|

市场调查报告书

商品编码

1699400

数位健康市场机会、成长动力、产业趋势分析及 2025-2034 年预测Digital Health Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

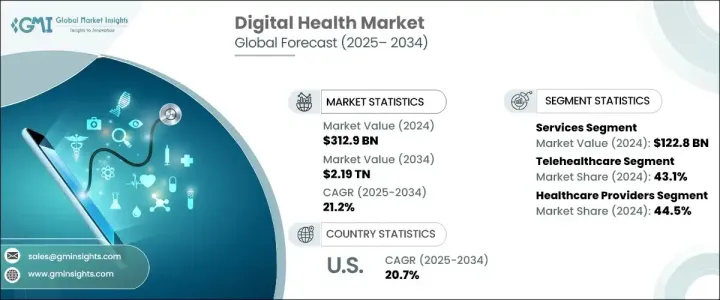

2024 年全球数位健康市场价值为 3,129 亿美元,预计在 2025 年至 2034 年期间的复合年增长率将达到 21.2%。这一显着增长源于尖端数位技术在医疗保健领域的日益融合。人工智慧 (AI)、巨量资料分析、云端运算和物联网 (IoT) 正在改变行业、提高效率并加强患者护理。由于对改善可近性、经济有效的治疗和即时患者监控的需求,对数位健康解决方案的需求持续激增。数位医疗解决方案的快速发展不仅提高了营运效率,而且重新定义了患者参与度,为更个人化和数据驱动的医疗方法铺平了道路。

世界各国政府和私人投资者正在大力资助数位健康计划,进一步加速市场的扩张。支持远距医疗、人工智慧诊断和数位治疗的强有力政策框架在重塑医疗保健服务方面发挥关键作用。连网设备和行动医疗 (mHealth) 应用的兴起极大地影响了患者的行为,促使人们转向预防和远距照护模式。此外,慢性病和人口老化的日益普及也增加了对数位健康平台的需求,使其成为现代医疗保健生态系统不可或缺的组成部分。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3129亿美元 |

| 预测值 | 2.19兆美元 |

| 复合年增长率 | 21.2% |

数位健康市场分为三个核心部分:硬体、软体和服务。该服务领域在 2024 年的价值为 1,228 亿美元,预计到 2034 年将以 21.3% 的复合年增长率成长。这一扩张是由对远距病人监控、远距医疗和医疗保健分析的激增的需求所推动的。随着人工智慧和物联网等先进技术的融合,数位医疗服务正在简化营运、增强医疗服务并促进无缝的患者与提供者互动。随着医疗保健组织寻求优化工作流程和改善患者治疗效果,数位服务正成为高效、主动医疗介入的关键推动因素。

远距医疗、行动医疗(mHealth)、健康分析和数位健康系统仍然处于行业进步的前沿。到 2024 年,远距医疗领域将占据 43.1% 的市场份额,这得益于对虚拟咨询、远距诊断和远距医疗平台的依赖日益增加。 COVID-19 疫情加速了这些技术的采用,凸显了可访问且可扩展的医疗保健解决方案的必要性。因此,全球医疗保健提供者继续整合远距医疗服务,以扩大其覆盖范围并提高医疗服务的可近性,确保患者及时获得具有成本效益的医疗服务。

2024 年,美国数位医疗市场规模达 1,236 亿美元,预估 2025 年至 2034 年期间的复合年增长率为 20.7%。凭藉强大的监管框架、高投资水平和先进的数位基础设施,美国在数位医疗应用领域仍处于全球领先地位。人工智慧诊断工具、远端患者监控解决方案和数据驱动医疗保健模式的广泛实施巩固了美国市场的主导地位。随着下一代技术的日益融合和基于价值的医疗的强劲推动,美国的数位医疗产业将经历持续成长,巩固其作为全球市场驱动力的地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 远距病人监护服务需求不断增长

- 智慧型手机普及率和网路连线率不断提高

- 政府在数位医疗领域采取的优惠措施和资金支持

- 创投不断成长

- 产业陷阱与挑战

- 资料隐私和安全问题

- 实施成本高

- 成长动力

- 成长潜力分析

- 市场进入格局

- 监管格局

- 我们

- 欧洲

- 按地区进行的投资分析

- 我们

- 欧洲

- 亚太地区

- 併购格局

- 报销场景

- 数位健康项目/计划

- 技术格局

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按组成部分,2021 年至 2034 年

- 主要趋势

- 硬体

- 软体

- 基于云端

- 本地

- 服务

第六章:市场估计与预测:按技术,2021 年至 2034 年

- 主要趋势

- 远距医疗

- 远距医疗

- 活动监控

- 远端药物管理

- 远距医疗

- 长期照护监测

- 视讯咨询

- 远距医疗

- 行动医疗

- 穿戴式装置和连网医疗设备

- 血压监测仪

- 心率监测器

- 血糖监测仪

- 脉搏血氧仪

- 睡眠追踪器

- 神经系统监测器

- 其他穿戴式装置和连网医疗设备

- 行动医疗应用

- 医疗应用

- 女性健康应用

- 慢性病管理应用

- 个人健康记录应用

- 药物管理应用程式

- 远端监控应用程式

- 其他医疗应用

- 健身应用

- 医疗应用

- 穿戴式装置和连网医疗设备

- 健康分析

- 预测分析

- 规范分析

- 描述性分析

- 数位健康系统

- 电子健康纪录(EHR)

- 电子处方系统

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医疗保健提供者

- 患者

- 付款人

- 其他最终用途

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Accenture

- AMD Global Telemedicine

- American Well (Amwell)

- Athenahealth

- Capsa Healthcare

- Eagle Telemedicine

- Firstbeat Technologies

- GE Healthcare

- Health Catalyst

- Honeywell International

- IBM

- iHealth Lab

- Koninklijke Philips NV

- McKesson Corporation

- Oracle (Cerner Corporation)

- Qualcomm Technologies

- Teladoc Health

- Veradigm LLC (Allscripts Healthcare Solutions)

The Global Digital Health Market was valued at USD 312.9 billion in 2024 and is poised to expand at a CAGR of 21.2% between 2025 and 2034. This remarkable growth stems from the increasing integration of cutting-edge digital technologies in healthcare. Artificial intelligence (AI), big data analytics, cloud computing, and the Internet of Things (IoT) are transforming the industry, driving efficiency, and enhancing patient care. The demand for digital health solutions continues to surge, fueled by the need for improved accessibility, cost-effective treatments, and real-time patient monitoring. The rapid evolution of digital healthcare solutions is not just improving operational efficiency but also redefining patient engagement, paving the way for more personalized and data-driven medical approaches.

Governments and private investors worldwide are heavily funding digital health initiatives, further accelerating the market's expansion. Strong policy frameworks supporting telehealth adoption, AI-driven diagnostics, and digital therapeutics are playing a pivotal role in reshaping healthcare delivery. The rise of connected devices and mobile health (mHealth) applications has significantly influenced patient behaviors, prompting a shift toward preventive and remote care models. Additionally, the increasing prevalence of chronic diseases and aging populations has heightened the demand for digital health platforms, making them indispensable components of modern healthcare ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $312.9 Billion |

| Forecast Value | $2.19 trillion |

| CAGR | 21.2% |

The digital health market is categorized into three core components: hardware, software, and services. The services segment, valued at USD 122.8 billion in 2024, is expected to grow at a CAGR of 21.3% through 2034. This expansion is driven by the soaring demand for remote patient monitoring, telehealth, and healthcare analytics. With the integration of advanced technologies such as AI and IoT, digital health services are streamlining operations, enhancing care delivery, and fostering seamless patient-provider interactions. As healthcare organizations seek to optimize workflows and improve patient outcomes, digital services are becoming a critical enabler of efficient and proactive medical interventions.

Telehealthcare, mobile health (mHealth), health analytics, and digital health systems remain at the forefront of industry advancements. The telehealthcare segment accounted for 43.1% of the market share in 2024, propelled by the growing reliance on virtual consultations, remote diagnostics, and telemedicine platforms. The COVID-19 pandemic accelerated the adoption of these technologies, highlighting the necessity of accessible and scalable healthcare solutions. As a result, healthcare providers globally continue to integrate telehealth services to expand their reach and enhance care accessibility, ensuring patients receive timely and cost-effective medical attention.

The U.S. digital health market generated USD 123.6 billion in 2024, with a projected CAGR of 20.7% between 2025 and 2034. The country remains a global leader in digital healthcare adoption, backed by strong regulatory frameworks, high investment levels, and an advanced digital infrastructure. The widespread implementation of AI-powered diagnostic tools, remote patient monitoring solutions, and data-driven healthcare models has cemented the U.S. market's dominance. With the increasing integration of next-gen technologies and a robust push toward value-based care, the digital health sector in the U.S. is set to experience sustained growth, reinforcing its position as a driving force in the global market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for remote patient monitoring services

- 3.2.1.2 Increasing smartphone penetration and internet connectivity

- 3.2.1.3 Favorable government initiatives and fundings in digital health

- 3.2.1.4 Growing venture capital investments

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security concerns

- 3.2.2.2 High implementation cost

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Market entry landscape

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.6 Investment analysis, by region

- 3.6.1 U.S.

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.7 Merger and acquisition landscape

- 3.8 Reimbursement scenario

- 3.9 Digital health project/initiatives

- 3.10 Technology landscape

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Component, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.3.1 Cloud-based

- 5.3.2 On-premises

- 5.4 Services

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Telehealthcare

- 6.2.1 Telecare

- 6.2.1.1 Activity monitoring

- 6.2.1.2 Remote medication management

- 6.2.2 Telehealth

- 6.2.2.1 LTC monitoring

- 6.2.2.2 Video consultation

- 6.2.1 Telecare

- 6.3 mHealth

- 6.3.1 Wearables and connected medical devices

- 6.3.1.1 Blood pressure monitors

- 6.3.1.2 Heart rate monitors

- 6.3.1.3 Blood glucose monitor

- 6.3.1.4 Pulse oximeters

- 6.3.1.5 Sleep trackers

- 6.3.1.6 Neurological monitors

- 6.3.1.7 Other wearables and connected medical devices

- 6.3.2 mHealth apps

- 6.3.2.1 Medical apps

- 6.3.2.1.1 Womens health apps

- 6.3.2.1.2 Chronic disease management apps

- 6.3.2.1.3 Personal health record apps

- 6.3.2.1.4 Medication management apps

- 6.3.2.1.5 Remote monitoring apps

- 6.3.2.1.6 Other medical apps

- 6.3.2.2 Fitness apps

- 6.3.2.1 Medical apps

- 6.3.1 Wearables and connected medical devices

- 6.4 Health analytics

- 6.4.1 Predictive analytics

- 6.4.2 Prescriptive analytics

- 6.4.3 Descriptive analytics

- 6.5 Digital health systems

- 6.5.1 Electronic health records (EHRs)

- 6.5.2 e-prescribing systems

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Healthcare providers

- 7.3 Patients

- 7.4 Payers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Accenture

- 9.2 AMD Global Telemedicine

- 9.3 American Well (Amwell)

- 9.4 Athenahealth

- 9.5 Capsa Healthcare

- 9.6 Eagle Telemedicine

- 9.7 Firstbeat Technologies

- 9.8 GE Healthcare

- 9.9 Health Catalyst

- 9.10 Honeywell International

- 9.11 IBM

- 9.12 iHealth Lab

- 9.13 Koninklijke Philips N.V.

- 9.14 McKesson Corporation

- 9.15 Oracle (Cerner Corporation)

- 9.16 Qualcomm Technologies

- 9.17 Teladoc Health

- 9.18 Veradigm LLC (Allscripts Healthcare Solutions)

2026年全球数位健康监测设备市场报告

2026年全球数位健康监测设备市场报告 慢性病数位健康解决方案市场规模、份额和成长分析:按组件、疾病类型、应用、最终用户产业和地区划分-2026-2033年产业预测2026年全球数位听诊市场报告

慢性病数位健康解决方案市场规模、份额和成长分析:按组件、疾病类型、应用、最终用户产业和地区划分-2026-2033年产业预测2026年全球数位听诊市场报告 2026-2034年医疗保健产业电脑化维护管理系统(CMMS)全球市场规模、份额、趋势和成长分析报告全球数位医疗市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年医疗保健产业电脑化维护管理系统(CMMS)全球市场规模、份额、趋势和成长分析报告全球数位医疗市场规模、份额、趋势和成长分析报告(2026-2034) 日本数位医疗市场报告:按类型、组件和地区划分(2026-2034年)

日本数位医疗市场报告:按类型、组件和地区划分(2026-2034年) 2025-2029年全球医疗保健技术领域人工智慧市场

2025-2029年全球医疗保健技术领域人工智慧市场 数位健康市场-全球产业规模、份额、趋势、机会及预测(依技术、组件、地区及竞争格局划分,2021-2031年)数位医疗市场-2026-2031年预测全球数位医疗市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的分析以及未来预测(2026-2034)

数位健康市场-全球产业规模、份额、趋势、机会及预测(依技术、组件、地区及竞争格局划分,2021-2031年)数位医疗市场-2026-2031年预测全球数位医疗市场:市场规模、份额、成长率、产业分析、按类型、应用和地区划分的分析以及未来预测(2026-2034)