|

市场调查报告书

商品编码

1642129

机器人软体:市场占有率分析、产业趋势与统计、成长预测(2025-2030 年)Robot Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

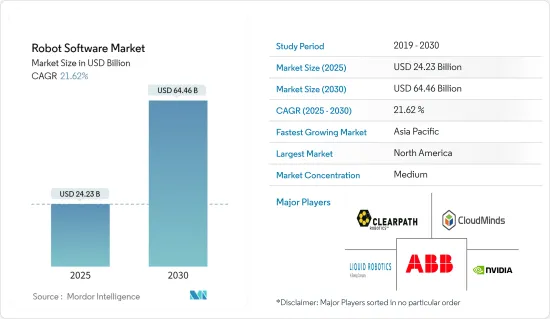

机器人软体市场规模预计在 2025 年为 242.3 亿美元,预计到 2030 年将达到 644.6 亿美元,预测期内(2025-2030 年)的复合年增长率为 21.62%。

机器人软体可实现智慧、运动、安全和生产力功能,使机器人能够观察、感知、学习并保持安全。这些功能和优势使用户能够快速轻鬆地推出并运作机器人,以实现最佳生产力。

主要亮点

- 推动机器人软体市场发展的关键因素是采用人工智慧、提高速度、提高品质、降低人事费用、提高精度和提高生产的扩充性。

- 製造业、电气电子、汽车、食品饮料和製程控制等各种终端用户产业对机器人技术的采用日益广泛,预计将成为机器人软体平台市场的主要成长要素。机器人技术在各个终端用户产业的应用日益广泛,有助于满足客製化需求,同时降低人事费用。

- 自从机器人发明以来,软体在机器人领域就发挥着至关重要的作用。随着新软体功能的推出,可以更好地控制机器人、更快地自订序列和易于使用,该软体预计将在未来几年进一步推动机器人技术的应用。

- 然而,资料安全和日益增多的网路攻击正在阻碍市场成长。此外,机器人犯罪的增加阻碍了各个领域采用机器人,从而降低了采用机器人软体的前景。此外,缺乏熟练的专业知识也是该市场发展的一大限制。

- COVID-19 有力地推动了机器人软体的扩大使用和机器人研究的改进。疫情期间,各公司部署了机器人对区域进行消毒,并为隔离人员运送食物。其他公司也设计了机器人软体来帮助追踪当地社区的 COVID-19。

机器人软体市场趋势

工业机器人是主要应用

- 随着物联网 (IIoT) 等技术的出现,再加上工业 4.0 以及智慧工厂概念的重要性,工业机器人在整个製造业的应用正在日益增加。工业机器人通常用于取代人类工人执行危险或重复性的高精度任务。根据IFR预测,到2024年,亚洲/澳洲安装的工业机器人数量将达到37万台。

- 为了有效率地运作机器人,机器人软体对于根据製造商的需求操作机器人至关重要。该软体是人类能力的延伸。它体现了人类的视野随着每一代和技术的飞跃而日益清晰。随着工业领域机器人技术的快速发展,对机器人软体的需求也大幅增加。

- 此外,人工智慧和机器学习能力正在迅速渗透到工业机器人技术中。机器人技术与人工智慧技术结合的最大优势之一是透过预测性维护来提高运作和生产力。

- 人工智慧与工业机器人技术的整合将使机器人能够监控自身的准确性和性能,并在需要维护时提供讯号,从而避免代价高昂的停机。

- 此外,2023 年 5 月,Alphabet 宣布推出其工业机器人部门 Intrinsic 的首款产品 Flowstate。 Flowstate 是一个直觉的基于 Web 的开发环境,可协助公司建立机器人工作流程,为使用者提供开始建立机器人系统的基础和测试其设计的模拟功能。具体来说,该软体旨在使非专家能够理解和使用机器人系统。

亚太地区:预计大幅成长

- 预计亚太地区在预测期内将呈现显着的成长机会。为该地区机器人软体市场的成长做出贡献的主要国家是中国、日本、新加坡、韩国和印度。该地区的国家正在增加整体行业对机器人技术的采用。

- 中国市场预计将增加对人工智慧和机器人技术的支出,因为中国在其「十三五」规划中明确表示将重点放在这些技术。中国国家发展和改革委员会宣布了一项为期三年的人工智慧实施方案,预计将加速采用先进技术,帮助中国在 2030 年成为超级大国。

- 化工厂等执行危险作业的组织对自动化和安全的需求不断增加,推动了市场的成长。此外,工业物联网 (IIoT) 等最尖端科技的日益普及(该技术是智慧工厂计划与工业 4.0 结合不可或缺的一部分)正在推动工业机器人市场的成长。

- 此外,过去几年来,机器人工作单元的成本每年下降 5-10%,而机器人的速度和产量却大幅提高。

机器人软体产业概况

随着机器人技术在全球范围内的渗透及其在各个行业的应用,机器人软体市场变得越来越复杂。机器人软体公司不断专注于开发先进技术以增强机器人流程并帮助增强製造流程。市场上的知名供应商包括 ABB Ltd、Clearpath Robotics、NVIDIA Corporation 和 CloudMinds Technology Inc.

- 2023 年 12 月-ABB 有限公司宣布加强与沃尔沃汽车的长期伙伴关係关係,为该公司打造下一代电动车提供 1,300 多个机器人和功能套件。这将有助于这家瑞典汽车製造商实现其雄心勃勃的永续性目标。

- 2023 年 10 月-NVIDIA 在其 Jeston 平台上宣布了两个用于边缘 AI 和机器人的框架:NVIDIA Isaac ROS 机器人框架。

其他福利:

- Excel 格式的市场预测 (ME) 表

- 3 个月的分析师支持

目录

第 1 章 简介

- 研究假设和市场定义

- 研究范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概况

- 产业价值链分析

- 产业吸引力-波特五力分析

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争强度

- COVID-19 市场影响评估

第五章 市场动态

- 市场驱动因素

- 组织对自动化和安全的需求日益增加

- 中小企业快速采用机器人软体来降低人事费用和能源成本

- 市场挑战

- 部署成本上升以及针对软体的恶意软体攻击增多

第六章 市场细分

- 依软体类型

- 辨识软体

- 模拟软体

- 预测性维护软体

- 资料管理与分析软体

- 通讯管理软体

- 按机器人类型

- 工业机器人

- 服务机器人

- 按部署

- 本地

- 一经请求

- 按公司规模

- 中小型企业

- 大型企业

- 按行业

- 车

- 零售与电子商务

- 政府和国防

- 卫生保健

- 运输和物流

- 製造业

- 资讯科技/通讯

- 其他最终用户产业

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

第七章 竞争格局

- 公司简介

- ABB Ltd

- Clearpath Robotics

- NVIDIA Corporation

- CloudMinds Technology Inc.

- Liquid Robotics Inc.

- Brain Corporation

- AIBrain Inc.

- Furhat Corporation

- Neurala Inc.

第八章投资分析

第九章 市场机会与未来趋势

The Robot Software Market size is estimated at USD 24.23 billion in 2025, and is expected to reach USD 64.46 billion by 2030, at a CAGR of 21.62% during the forecast period (2025-2030).

Robot software enables functions for intelligence, motion, safety, and productivity and gives the power to get the robots to see, feel, learn, and maintain security. These characteristics and benefits allow users to instantly and easily get their robots up and running at optimum productivity.

Key Highlights

- The major factors driving the robot software market are the adoption of artificial intelligence, enhanced speed, improved quality, reduced labor cost, increased accuracy, and production scalability.

- Rising adoption of robots across various end-user industries such as manufacturing, electrical and electronics, automotive, food and beverage, and process controls are seen as primary growth drivers for the robotics software platforms market. The growing utilization of robots in varied end-user industries helps meet customized demand while simultaneously helping lower labor costs.

- Since the invention of robots, software has played a key role in the field of robotics. With the introduction of new software features that enable better control of the robot, quick customization of sequences, and ease of use, the software is expected to further boost the adoption of robotics in the coming years.

- However, data security and increasing cyberattacks are hindering market growth. Also, increasing robot crimes are impeding the adoption of robots in various sectors, thus, reducing the robot software adoption prospects. Also, the lack of skilled expertise is another major restraining factor for this market.

- COVID-19 provided a solid push to expand the usage of robot software and improve robotics research. During the pandemic, various companies have installed robots to disinfect areas and deliver food to quarantined people. Some companies designed robot software to help people track COVID-19 in their communities.

Robot Software Market Trends

Industrial Robots to Have the Majority Application

- With the advent of technologies like the Industrial Internet of Things (IIoT), vital to the smart factory concept coupled with Industry 4.0, industrial robot adoption is increasing across the manufacturing industries. An industrial robot is generally used in place of human laborers to perform dangerous or repetitive tasks with high accuracy. and According to IFR It is projected that by 2024, industrial robot installations in Asia/Australia will reach 370,000 units.

- In order to make the robots perform efficiently, robot software is essential to operate the robots according to the needs of the manufacturers. This software is an extension of human capability. It reflects the human vision that gets keener with every generation and every technological leap. With the enormous growth of robotics in the industrial sector, the need for robotic software is also increasing substantially.

- Moreover, Artificial Intelligence and machine learning capabilities have been rapidly making their way into industrial robotics technology. One of the most significant benefits derived from the merging of robotics and AI technology is increased uptime and productivity from predictive maintenance.

- With AI integrated with industrial robotics technology, robots are able to monitor their own accuracy and performance, providing signals when maintenance is required to avoid expensive downtime.

- Furthermore, in May 2023, Alphabet launched the first product under its industrial robotics business unit Intrinsic, called Flowstate, which is an intuitive, web-based developer environment where companies can create robotic workflows, offering users the foundation to begin building robotic systems, as well as simulation capabilities to test designs. In particular, the software is aimed at helping non-experts understand and leverage robotic systems.

The Asia-Pacific Region Expected to Register Significant Growth

- The Asia-Pacific region is expected to exhibit significant growth opportunities over the forecast period. The major economies contributing to the growth of the robot software market in this region are China, Japan, Singapore, South Korea, and India. The countries in this region are increasingly adopting robotics across industries.

- The Chinese market is expected to increase its expenditure on AI and robotics, as the country has categorically prioritized its focus on AI and robotics in its 13th five-year plans. China's National Development and Reform Commission has announced an AI three-year implementation program expected to accelerate the adoption of advanced technologies to help the country become a superpower by 2030.

- Rise in demand for automation and safety in organization for hazardous works like chemical plants and others, is driving the growth of the market. Furthermore, with the rising adoption of cutting-edge technologies like the Industrial Internet of Things (IIoT) vital to the smart factory concept coupled with Industry 4.0, and industrial robot is driving the growth of the market

- In addition, the cost of robot work cells has decreased by 5-10% per year since few years and the speed and throughput of robot has increased significantly; due to which there is an increase in adoption of robots, which in turns drives the growth of the market across the region.

Robot Software Industry Overview

The Robot Software Market is semi-conslodiated owing to the penetration of robotics globally with applications in various industries. Robotic software companies are constantly focusing on developing advanced technologies that would enhance the robotic processes and help the manufacturing industries to intensify their process. Some of the prominent vendors in the market include ABB Ltd, Clearpath Robotics, NVIDIA Corporation, and CloudMinds Technology Inc.

- December 2023 - ABB Ltd has announced the strengthening of its long-standing partnership with Volvo Cars to supply more than 1,300 robots and functional packages to build the next generation of electric vehicles. This will support the Swedish car manufacturer to achieve its ambitious sustainability targets.

- October 2023 - NVIDIA announced launch of its to two frameworks on the Jeston Platform for edge AI and robotics the NVIDIA Isaac ROS robotics framework for Robotics Platform to Meet the Rise of Generative AI, More than 10,000 companies building on the NVIDIA Jetson platform can now use new generative AI, APIs and microservices to accelerate industrial digitalization.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Assessment of the Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rise in need for automation and safety in organizations

- 5.1.2 Rapid adoption of robot software by SMEs to reduce labor and energy costs

- 5.2 Market Challenges

- 5.2.1 High cost of implementation and rise in malware attacks on the software

6 MARKET SEGMENTATION

- 6.1 By Software Type

- 6.1.1 Recognition Software

- 6.1.2 Simulation Software

- 6.1.3 Predictive Maintenance Software

- 6.1.4 Data Management and Analysis Software

- 6.1.5 Communication Management Software

- 6.2 By Robot Type

- 6.2.1 Industrial Robots

- 6.2.2 Service Robots

- 6.3 By Deployment

- 6.3.1 On-Premise

- 6.3.2 On-Demand

- 6.4 By Enterprise Size

- 6.4.1 Small and Medium Enterprises

- 6.4.2 Large Enterprises

- 6.5 By End-user Vertical

- 6.5.1 Automotive

- 6.5.2 Retail and E-commerce

- 6.5.3 Government and Defense

- 6.5.4 Healthcare

- 6.5.5 Transportation and Logistics

- 6.5.6 Manufacturing

- 6.5.7 IT and Telecommunications

- 6.5.8 Other End-user Verticals

- 6.6 By Geography

- 6.6.1 North America

- 6.6.2 Europe

- 6.6.3 Asia-Pacific

- 6.6.4 Latin America

- 6.6.5 Middle-East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ABB Ltd

- 7.1.2 Clearpath Robotics

- 7.1.3 NVIDIA Corporation

- 7.1.4 CloudMinds Technology Inc.

- 7.1.5 Liquid Robotics Inc.

- 7.1.6 Brain Corporation

- 7.1.7 AIBrain Inc.

- 7.1.8 Furhat Corporation

- 7.1.9 Neurala Inc.

8 INVESTMENT ANALYSIS

9 MARKET OPPORTUNITIES AND FUTURE TRENDS

机器人软体市场规模、份额和成长分析(按软体类型、机器人类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测

机器人软体市场规模、份额和成长分析(按软体类型、机器人类型、部署模式、组织规模、垂直产业和地区划分)-2026-2033年产业预测 机器人软体市场-全球产业规模、份额、趋势、机会和预测,按软体类型、机器人类型、企业规模、产业垂直领域、地区和竞争格局划分,2020-2030年预测

机器人软体市场-全球产业规模、份额、趋势、机会和预测,按软体类型、机器人类型、企业规模、产业垂直领域、地区和竞争格局划分,2020-2030年预测 机器人软体平台市场:按软体类型、机器人类型、部署类型、组织规模和行业垂直领域划分 - 全球预测 2025-2032 年

机器人软体平台市场:按软体类型、机器人类型、部署类型、组织规模和行业垂直领域划分 - 全球预测 2025-2032 年 视觉引导机器人软体市场,按组件类型、按行业垂直、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测飞机平台市场(按组件、飞机类型、技术、最终用户和应用划分)—2025-2030 年全球预测

视觉引导机器人软体市场,按组件类型、按行业垂直、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测飞机平台市场(按组件、飞机类型、技术、最终用户和应用划分)—2025-2030 年全球预测 飞机平台市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

飞机平台市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球飞机平台市场按类型、动力来源、推进技术和地区划分 - 预测至 2030 年机器人软体市场机会、成长动力、产业趋势分析及 2025-2034 年预测

全球飞机平台市场按类型、动力来源、推进技术和地区划分 - 预测至 2030 年机器人软体市场机会、成长动力、产业趋势分析及 2025-2034 年预测 2030 年飞机平台市场预测:按飞机类型、零件、技术、应用、最终用户和地区进行的全球分析

2030 年飞机平台市场预测:按飞机类型、零件、技术、应用、最终用户和地区进行的全球分析 2025 年至 2029 年全球移动机器人平台市场

2025 年至 2029 年全球移动机器人平台市场