|

市场调查报告书

商品编码

1708158

汽车燃油供给帮浦市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Fuel Feed Pumps Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

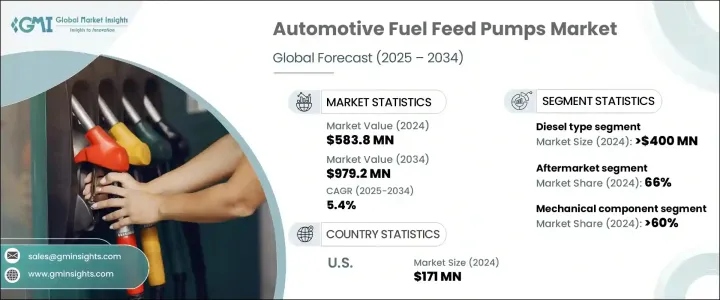

2024 年全球汽车燃油供给帮浦市场价值为 5.838 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.4%。在已开发经济体和新兴经济体汽车产量和销售量激增的推动下,该市场正在稳步扩张。随着中国、印度、巴西等快速成长市场的都市化进程加快、可支配所得增加,对乘用车和商用车的需求也急剧上升。随着道路上车辆数量的增加,对高效燃油供给帮浦系统的需求也日益增长,因为这些零件在确保无缝燃油输送和维持引擎性能方面发挥着至关重要的作用。

此外,汽车工程技术的进步,包括提高燃油效率和控制排放的推动,正在推动先进燃油供给帮浦的采用。由于汽车製造商优先考虑引擎耐用性和优化燃料使用,全球汽车产业向混合动力和先进内燃机的转变也刺激了对高性能燃油供给帮浦系统的需求。此外,由于车队老化导致对替换零件的需求不断增加,加上政府对汽车排放和性能的监管更加严格,正在影响市场动态,并为全球OEM和售后市场供应商创造持续的成长机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 5.838亿美元 |

| 预测值 | 9.792亿美元 |

| 复合年增长率 | 5.4% |

汽车燃油供给帮浦市场依引擎类型分为汽油和柴油两类。其中,柴油引擎燃油供给帮浦在2024年的收入为4亿美元。柴油引擎广泛应用于商用和工业车辆,包括卡车、巴士和建筑机械,所有这些车辆都需要高效耐用的燃油输送系统。柴油供给帮浦对于支援高压燃油喷射系统至关重要,该系统可优化引擎功率、提高燃油效率并确保引擎的长期可靠性。随着全球对重型车辆的需求不断增长,特别是在建筑、物流和公共交通领域,对坚固的柴油供应泵的需求也不断增加。这些泵浦因其能够应对极端操作条件而受到青睐,使其成为各行各业高性能车辆不可或缺的零件。

汽车燃油供给帮浦的销售分为OEM (原厂设备製造商)和售后市场通路。到 2024 年,售后市场将占据主导地位,占有 66% 的份额,这主要是由于随着车辆老化,对更换泵浦的需求不断增加。随着时间的推移,燃油供给帮浦会磨损,需要更换以保持车辆的性能和安全。消费者和车队营运商都在寻求经济高效、可靠的售后解决方案,这些解决方案必须随时可用并且与各种车型相容。售后市场广泛的产品可用性和可负担性继续吸引多样化的客户群,使其成为市场格局的重要组成部分。

美国汽车燃油供给帮浦市场在 2024 年创造了 1.71 亿美元的产值,预计 2025 年至 2034 年的复合年增长率为 5.5%。这一增长主要得益于该国庞大的汽车保有量和强大的汽车製造生态系统。美国车辆平均使用年限的增加扩大了售后市场对燃油供给帮浦的需求,因为更换燃油供给帮浦对于维持车辆的运作和效率至关重要。美国强劲的替代市场凸显了对高品质、耐用的燃油供给帮浦的需求,以满足消费者对性能和寿命的期望。

目录

第一章:方法论与范围

- 研究设计

- 研究方法

- 资料收集方法

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 预测模型

- 初步研究和验证

- 主要来源

- 资料探勘来源

- 市场范围和定义

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 组件提供者

- 製造商

- 技术提供者

- 配销通路分析

- 最终用途

- 利润率分析

- 供应商格局

- 技术与创新格局

- 专利分析

- 监管格局

- 成本細項分析

- 重要新闻和倡议

- 衝击力

- 成长动力

- 增加汽车产量和销售

- 严格的排放法规

- 对节能汽车的需求不断增长

- 汽车技术的进步

- 产业陷阱与挑战

- 创新研发成本高

- 更严格的车辆安全和性能标准

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按引擎,2021 - 2034 年

- 主要趋势

- 汽油

- 柴油引擎

第六章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 机械的

- 电的

- 涡轮泵

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 商用车

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

- 两轮车

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 直接喷射系统

- 多点喷射系统

- 燃油喷射系统

- 化油器发动机

- 高性能车辆

第九章:市场估计与预测:依销售管道,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Aisin Seiki

- AST Otomotiv

- Carter Fuel

- Continental

- Daimler

- Delphi Automotive

- DENSO

- DEUTZ

- Devendra

- HELLA

- Hitachi Astemo

- Johnson Electric

- Perkins Engines

- Rheinmetall

- Robert Bosch

- Scania

- Schaeffler

- SHW

- Valeo

- ZF Friedrichshafen

The Global Automotive Fuel Feed Pumps Market was valued at USD 583.8 million in 2024 and is projected to grow at a CAGR of 5.4% between 2025 and 2034. The market is witnessing steady expansion driven by surging vehicle production and sales across both developed and emerging economies. As urbanization accelerates and disposable incomes rise in fast-growing markets like China, India, and Brazil, the demand for passenger and commercial vehicles is also rising sharply. With more vehicles on the road, the need for efficient fuel feed pump systems is growing, as these components play a crucial role in ensuring seamless fuel delivery and maintaining engine performance.

Additionally, technological advancements in automotive engineering, including the push toward better fuel efficiency and emission control, are fueling the adoption of advanced fuel feed pumps. The global automotive sector's shift toward hybrid and advanced internal combustion engines is also stimulating the demand for high-performance fuel feed pump systems as automakers prioritize engine durability and optimized fuel usage. Furthermore, the increasing need for replacement parts due to aging vehicle fleets, combined with stricter government regulations for vehicle emissions and performance, is influencing market dynamics and creating consistent growth opportunities for both OEM and aftermarket suppliers worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $583.8 Million |

| Forecast Value | $979.2 Million |

| CAGR | 5.4% |

The automotive fuel feed pump market is segmented based on engine type into gasoline and diesel categories. Among these, diesel engine fuel feed pumps accounted for USD 400 million in revenue in 2024. Diesel-powered engines are widely used in commercial and industrial vehicles, including trucks, buses, and construction machinery, all of which require highly efficient and durable fuel delivery systems. Diesel fuel feed pumps are essential in supporting high-pressure fuel injection systems that optimize engine power, improve fuel efficiency, and ensure long-term engine reliability. As global demand for heavy-duty vehicles grows, particularly in the construction, logistics, and public transportation sectors, the need for robust diesel fuel feed pumps is rising. These pumps are favored for their ability to handle extreme operating conditions, making them indispensable components in high-performance vehicles across a range of industries.

Sales of automotive fuel feed pumps are classified into OEM (original equipment manufacturer) and aftermarket channels. The aftermarket segment dominated with a 66% share in 2024, largely due to the rising need for replacement pumps as vehicles age. Over time, fuel feed pumps experience wear and require replacement to maintain vehicle performance and safety. Consumers and fleet operators alike seek cost-effective and reliable aftermarket solutions that are readily available and compatible with a variety of vehicle models. The aftermarket's broad product availability and affordability continue to attract a diverse customer base, making it a critical part of the market landscape.

The U.S. automotive fuel feed pumps market generated USD 171 million in 2024, with expectations to grow at a CAGR of 5.5% from 2025 to 2034. This growth is primarily driven by the country's substantial vehicle fleet and a strong automotive manufacturing ecosystem. The rising average age of vehicles in the U.S. amplifies the demand for aftermarket fuel feed pumps as replacements become essential to keep vehicles operational and efficient. The robust replacement market in the U.S. highlights the need for high-quality, durable fuel feed pumps that align with consumer expectations for performance and longevity.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Key news & initiatives

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Increasing vehicle production & sales

- 3.7.1.2 Stringent emission regulations

- 3.7.1.3 Growing demand for fuel-efficient vehicles

- 3.7.1.4 Advancements in automotive technology

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High R&D costs for innovation

- 3.7.2.2 Stricter vehicle safety & performance standards

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Engine, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Gasoline

- 5.3 Diesel

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Mechanical

- 6.3 Electric

- 6.4 Turbopump

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger Vehicle

- 7.3 Commercial Vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

- 7.4 Two wheelers

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Direct injection system

- 8.3 Multipoint injection system

- 8.4 Fuel injection system

- 8.5 Carbureted engines

- 8.6 High-performance vehicles

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 AST Otomotiv

- 11.3 Carter Fuel

- 11.4 Continental

- 11.5 Daimler

- 11.6 Delphi Automotive

- 11.7 DENSO

- 11.8 DEUTZ

- 11.9 Devendra

- 11.10 HELLA

- 11.11 Hitachi Astemo

- 11.12 Johnson Electric

- 11.13 Perkins Engines

- 11.14 Rheinmetall

- 11.15 Robert Bosch

- 11.16 Scania

- 11.17 Schaeffler

- 11.18 SHW

- 11.19 Valeo

- 11.20 ZF Friedrichshafen

燃油压力调节阀市场按销售管道、车辆类型、燃油类型、最终用户、喷射技术和压力类型划分,全球预测,2026-2032年汽车无刷燃油泵市场按产品类型、燃油类型、电压、车辆类型和分销管道划分,全球预测(2026-2032年)

燃油压力调节阀市场按销售管道、车辆类型、燃油类型、最终用户、喷射技术和压力类型划分,全球预测,2026-2032年汽车无刷燃油泵市场按产品类型、燃油类型、电压、车辆类型和分销管道划分,全球预测(2026-2032年) 汽车帮浦市场规模、份额和成长分析(按类型、技术、排放、车辆类型、销售管道和地区划分)-2026-2033年产业预测汽车帮浦市场按泵浦类型、车辆类型、燃料类型和销售管道-全球预测,2025-2032年汽车燃油输送帮浦市场:按应用、帮浦类型、燃油类型、最终用途和销售管道划分 - 全球预测 2025-2032

汽车帮浦市场规模、份额和成长分析(按类型、技术、排放、车辆类型、销售管道和地区划分)-2026-2033年产业预测汽车帮浦市场按泵浦类型、车辆类型、燃料类型和销售管道-全球预测,2025-2032年汽车燃油输送帮浦市场:按应用、帮浦类型、燃油类型、最终用途和销售管道划分 - 全球预测 2025-2032 汽车帮浦市场:按泵浦类型、销售管道、技术、车辆类型和地区划分

汽车帮浦市场:按泵浦类型、销售管道、技术、车辆类型和地区划分 2025年全球汽车帮浦市场报告

2025年全球汽车帮浦市场报告 全球汽车燃油供给帮浦市场

全球汽车燃油供给帮浦市场 汽车燃油输送泵市场预测至 2032 年:按类型、车辆类型、燃料类型、材料、销售管道、应用和地区进行的全球分析

汽车燃油输送泵市场预测至 2032 年:按类型、车辆类型、燃料类型、材料、销售管道、应用和地区进行的全球分析 全球汽车帮浦市场(按车型、技术、应用、地区和预测)

全球汽车帮浦市场(按车型、技术、应用、地区和预测)