|

市场调查报告书

商品编码

1699343

机器人软体市场机会、成长动力、产业趋势分析及 2025-2034 年预测Robotic Software Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

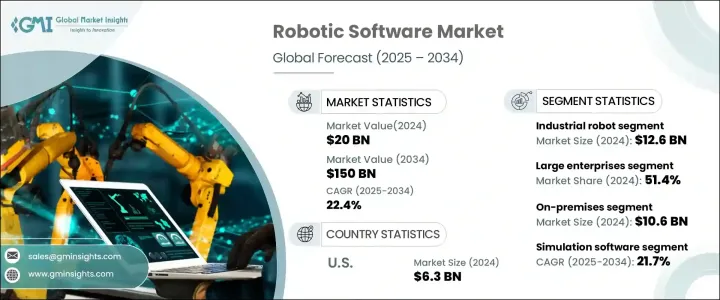

2024 年全球机器人软体市场价值为 200 亿美元,预计 2025 年至 2034 年期间的复合年增长率将达到 22.4%。推动这一成长的因素包括人工智慧和机器学习日益融入机器人软体,以及各行各业对协作机器人的需求不断增长。企业正在大力投资智慧自动化解决方案,以简化营运、降低成本并提高生产力。人工智慧和机器学习正在改变机器人系统,使它们能够做出数据驱动的决策、适应动态环境并以更高的精度执行复杂任务。

这些进步在製造业、医疗保健、物流和农业等领域尤为明显,自动化正在优化效率并提高整体产出。劳动密集和重复性过程对机器人的依赖日益增加,推动了对能够管理、分析和增强机器人性能的先进软体解决方案的需求。此外,世界各国政府和企业都在增加对智慧机器人的投资,进一步加速市场扩张。基于云端的机器人技术、增强的连接性和无缝软体整合的兴起,使得机器人应用更具可扩展性和可访问性,为各种规模的企业利用自动化获得竞争优势开闢了新的机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 200亿美元 |

| 预测值 | 1500亿美元 |

| 复合年增长率 | 22.4% |

市场根据机器人类型进行细分,其中工业机器人和服务机器人是两个主要类别。 2024年,工业机器人软体占据市场主导地位,规模达126亿美元。这些系统对于自动化製造和组装流程、减少错误和提高营运效率至关重要。工业机器人软体结合了强大的资料分析工具,可以即时洞察机器人的操作,帮助企业优化效能、最大限度地减少停机时间并提高产品品质。此外,模拟和视觉化工具等功能使用户能够在部署之前预测和缓解潜在问题,确保无缝整合到生产环境中。随着各行各业越来越重视自动化以满足不断增长的需求并保持竞争优势,工业机器人软体的采用率将大幅上升。

企业规模是影响机器人软体市场的另一个关键部分,涵盖大型企业和中小型企业 (SME)。大型企业在 2024 年占据了 51.4% 的市场份额,凸显了其在采用机器人解决方案方面的主导作用。这些组织运作多条生产线、仓库和物流中心,需要先进的软体来实现无缝协调、任务管理和流程最佳化。机器人软体使大公司能够监控效能、自动执行重复性任务并增强可扩展性,最终提高效率并节省成本。同时,中小企业也越来越多地投资于机器人自动化,以提高营运灵活性、降低劳动力成本,并在不断变化的商业环境中更有效地竞争。

2024 年美国机器人软体市场价值为 63 亿美元,反映了该国在自动化和先进机器人技术应用方面的领导地位。随着製造业、医疗保健和物流等行业采用智慧自动化,对机器人软体解决方案的需求持续激增。对成本效益高、高效和精确的製造流程的追求正在推动企业实施人工智慧机器人技术,以提高生产品质并减少人工干预。随着美国公司寻求透过智慧自动化优化运营,美国仍然是塑造全球机器人软体格局的关键参与者。

目录

第一章:方法论与范围

- 市场范围和定义

- 基础估算与计算

- 预测计算

- 资料来源

- 基本的

- 次要

- 付费来源

- 公共资源

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 人工智慧和机器学习日益融入机器人软体

- 协作机器人需求不断成长

- 各行各业自动化程度提高

- 提高各行各业对机器人的采用率

- 产业陷阱与挑战

- 初期投资高

- 与现有系统整合的综合体

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按软体类型,2021-2034 年

- 主要趋势

- 模拟软体

- 导航和地图软体

- 数据分析与管理软体

- 视觉软体

- 预测性维护软体

- 其他的

第六章:市场估计与预测:依机器人类型,2021-2034

- 主要趋势

- 工业机器人

- 服务机器人

第七章:市场估计与预测:依部署模式,2021-2034

- 主要趋势

- 本地

- 基于云端

第八章:市场估计与预测:依企业规模,2021-2034

- 主要趋势

- 大型企业

- 中小企业(SME)

第九章:市场估计与预测:依最终用途产业,2021-2034 年

- 主要趋势

- 製造业

- 汽车

- 卫生保健

- 运输和物流

- 金融服务业

- 零售与电子商务

- 其他的

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- ABB Ltd

- Amazon Robotics (Amazon.com, Inc.)

- Autodesk, Inc.

- Blue Prism Group plc

- Boston Dynamics

- Clearpath Robotics

- Cognex Corporation

- Denso Corporation

- FANUC Corporation

- Hanson Robotics

- iRobot Corporation

- KUKA AG

- Mitsubishi Electric Corporation

- NVIDIA Corporation

- Omron Corporation

- Open Robotics (OSRF)

- Rockwell Automation, Inc.

- Siemens AG

- SoftBank Robotics

- Teradyne Inc.

- UiPath Inc.

- Universal Robots A/S

- Vecna Robotics

- Yaskawa Electric Corporation

The Global Robotic Software Market was valued at USD 20 billion in 2024 and is expected to expand at a CAGR of 22.4% from 2025 to 2034. This growth is being driven by the increasing integration of artificial intelligence and machine learning into robotic software, as well as the rising demand for collaborative robots across industries. Businesses are investing heavily in intelligent automation solutions to streamline operations, reduce costs, and enhance productivity. AI and ML are transforming robotic systems by enabling them to make data-driven decisions, adapt to dynamic environments, and perform complex tasks with greater precision.

These advancements are particularly evident in sectors such as manufacturing, healthcare, logistics, and agriculture, where automation is optimizing efficiency and improving overall output. The growing reliance on robotics for labor-intensive and repetitive processes is fueling the demand for advanced software solutions capable of managing, analyzing, and enhancing robot performance. Additionally, governments and enterprises worldwide are ramping up investments in smart robotics, further accelerating market expansion. The rise of cloud-based robotics, enhanced connectivity, and seamless software integration is making robotic applications more scalable and accessible, opening new opportunities for businesses of all sizes to leverage automation for competitive advantage.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $20 Billion |

| Forecast Value | $150 Billion |

| CAGR | 22.4% |

The market is segmented based on the type of robot, with industrial robots and service robots being the two primary categories. In 2024, industrial robot software dominated the market, accounting for USD 12.6 billion. These systems are essential for automating manufacturing and assembly processes, reducing errors, and improving operational efficiency. Industrial robot software incorporates powerful data analytics tools that provide real-time insights into robotic operations, allowing businesses to optimize performance, minimize downtime, and enhance product quality. Additionally, features such as simulation and visualization tools enable users to anticipate and mitigate potential issues before deployment, ensuring seamless integration into production environments. As industries increasingly prioritize automation to meet growing demands and maintain a competitive edge, the adoption of industrial robot software is set to rise significantly.

Enterprise size is another crucial segment shaping the robotic software market, encompassing both large enterprises and small and medium-sized enterprises (SMEs). Large enterprises accounted for a 51.4% market share in 2024, highlighting their dominant role in adopting robotic solutions. These organizations operate multiple production lines, warehouses, and logistics centers, necessitating advanced software for seamless coordination, task management, and process optimization. Robotic software enables large companies to monitor performance, automate repetitive tasks, and enhance scalability, ultimately leading to higher efficiency and cost savings. Meanwhile, SMEs are also increasingly investing in robotic automation to improve operational agility, minimize labor costs, and compete more effectively in an evolving business landscape.

The U.S. robotic software market was valued at USD 6.3 billion in 2024, reflecting the country's leadership in automation and advanced robotics adoption. With industries such as manufacturing, healthcare, and logistics embracing intelligent automation, demand for robotic software solutions continues to surge. The push for cost-effective, efficient, and precise manufacturing processes is driving businesses to implement AI-powered robotics to enhance production quality and reduce human intervention. As American companies seek to optimize operations through intelligent automation, the U.S. remains a key player in shaping the global robotic software landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing integration of AI and ML into robotic software

- 3.6.1.2 Rising demand for collaborative robots

- 3.6.1.3 Increased automation across industries

- 3.6.1.4 Raising the adoption of robots across various sectors

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial investments

- 3.6.2.2 Complexes in integration with existing systems

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Software Type, 2021-2034 (USD Billion)

- 5.1 Key trends

- 5.2 Simulation software

- 5.3 Navigation and mapping software

- 5.4 Data analytics and management software

- 5.5 Vision software

- 5.6 Predictive maintenance software

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Robot Type, 2021-2034 (USD Billion)

- 6.1 Key trends

- 6.2 Industrial robot

- 6.3 Service robot

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021-2034 (USD Billion)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud-based

Chapter 8 Market Estimates & Forecast, By Enterprise Size, 2021-2034 (USD Billion)

- 8.1 Key trends

- 8.2 Large enterprise

- 8.3 Small and Medium Enterprises (SME)

Chapter 9 Market Estimates & Forecast, By End-use Industry, 2021-2034 (USD Billion)

- 9.1 Key trends

- 9.2 Manufacturing

- 9.3 Automotive

- 9.4 Healthcare

- 9.5 Transportation and logistics

- 9.6 BFSI

- 9.7 Retail & e-commerce

- 9.8 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 ABB Ltd

- 11.2 Amazon Robotics (Amazon.com, Inc.)

- 11.3 Autodesk, Inc.

- 11.4 Blue Prism Group plc

- 11.5 Boston Dynamics

- 11.6 Clearpath Robotics

- 11.7 Cognex Corporation

- 11.8 Denso Corporation

- 11.9 FANUC Corporation

- 11.10 Hanson Robotics

- 11.11 iRobot Corporation

- 11.12 KUKA AG

- 11.13 Mitsubishi Electric Corporation

- 11.14 NVIDIA Corporation

- 11.15 Omron Corporation

- 11.16 Open Robotics (OSRF)

- 11.17 Rockwell Automation, Inc.

- 11.18 Siemens AG

- 11.19 SoftBank Robotics

- 11.20 Teradyne Inc.

- 11.21 UiPath Inc.

- 11.22 Universal Robots A/S

- 11.23 Vecna Robotics

- 11.24 Yaskawa Electric Corporation

机器人软体市场规模、份额和成长分析(按软体类型、机器人类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测

机器人软体市场规模、份额和成长分析(按软体类型、机器人类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测 机器人软体市场-全球产业规模、份额、趋势、机会和预测,按软体类型、机器人类型、企业规模、产业垂直领域、地区和竞争格局划分,2020-2030年预测

机器人软体市场-全球产业规模、份额、趋势、机会和预测,按软体类型、机器人类型、企业规模、产业垂直领域、地区和竞争格局划分,2020-2030年预测 机器人软体平台市场:按软体类型、机器人类型、部署类型、组织规模和行业垂直领域划分 - 全球预测 2025-2032 年

机器人软体平台市场:按软体类型、机器人类型、部署类型、组织规模和行业垂直领域划分 - 全球预测 2025-2032 年 视觉引导机器人软体市场,按组件类型、按行业垂直、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测飞机平台市场(按组件、飞机类型、技术、最终用户和应用划分)—2025-2030 年全球预测

视觉引导机器人软体市场,按组件类型、按行业垂直、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测飞机平台市场(按组件、飞机类型、技术、最终用户和应用划分)—2025-2030 年全球预测 飞机平台市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

飞机平台市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球飞机平台市场按类型、动力来源、推进技术和地区划分 - 预测至 2030 年

全球飞机平台市场按类型、动力来源、推进技术和地区划分 - 预测至 2030 年 2030 年飞机平台市场预测:按飞机类型、零件、技术、应用、最终用户和地区进行的全球分析

2030 年飞机平台市场预测:按飞机类型、零件、技术、应用、最终用户和地区进行的全球分析 2025 年至 2029 年全球移动机器人平台市场

2025 年至 2029 年全球移动机器人平台市场 机器人软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)

机器人软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)