighten, the transition toward cleaner-burning fuels is accelerating, further propelling market growth.

In the United States, the condensing food processing boiler market generated USD 45.3 million in 2024 and is expected to reach USD 70 million by 2034. This growth is primarily supported by stringent emissions regulations imposed by agencies such as the Occupational Safety and Health Administration (OSHA) and the Environmental Protection Agency (EPA). These regulations encourage the adoption of advanced, low-emission heating systems across the food processing sector. As compliance requirements become more rigorous, food manufacturers are transitioning to high-efficiency condensing boilers to meet environmental standards while ensuring optimal production efficiency. With ongoing technological advancements and increasing regulatory pressure, the market is set to witness steady expansion in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million, MMBTU/hr & Units)

- 5.1 Key trends

- 5.2 < 10 MMBTU/hr

- 5.3 10 - 25 MMBTU/hr

- 5.4 25 - 50 MMBTU/hr

- 5.5 50 - 75 MMBTU/hr

- 5.6 75 - 100 MMBTU/hr

- 5.7 100 - 175 MMBTU/hr

- 5.8 175 - 250 MMBTU/hr

- 5.9 > 250 MMBTU/hr

Chapter 6 Market Size and Forecast, By Product, 2021 – 2034 (USD Million, MMBTU/hr & Units)

- 6.1 Key trends

- 6.2 Fire-tube

- 6.3 Water-tube

Chapter 7 Market Size and Forecast, By Fuel, 2021 – 2034 (USD Million, MMBTU/hr & Units)

- 7.1 Key trends

- 7.2 Natural gas

- 7.3 Oil

- 7.4 Coal

- 7.5 Others

Chapter 8 Market Size and Forecast, By Region, 2021 – 2034 (USD Million, MMBTU/hr & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.2.3 Mexico

- 8.3 Europe

- 8.3.1 France

- 8.3.2 UK

- 8.3.3 Poland

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Austria

- 8.3.7 Germany

- 8.3.8 Sweden

- 8.3.9 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Philippines

- 8.4.4 Japan

- 8.4.5 South Korea

- 8.4.6 Australia

- 8.4.7 Indonesia

- 8.5 Middle East & Africa

- 8.5.1 Saudi Arabia

- 8.5.2 Iran

- 8.5.3 UAE

- 8.5.4 Nigeria

- 8.5.5 South Africa

- 8.6 Latin America

- 8.6.1 Argentina

- 8.6.2 Chile

- 8.6.3 Brazil

Chapter 9 Company Profiles

- 9.1 ALFA LAVAL

- 9.2 Babcock & Wilcox Enterprises

- 9.3 Babcock Wanson

- 9.4 BM GreenTech

- 9.5 Bosch Industriekessel

- 9.6 Clayton Industries

- 9.7 Cleaver-Brooks

- 9.8 Cochran

- 9.9 Forbes Marshall

- 9.10 Hurst Boiler

- 9.11 Miura America

- 9.12 Rentech Boiler Systems

- 9.13 Thermax

- 9.14 Thermodyne Boilers

- 9.15 Viessmann

全球瓦斯食品加工锅炉市场全球食品加工锅炉市场火管食品加工锅炉的全球市场瓦斯火管食品加工锅炉的全球市场全球冷凝式食品加工锅炉市场全球冷凝管状食品加工锅炉市场

全球瓦斯食品加工锅炉市场全球食品加工锅炉市场火管食品加工锅炉的全球市场瓦斯火管食品加工锅炉的全球市场全球冷凝式食品加工锅炉市场全球冷凝管状食品加工锅炉市场 冷凝火管食品加工锅炉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

冷凝火管食品加工锅炉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 火管食品加工锅炉市场 - 全球产业规模、份额、趋势、机会和预测,按燃料类型、应用、行业垂直、压力、地区、竞争进行细分,2020-2030 年冷凝式食品加工工业用热水锅炉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测燃气水管食品加工锅炉市场机会、成长动力、产业趋势分析与预测 2025 - 2034

火管食品加工锅炉市场 - 全球产业规模、份额、趋势、机会和预测,按燃料类型、应用、行业垂直、压力、地区、竞争进行细分,2020-2030 年冷凝式食品加工工业用热水锅炉市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测燃气水管食品加工锅炉市场机会、成长动力、产业趋势分析与预测 2025 - 2034