|

市场调查报告书

商品编码

1699432

囊性纤维化治疗市场机会、成长动力、产业趋势分析及 2025-2034 年预测Cystic Fibrosis Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

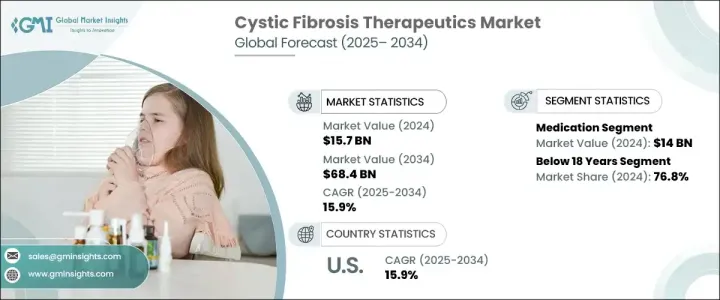

2024 年全球囊性纤维化治疗市场价值为 157 亿美元,预计 2025 年至 2034 年的复合年增长率为 15.9%。囊性纤维化 (CF) 盛行率的不断上升以及对有效治疗方案的日益关注,对市场成长做出了重大贡献。 CF 病例数的不断增加,增加了早期诊断和改善治疗方案的需求,从而推动了对创新治疗的需求。研发投资加速了潜在疗法的进步,特别是 CF 跨膜传导调节剂 (CFTR) 调节剂,从而扩大了临床试验的范围。这些努力旨在提高治疗效果、满足未满足的医疗需求、拓宽市场成长机会。

全球市场分为药物和非药物类别。 2023 年医药领域价值为 119 亿美元,预计 2024 年将创造 140 亿美元的收入。预计在整个预测期内它将保持主导地位,复合年增长率为 16.1%。此部分包括 CFTR 调节剂、支气管扩张剂、抗感染剂、黏液溶解剂、胰酶补充剂和其他药物类别。 CF 药物治疗(尤其是 CFTR 调节剂和其他症状治疗)的持续进步极大地促进了需求。这些药物透过针对 CF 症状和基因突变来改善患者的治疗效果。不断增加的研发投入将继续提高治疗的可用性,以巩固该领域在市场上的地位。个人化医疗的扩展和更广泛的报销支持也是推动该领域成长的关键因素。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 157亿美元 |

| 预测值 | 684亿美元 |

| 复合年增长率 | 15.9% |

依年龄段,市场分为18岁以下、18-40岁、41岁以上。 2024 年,18 岁以下族群的市占率最大,为 76.8%。儿童和青少年的 CF 发生率很高,这推动了对早期诊断和针对性治疗的需求。大多数病例是在儿童早期发现的,需要及时介入和专门治疗。获得改进的诊断工具和创新疗法的机会不断增加,进一步促进了该领域的成长。儿科研究和监管批准在确保整个预测期内继续占据主导地位方面也发挥着至关重要的作用。

2024 年,美国在北美囊性纤维化治疗市场中占有相当大的份额,市场规模将从 2023 年的 89 亿美元增长至 105 亿美元,复合年增长率为 15.9%。该国 CF 患病率高,刺激了对有效治疗的需求,并得到了旨在控制疾病负担的强大研发计划的支持。来自政府和私营部门的大量资金继续推动药物开发的创新,特别是在 CFTR 调节剂和先进疗法方面。透过新型药物配方扩大治疗选择进一步促进了市场成长。强有力的报销政策和领先製药公司的存在有助于该国在市场上保持领先地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 囊性纤维化患者发生率不断上升

- CFTR调节剂治疗的进展

- 研发投入不断增加

- 政府支持和倡议

- 产业陷阱与挑战

- 治疗费用高

- 目前疗法的不良副作用

- 成长动力

- 成长潜力分析

- 管道分析

- 流行病学情景

- 监管格局

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 药物

- 药品类别

- CFTR调节剂

- 黏液溶解剂

- 支气管扩张剂

- 抗感染药物

- 胰酵素补充剂

- 其他药物类别

- 给药途径

- 口服

- 吸入

- 配销通路

- 医院药房

- 零售药局

- 网路药局

- 药品类别

- 非药物治疗

第六章:市场估计与预测:依年龄组,2021 年至 2034 年

- 主要趋势

- 18岁以下

- 18 - 40岁

- 41岁以上

第七章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 爱尔兰

- 亚太地区

- 印度

- 日本

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第八章:公司简介

- Alcresta Therapeutics

- Baxter

- Chiesi Farmaceutici SpA

- F. Hoffmann-La Roche

- Gilead

- Koninklijke Philips NV

- Lupin

- Monaghan Medical

- Novartis AG

- Savara

- Sionna Therapeutics

- Teva Pharmaceutical Industries

- Vertex Pharmaceuticals

The Global Cystic Fibrosis Therapeutics Market was valued at USD 15.7 billion in 2024 and is projected to grow at a CAGR of 15.9% from 2025 to 2034. The increasing prevalence of cystic fibrosis (CF) and the rising focus on effective treatment solutions have contributed significantly to market growth. The growing number of CF cases has heightened the need for early diagnosis and improved therapeutic options, driving demand for innovative treatments. Research and development investments have accelerated advancements in potential therapies, particularly CF transmembrane conductance regulator (CFTR) modulators, leading to an expanding pipeline of clinical trials. These efforts aim to enhance treatment effectiveness and address unmet medical needs, broadening growth opportunities in the market.

The global market is segmented into medication and non-medication categories. The medication segment, valued at USD 11.9 billion in 2023, is projected to generate USD 14 billion in revenue in 2024. It is expected to maintain its dominance throughout the forecast period, growing at a CAGR of 16.1%. This segment includes CFTR modulators, bronchodilators, anti-infective agents, mucolytic agents, pancreatic enzyme supplements, and other drug classes. The growing advancements in CF drug therapies, particularly CFTR modulators and other symptomatic treatments, have significantly boosted demand. These medications improve patient outcomes by targeting CF symptoms and genetic mutations. Increasing research and development investments continue to enhance treatment availability, strengthening the segment's position in the market. The expansion of personalized medicine and broader reimbursement support are also key factors fueling segment growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.7 Billion |

| Forecast Value | $68.4 Billion |

| CAGR | 15.9% |

Based on age group, the market is divided into Below 18 years, 18-40 years, and 41 years and above. In 2024, the Below 18 years segment held the largest market share at 76.8%. The high occurrence of CF in children and adolescents has driven demand for early diagnosis and targeted therapies. Most cases are identified in early childhood, necessitating prompt intervention and specialized treatments. Growing access to improved diagnostic tools and innovative therapies further reinforces segment growth. Pediatric research and regulatory approvals also play a crucial role in ensuring continued dominance throughout the forecast period.

In 2024, the United States held a significant share of the North American cystic fibrosis therapeutics market, generating USD 10.5 billion, up from USD 8.9 billion in 2023, with a CAGR of 15.9%. The high prevalence of CF in the country has fueled the demand for effective treatments, supported by strong research and development initiatives aimed at managing the disease burden. Extensive funding from both government and private sectors continues to drive innovations in drug development, particularly in CFTR modulators and advanced therapies. Expanding treatment options through novel drug formulations further boosts market growth. Strong reimbursement policies and the presence of leading pharmaceutical companies contribute to the country's sustained leadership in the market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing incidence rate of cystic fibrosis patient population

- 3.2.1.2 Advancements in CFTR modulator therapy

- 3.2.1.3 Growing investment in research and development

- 3.2.1.4 Government support and initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High treatment costs

- 3.2.2.2 Adverse side effects of current therapies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Epidemology scenario

- 3.6 Regulatory landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Medication

- 5.2.1 Drug class

- 5.2.1.1 CFTR modulators

- 5.2.1.2 Mucolytic agents

- 5.2.1.3 Bronchodilators

- 5.2.1.4 Anti-infective agents

- 5.2.1.5 Pancreatic enzyme supplements

- 5.2.1.6 Other drug classes

- 5.2.2 Route of administration

- 5.2.2.1 Oral

- 5.2.2.2 Inhalation

- 5.2.3 Distribution channel

- 5.2.3.1 Hospital pharmacies

- 5.2.3.2 Retail pharmacies

- 5.2.3.3 Online pharmacies

- 5.2.1 Drug class

- 5.3 Non-medication

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Below 18 years

- 6.3 18 - 40 years

- 6.4 41 and above

Chapter 7 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 Ireland

- 7.4 Asia Pacific

- 7.4.1 India

- 7.4.2 Japan

- 7.4.3 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Alcresta Therapeutics

- 8.2 Baxter

- 8.3 Chiesi Farmaceutici S.p.A.

- 8.4 F. Hoffmann-La Roche

- 8.5 Gilead

- 8.6 Koninklijke Philips N.V.

- 8.7 Lupin

- 8.8 Monaghan Medical

- 8.9 Novartis AG

- 8.10 Savara

- 8.11 Sionna Therapeutics

- 8.12 Teva Pharmaceutical Industries

- 8.13 Vertex Pharmaceuticals

囊肿纤维化治疗药物市场规模、份额和成长分析(按药物类别、给药途径、分销管道和地区划分)—产业预测(2026-2033 年)

囊肿纤维化治疗药物市场规模、份额和成长分析(按药物类别、给药途径、分销管道和地区划分)—产业预测(2026-2033 年) 囊肿纤维化市场-全球及区域分析:按国家/地区划分-分析与预测(2025-2035)

囊肿纤维化市场-全球及区域分析:按国家/地区划分-分析与预测(2025-2035) 囊肿纤维化市场(按产品类型、给药途径、最终用户和分销管道)—2025-2032 年全球预测

囊肿纤维化市场(按产品类型、给药途径、最终用户和分销管道)—2025-2032 年全球预测 全球囊性纤维化治疗市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年)

全球囊性纤维化治疗市场研究报告 - 产业分析、规模、份额、成长、趋势及预测(2025 年至 2033 年) 囊肿纤维化市场规模、份额、成长分析(按治疗、给药途径、药物类别和地区)- 产业预测(2025 年至 2032 年)

囊肿纤维化市场规模、份额、成长分析(按治疗、给药途径、药物类别和地区)- 产业预测(2025 年至 2032 年) 囊性纤维化治疗市场报告(按药物类别、药物分子类型、给药途径、最终用户和地区划分)2025 年至 2033 年

囊性纤维化治疗市场报告(按药物类别、药物分子类型、给药途径、最终用户和地区划分)2025 年至 2033 年 囊状纤维化症治疗的全球市场的评估:各类药物,各给药途径,各流通管道,各地区,机会,预测(2018年~2032年)

囊状纤维化症治疗的全球市场的评估:各类药物,各给药途径,各流通管道,各地区,机会,预测(2018年~2032年) 囊肿纤维化治疗市场规模、份额、趋势分析报告:按药物类别、给药途径、分销管道、地区、细分市场预测,2025-2030

囊肿纤维化治疗市场规模、份额、趋势分析报告:按药物类别、给药途径、分销管道、地区、细分市场预测,2025-2030