|

市场调查报告书

商品编码

1699405

临床试验市场机会、成长动力、产业趋势分析及 2025-2034 年预测Clinical Trials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

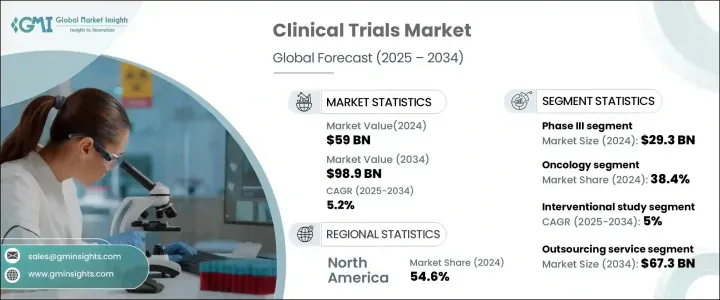

2024 年全球临床试验市场价值为 590 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.2%。对先进治疗方案的需求不断增长,加上对药物开发的投资不断增加,正在推动市场扩张。随着癌症、糖尿病和心血管疾病等慢性疾病变得越来越普遍,製药和生技公司正在加强推出创新疗法。临床研究活动的激增反映了向精准医疗和标靶治疗的更广泛转变,进一步推动了临床试验领域的成长。此外,人工智慧 (AI)、巨量资料分析和分散试验等技术进步正在改变临床研究,使试验更有效率、更具成本效益。监管部门对快速药品审批的支持以及研究机构和医疗保健提供者之间合作的加强也促进了市场扩张。随着对以患者为中心的方法和自适应试验设计的日益关注,临床试验市场将在未来几年见证重大变革。

临床试验市场依阶段分为 I 期、II 期、III 期和 IV 期。其中,III 期临床试验占主导地位,2024 年市场规模将达 293 亿美元。这些大规模试验对于在监管部门批准之前验证药物的安全性和有效性至关重要。鑑于其复杂性和对多样化患者群体的需求,第三阶段研究在多个地点进行,以产生全面的临床资料。随着各公司不断推动新型药物配方和生物相似药的研发,对广泛的 III 期试验的需求持续上升,巩固了该领域在市场上的领先地位。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 590亿美元 |

| 预测值 | 989亿美元 |

| 复合年增长率 | 5.2% |

根据研究设计,临床试验分为介入性研究、观察性研究、扩展研究。介入研究领域在 2024 年引领市场,预计 2025 年至 2034 年的复合年增长率为 5%。这些研究透过积极让参与者参与受控治疗方案,在确定新医疗干预措施的有效性方面发挥关键作用。透过消除回忆偏差并提供对治疗结果的结构化评估,介入试验提供了最高水准的临床证据。因此,製药公司和监管机构越来越依赖这些研究来加速药物审批并提高治疗标准。

2024 年,北美临床试验市场占有 54.6% 的份额,由于製药和生物技术公司高度集中,保持了主导地位。随着药物开发(尤其是精准医疗和生物製剂)的日益复杂,该地区的公司正在大力投资临床试验,将下一代治疗方法推向市场。强有力的监管框架、完善的研究基础设施以及增加的临床研究资金进一步支持了北美在该领域的领导地位。随着对创新疗法的需求不断增加,该地区有望继续成长,巩固其在全球临床研究中的关键作用。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 全球慢性病盛行率不断上升

- 将临床试验外包给CRO的需求不断成长

- 政府和非政府对临床试验的资助增加

- 亚太国家进行临床试验的机会日益增多

- 产业陷阱与挑战

- 缺乏临床研究的熟练劳动力

- 发展中国家的基础建设障碍

- 北美和欧洲进行临床试验所面临的挑战

- 成长动力

- 成长潜力分析

- 临床试验量分析

- 2021 - 2024 年各地区临床试验数量分析

- 2021 - 2024 年临床试验数量分析(依开发阶段划分)

- 2021 - 2024 年临床试验量分析(依适应症)

- 监管格局

- 我们

- 欧洲

- 亚太地区

- 新加坡

- 马来西亚

- 印尼

- 泰国

- 韩国

- 菲律宾

- 临床试验—亚太优势

- 波特分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 併购格局

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依阶段,2021 年至 2034 年

- 主要趋势

- 第一阶段

- 第二阶段

- 第三阶段

- 第四阶段

第六章:市场估计与预测:依研究设计,2021 年至 2034 年

- 主要趋势

- 干预性研究

- 观察性研究

- 扩展访问研究

第七章:市场估计与预测:依服务类型,2021 年至 2034 年

- 主要趋势

- 外包服务

- 内部服务

第八章:市场估计与预测:按治疗领域,2021 年至 2034 年

- 主要趋势

- 自体免疫疾病

- 肿瘤学

- 心臟病学

- 传染病

- 皮肤科

- 眼科

- 神经病学

- 血液学

- 其他治疗领域

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 波兰

- 荷兰

- 瑞士

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 新加坡

- 马来西亚

- 印尼

- 泰国

- 菲律宾

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Charles River Laboratories

- Clinipace

- Eli Lilly and Company

- ICON

- IQVIA

- Laboratory Corporation of America Holdings (Covance Inc)

- Medpace

- Merck & Co

- Parexel International Corporation

- Pfizer

- SGS SA

- Syneos Health

- The Emmes Company

- Thermo Fisher Scientific (PPD)

- Veeda Clinical Research

- Worldwide Clinical Trials

- WuXi AppTech

The Global Clinical Trials Market was valued at USD 59 billion in 2024 and is projected to grow at a CAGR of 5.2% between 2025 and 2034. The rising demand for advanced treatment options, coupled with increasing investments in drug development, is driving market expansion. As chronic diseases such as cancer, diabetes, and cardiovascular conditions become more prevalent, pharmaceutical and biotechnology companies are ramping up their efforts to introduce innovative therapies. The surge in clinical research activity reflects a broader shift toward precision medicine and targeted treatments, further fueling growth in the clinical trials sector. Additionally, technological advancements such as artificial intelligence (AI), big data analytics, and decentralized trials are transforming clinical research, making trials more efficient and cost-effective. Regulatory support for fast-track drug approvals and increased collaboration between research institutions and healthcare providers are also contributing to market expansion. With an increasing focus on patient-centric approaches and adaptive trial designs, the clinical trials market is set to witness significant evolution in the coming years.

The clinical trials market is segmented by phase into Phase I, II, III, and IV. Among these, Phase III dominates the sector, accounting for USD 29.3 billion in 2024. These large-scale trials are critical for validating a drug's safety and efficacy before regulatory approval. Given their complexity and the need for diverse patient populations, Phase III studies are conducted across multiple locations to generate comprehensive clinical data. As companies push forward with novel drug formulations and biosimilars, the demand for extensive Phase III trials continues to rise, reinforcing this segment's leading position in the market.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $59 Billion |

| Forecast Value | $98.9 Billion |

| CAGR | 5.2% |

Based on study design, clinical trials are categorized into interventional, observational, and expanded access studies. The interventional study segment led the market in 2024 and is anticipated to grow at a CAGR of 5% from 2025 to 2034. These studies play a pivotal role in determining the efficacy of new medical interventions by actively involving participants in controlled treatment protocols. By eliminating recall bias and offering a structured evaluation of treatment outcomes, interventional trials provide the highest level of clinical evidence. As a result, pharmaceutical companies and regulatory bodies increasingly rely on these studies to accelerate drug approvals and enhance treatment standards.

North America Clinical Trials Market held a 54.6% share in 2024, maintaining its dominance due to a high concentration of pharmaceutical and biotechnology companies. With the growing complexity of drug development, particularly in precision medicine and biologics, companies across the region are investing heavily in clinical trials to bring next-generation treatments to market. Strong regulatory frameworks, well-established research infrastructure, and increased funding for clinical studies further support North America's leadership in the sector. As demand for innovative therapies escalates, the region is poised for continued growth, reinforcing its pivotal role in global clinical research.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic diseases across the globe

- 3.2.1.2 Growing demand for outsourcing clinical trials to CROs

- 3.2.1.3 Rise in government and non-government funding for clinical trials

- 3.2.1.4 Growing opportunities for conducting clinical trials in countries of Asia Pacific

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Lack of skilled workforce in clinical research

- 3.2.2.2 Infrastructural barriers in developing countries

- 3.2.2.3 Challenges faced in North America and Europe for conducting clinical trials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Clinical trials volume analysis

- 3.4.1 Clinical trials volume analysis, by region, 2021 - 2024

- 3.4.2 Clinical trials volume analysis, by phase of development, 2021 - 2024

- 3.4.3 Clinical trials volume analysis, by indication, 2021 - 2024

- 3.5 Regulatory landscape

- 3.5.1 U.S.

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.3.1 Singapore

- 3.5.3.2 Malaysia

- 3.5.3.3 Indonesia

- 3.5.3.4 Thailand

- 3.5.3.5 South Korea

- 3.5.3.6 Philippines

- 3.6 Clinical trials - Asia Pacific advantage

- 3.7 Porters analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Merger and acquisition landscape

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Phase, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Phase I

- 5.3 Phase II

- 5.4 Phase III

- 5.5 Phase IV

Chapter 6 Market Estimates and Forecast, By Study Design, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Interventional study

- 6.3 Observational study

- 6.4 Expanded access study

Chapter 7 Market Estimates and Forecast, By Service Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Outsourcing service

- 7.3 In-house service

Chapter 8 Market Estimates and Forecast, By Therapeutic Area, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Autoimmune disease

- 8.3 Oncology

- 8.4 Cardiology

- 8.5 Infectious disease

- 8.6 Dermatology

- 8.7 Ophthalmology

- 8.8 Neurology

- 8.9 Hematology

- 8.10 Other therapeutic areas

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Poland

- 9.3.7 Netherlands

- 9.3.8 Switzerland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Singapore

- 9.4.7 Malaysia

- 9.4.8 Indonesia

- 9.4.9 Thailand

- 9.4.10 Philippines

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Charles River Laboratories

- 10.2 Clinipace

- 10.3 Eli Lilly and Company

- 10.4 ICON

- 10.5 IQVIA

- 10.6 Laboratory Corporation of America Holdings (Covance Inc)

- 10.7 Medpace

- 10.8 Merck & Co

- 10.9 Parexel International Corporation

- 10.10 Pfizer

- 10.11 SGS SA

- 10.12 Syneos Health

- 10.13 The Emmes Company

- 10.14 Thermo Fisher Scientific (PPD)

- 10.15 Veeda Clinical Research

- 10.16 Worldwide Clinical Trials

- 10.17 WuXi AppTech

人工智慧在临床试验优化市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户、解决方案和阶段划分

人工智慧在临床试验优化市场分析及预测(至2035年):按类型、产品、服务、技术、组件、应用、部署类型、最终用户、解决方案和阶段划分 全球临床试验市场规模、份额、趋势和成长分析报告(2026-2034)

全球临床试验市场规模、份额、趋势和成长分析报告(2026-2034) 临床试验平台市场预测至2034年:按平台类型、临床试验阶段、研究类型、部署模式、应用、最终用户和地区分類的全球分析

临床试验平台市场预测至2034年:按平台类型、临床试验阶段、研究类型、部署模式、应用、最终用户和地区分類的全球分析 临床试验外包市场-全球产业规模、份额、趋势、机会及预测(依临床试验阶段、治疗领域、最终用户、地区及竞争格局划分,2021-2031年)临床试验市场-全球产业规模、份额、趋势、机会及预测(按类型、阶段、研究设计、适应症、最终用户、地区和竞争格局划分,2021-2031年)

临床试验外包市场-全球产业规模、份额、趋势、机会及预测(依临床试验阶段、治疗领域、最终用户、地区及竞争格局划分,2021-2031年)临床试验市场-全球产业规模、份额、趋势、机会及预测(按类型、阶段、研究设计、适应症、最终用户、地区和竞争格局划分,2021-2031年) 临床试验技术服务市场:2026-2032年全球预测(依服务类型、试验阶段、试验设计、治疗领域及最终使用者划分)全球临床研究分析市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)全球临床研究服务市场-2026-2031年预测

临床试验技术服务市场:2026-2032年全球预测(依服务类型、试验阶段、试验设计、治疗领域及最终使用者划分)全球临床研究分析市场:市场规模、占有率、成长率、产业分析、依类型、应用和地区划分的分析以及未来预测(2026-2034)全球临床研究服务市场-2026-2031年预测 临床试验市场:依阶段、研究设计、适应症、服务、申办者类型、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测

临床试验市场:依阶段、研究设计、适应症、服务、申办者类型、国家及地区划分-全球产业分析、市场规模、市场占有率及2025-2032年预测 日本临床试验管理系统市场报告(按组件、部署模式、最终用户和地区划分,2026-2034 年)

日本临床试验管理系统市场报告(按组件、部署模式、最终用户和地区划分,2026-2034 年)