|

市场调查报告书

商品编码

1708211

塑胶托盘市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Plastic Pallets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

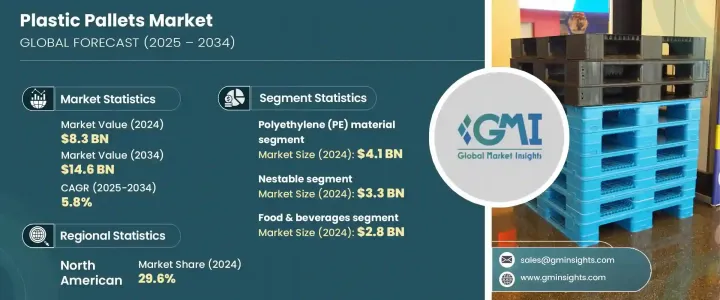

2024 年全球塑胶托盘市场价值为 83 亿美元,预计 2025 年至 2034 年期间的复合年增长率为 5.8%。对高效、可持续和耐用包装解决方案的不断增长的需求推动了这一增长,尤其是在电子商务、零售、製药和冷藏等领域。塑胶托盘比传统木质托盘具有更多优势,包括更耐用、污染风险更低、符合卫生标准。随着全球贸易不断扩大和供应链变得越来越复杂,越来越多的行业选择塑胶托盘来提高物流效率并降低成本。人们越来越重视减少碳足迹和确保运输过程中的产品安全,这进一步加速了各行业对塑胶托盘的采用。

此外,塑胶托盘设计的创新,包括促进仓库自动化的功能,使这些托盘成为现代供应链管理的重要组成部分。人们对塑胶托盘的长期成本效益的认识不断提高,加上政府出于对虫害的担忧而出台的限制木托盘使用的法规,进一步推动了市场的成长。全球对循环经济实践和永续供应链解决方案的推动正在鼓励企业投资可重复使用和可回收的塑胶托盘,从而增强其在不同行业的吸引力。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 83亿美元 |

| 预测值 | 146亿美元 |

| 复合年增长率 | 5.8% |

塑胶托盘市场根据材料进行细分,其中聚乙烯 (PE)、聚丙烯 (PP) 和其他材料构成主要类别。 2024 年 PE 市值为 41 亿美元。由于其价格实惠、重量轻且灵活性强,这种材料仍然是製造商的首选。聚乙烯托盘在零售和电子商务领域特别受欢迎,因为它们能够承受严格的处理,同时保持其结构完整性。它们也广泛用于饮料和快速消费品(FMCG)的运输,其中减震和抗衝击是产品安全的关键因素。

塑胶托盘也按类型分类,市场分为可嵌套、可堆迭、可货架和其他类型。可嵌套塑胶托盘市场在 2024 年创造了 33 亿美元的收入,这得益于对节省空间和具有成本效益的物流解决方案的需求不断增长。可嵌套托盘为减少仓库空间需求和最大限度降低退货运输成本提供了实用的解决方案,使其成为大量运输需求行业的理想选择。优先考虑营运效率和降低碳排放的企业越来越多地转向可嵌套托盘,因为它们能够优化储存空间并降低整体运输成本。

2024 年,北美占据塑胶托盘市场的 29.6%,反映出人们对精简供应链、仓库自动化以及永续包装替代品的关注度日益增长。出于对病虫害控制和卫生问题的考虑,政府对木质托盘使用的监管更加严格,进一步加速了该地区向塑胶托盘的转变。这些托盘提供了更耐用、更持久、更经济的解决方案,满足行业要求和监管标准。随着各行各业不断采用自动化并投资于供应链优化,塑胶托盘将在提高各行业的效率和可持续性方面发挥关键作用。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 电子商务和零售业的成长

- 食品饮料业的采用率不断上升

- 全球贸易和供应链优化的兴起

- 塑胶回收技术的进步

- 冷藏和化工产业的扩张

- 产业陷阱与挑战

- 可修復性有限

- 对塑胶废弃物的环境担忧

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按材料,2021 年至 2034 年

- 主要趋势

- 聚乙烯(PE)

- 高密度聚乙烯

- 低密度聚乙烯

- 聚丙烯(PP)

- 其他的

第六章:市场估计与预测:按类型,2021 年至 2034 年

- 主要趋势

- 可嵌套

- 可架设

- 可堆迭

- 其他的

第七章:市场估计与预测:依最终用途产业,2021 年至 2034 年

- 主要趋势

- 食品和饮料

- 化学品

- 製药

- 汽车

- 其他的

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Bekuplast

- Benoplast

- Cabka

- CHEP

- Craemer

- Loscam International

- Millwood

- Monoflo International

- Naeco Packaging

- Nilkamal Material Handling

- ORBIS Corporation

- Polymer Solutions International

- Premier Handling Solutions

- Rehrig Pacific

- Schoeller Allibert

- Smart-Flow

- TMF Corporation

- Werit Kunststoffwerke

The Global Plastic Pallets Market was valued at USD 8.3 billion in 2024 and is projected to grow at a CAGR of 5.8% between 2025 and 2034. The rising demand for efficient, sustainable, and durable packaging solutions is driving this growth, particularly in sectors such as e-commerce, retail, pharmaceuticals, and cold storage. Plastic pallets offer superior advantages over traditional wooden pallets, including better durability, reduced risk of contamination, and compliance with hygiene standards. As global trade continues to expand and supply chains become more complex, industries are increasingly opting for plastic pallets to enhance logistical efficiency and minimize costs. The growing emphasis on reducing carbon footprints and ensuring product safety during transit has further accelerated the adoption of plastic pallets in various industries.

Additionally, innovations in plastic pallet design, including features that facilitate automation in warehouses, are making these pallets an essential part of modern supply chain management. Rising awareness about the long-term cost benefits associated with plastic pallets, along with government regulations aimed at curbing the use of wooden pallets due to concerns about pest infestations, is further boosting market growth. The global push toward circular economy practices and sustainable supply chain solutions is encouraging companies to invest in reusable and recyclable plastic pallets, enhancing their appeal across diverse industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.3 Billion |

| Forecast Value | $14.6 Billion |

| CAGR | 5.8% |

The plastic pallets market is segmented based on material, with polyethylene (PE), polypropylene (PP), and other materials forming the key categories. The PE segment was valued at USD 4.1 billion in 2024. This material remains a preferred choice among manufacturers due to its affordability, lightweight properties, and remarkable flexibility. Polyethylene pallets are particularly popular in the retail and e-commerce sectors due to their ability to withstand rigorous handling while maintaining their structural integrity. They are also widely used in the transportation of beverages and fast-moving consumer goods (FMCG), where shock absorption and impact resistance are critical factors for product safety.

Plastic pallets are also categorized by type, with the market divided into nestable, stackable, rackable, and other types. The nestable plastic pallet segment generated USD 3.3 billion in 2024, driven by the increasing demand for space-saving and cost-effective logistics solutions. Nestable pallets offer a practical solution for reducing warehouse space requirements and minimizing return shipping costs, making them ideal for industries with high-volume shipping needs. Businesses that prioritize operational efficiency and lower carbon emissions are increasingly turning to nestable pallets for their ability to optimize storage space and reduce overall transportation costs.

North America held a 29.6% share of the plastic pallets market in 2024, reflecting a growing preference for streamlined supply chains, automation in warehouses, and a focus on sustainable packaging alternatives. Stricter government regulations concerning the use of wooden pallets, driven by pest control and hygiene concerns, have further accelerated the shift towards plastic pallets in this region. These pallets offer a more durable, long-lasting, and cost-effective solution that meets both industry requirements and regulatory standards. As industries continue to adopt automation and invest in supply chain optimization, plastic pallets are poised to play a pivotal role in enhancing efficiency and sustainability across various sectors.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growth in e-commerce & retail industry

- 3.2.1.2 Rising adoption in the food & beverage industry

- 3.2.1.3 Rise in global trade & supply chain optimization

- 3.2.1.4 Advancements in plastic recycling technology

- 3.2.1.5 Expansion of cold storage & chemical industries

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited repairability

- 3.2.2.2 Environmental concerns over plastic waste

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 – 2034 (USD Million & Units)

- 5.1 Key trends

- 5.2 Polyethylene (PE)

- 5.2.1 HDPE

- 5.2.2 LDPE

- 5.3 Polypropylene (PP)

- 5.4 Others

Chapter 6 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million & Units)

- 6.1 Key trends

- 6.2 Nestable

- 6.3 Rackable

- 6.4 Stackable

- 6.5 Others

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Million & Units)

- 7.1 Key trends

- 7.2 Food & beverages

- 7.3 Chemicals

- 7.4 Pharmaceuticals

- 7.5 Automotive

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Bekuplast

- 9.2 Benoplast

- 9.3 Cabka

- 9.4 CHEP

- 9.5 Craemer

- 9.6 Loscam International

- 9.7 Millwood

- 9.8 Monoflo International

- 9.9 Naeco Packaging

- 9.10 Nilkamal Material Handling

- 9.11 ORBIS Corporation

- 9.12 Polymer Solutions International

- 9.13 Premier Handling Solutions

- 9.14 Rehrig Pacific

- 9.15 Schoeller Allibert

- 9.16 Smart-Flow

- 9.17 TMF Corporation

- 9.18 Werit Kunststoffwerke

塑胶托盘市场:按产品类型、材料类型、承载能力、尺寸、最终用户、应用和销售管道划分-全球市场预测(2026-2032 年)

塑胶托盘市场:按产品类型、材料类型、承载能力、尺寸、最终用户、应用和销售管道划分-全球市场预测(2026-2032 年) 全球塑胶托盘市场规模、份额、趋势和成长分析报告(2026-2034年)

全球塑胶托盘市场规模、份额、趋势和成长分析报告(2026-2034年) 塑胶托盘:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

塑胶托盘:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 塑胶托盘市场规模、份额和成长分析(按产品类型、托盘类型、材料、最终用途产业和地区划分)-2026-2033年产业预测

塑胶托盘市场规模、份额和成长分析(按产品类型、托盘类型、材料、最终用途产业和地区划分)-2026-2033年产业预测 塑胶托盘市场-全球产业规模、份额、趋势、机会与预测,依材料(高密度聚乙烯、低密度聚乙烯、聚丙烯等)、类型、应用、地区和竞争情况细分,2020-2030 年预测

塑胶托盘市场-全球产业规模、份额、趋势、机会与预测,依材料(高密度聚乙烯、低密度聚乙烯、聚丙烯等)、类型、应用、地区和竞争情况细分,2020-2030 年预测 塑胶托盘市场:依产品类型、按托盘类型、依最终用途产业、按地区

塑胶托盘市场:依产品类型、按托盘类型、依最终用途产业、按地区 北美塑胶托盘市场规模、份额、趋势分析报告:按材料、按产品、按应用、按国家、细分市场预测,2024-2030

北美塑胶托盘市场规模、份额、趋势分析报告:按材料、按产品、按应用、按国家、细分市场预测,2024-2030 2024-2028年全球塑胶托盘市场

2024-2028年全球塑胶托盘市场