|

市场调查报告书

商品编码

1716505

脑炎治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Encephalitis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

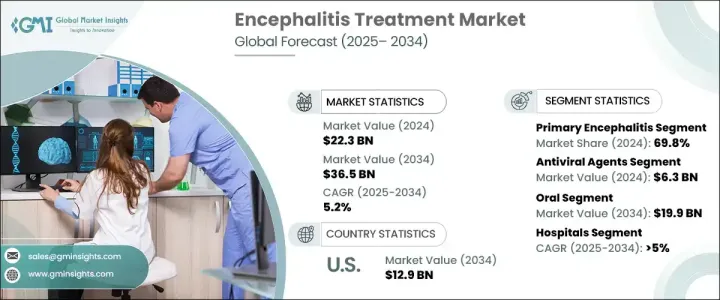

2024 年全球脑炎治疗市场价值为 223 亿美元,预计 2025-2034 年期间复合年增长率为 5.2%。由于病毒感染激增以及环境变化导致的致病媒介接触增加,全球脑炎病例持续上升,该市场有望稳步扩张。随着越来越多的人被诊断出患有这种严重的神经系统疾病,医疗保健系统面临越来越大的压力,需要提供及时有效的治疗方案。媒介传播疾病的盛行率不断上升,加上老年人口的成长,更容易患脑炎,加速了对先进治疗方案的需求。

此外,下一代抗病毒药物、免疫疗法和改进的诊断技术的引入正在进一步重塑脑炎治疗的模式。医疗保健提供者和製药公司正在共同努力创新治疗途径,不仅可以解决急性炎症,还可以防止长期神经损伤。尤其是在已开发经济体中,人们越来越重视早期诊断和干预,这为市场扩张创造了有利的环境。除此之外,公众意识的提高和政府主导的健康倡议正在推动发展中国家对更好的治疗可及性的需求,使脑炎治疗成为全球医疗保健的重点领域。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 223亿美元 |

| 预测值 | 365亿美元 |

| 复合年增长率 | 5.2% |

根据疾病类型,市场分为两大类:原发性脑炎和继发性脑炎。原发性脑炎是由病毒感染直接导致脑部发炎的疾病,2024 年该疾病占全球市场的 69.8%。随着病毒感染发生率的上升,特别是透过蚊子和蜱虫传播的病毒感染,原发性脑炎病例也在增加,对有效治疗方案的需求庞大。抗病毒药物对于治疗这些病例至关重要,因为它们有助于减少发炎和减轻神经系统併发症。此外,气候变迁持续影响媒介传播疾病的传播,直接影响原发性脑炎的流行,进而增加对治疗介入的需求。

根据治疗类型,脑炎治疗市场包括抗生素、类固醇注射、免疫球蛋白疗法、血浆置换、抗病毒药物和其他疗法。其中,抗病毒药物在2024年创收63亿美元,成为主导领域。对抗病毒药物的强劲需求主要是由于全球病毒性脑炎病例数量的增加。这些药物已被证明在控制发炎和预防严重脑损伤方面有效,并已成为标准治疗方案的重要组成部分。预计,对新型抗病毒化合物的研发力度不断加大,加上政府的支持措施和诊断工具的增强,将在未来十年加强该领域的成长轨迹。

2024 年,美国脑炎治疗市场占了 92.6% 的份额,创收 80 亿美元,预计到 2034 年将达到 129 亿美元。美国的成长得益于疾病意识的提高、诊断技术的快速进步以及创新疗法的广泛普及。该国强大的医疗保健基础设施加上大量的医疗保健支出确保了患者能够获得尖端治疗,巩固了该国在脑炎治疗领域的领先地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 脑炎盛行率不断上升

- 人们对脑炎治疗的认识不断提高

- 製药公司加大研发投入

- 产业陷阱与挑战

- 治疗费用高昂

- 成长动力

- 成长潜力分析

- 监管格局

- 管道分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:依疾病类型,2021 年至 2034 年

- 主要趋势

- 原发性脑炎

- 继发性脑炎

第六章:市场估计与预测:依治疗方式,2021 年至 2034 年

- 主要趋势

- 抗病毒药物

- 类固醇注射

- 抗生素

- 免疫球蛋白治疗

- 血浆置换

- 其他治疗

第七章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 口服

- 肠外

- 其他给药途径

第八章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 专科诊所

- 其他最终用途

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- Abbott Laboratories

- Allergan

- Basilea Pharmaceutica

- F. Hoffmann-La Roche

- GlaxoSmithKline

- Melinta Therapeutics

- Merck

- Pfizer

- Sanofi

- Teva Pharmaceutical Industries

The Global Encephalitis Treatment Market was valued at USD 22.3 billion in 2024 and is projected to grow at a CAGR of 5.2% during 2025-2034. This market is poised for steady expansion as cases of encephalitis continue to rise worldwide, driven by a surge in viral infections and increasing exposure to disease-causing vectors due to environmental changes. As more individuals are diagnosed with this serious neurological condition, healthcare systems are under growing pressure to provide timely and effective treatment options. The rising prevalence of vector-borne diseases, combined with the growing elderly population more susceptible to encephalitis, is accelerating the demand for advanced therapeutic solutions.

Additionally, the introduction of next-generation antiviral agents, immunotherapies, and improved diagnostic technologies is further reshaping the landscape of encephalitis treatment. Healthcare providers and pharmaceutical companies are working together to innovate treatment pathways that not only address acute inflammation but also prevent long-term neurological damage. The growing emphasis on early diagnosis and intervention, especially in developed economies, is creating a favorable environment for market expansion. Alongside this, increased public awareness and government-led health initiatives are pushing the demand for better treatment accessibility across developing nations, making encephalitis treatment a key focus area in global healthcare.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $22.3 Billion |

| Forecast Value | $36.5 Billion |

| CAGR | 5.2% |

The market is segmented into two primary categories based on disease type: primary encephalitis and secondary encephalitis. Primary encephalitis, directly caused by viral infections leading to brain inflammation, dominated the global market in 2024 with a 69.8% share. As incidences of viral infections climb, especially those transmitted by mosquitoes and ticks, primary encephalitis cases are growing, creating significant demand for effective treatment solutions. The availability of antiviral drugs is essential in managing these cases, as they help reduce inflammation and mitigate neurological complications. Moreover, climate change continues to influence the spread of vector-borne diseases, directly impacting the prevalence of primary encephalitis and subsequently driving up the need for therapeutic interventions.

Based on treatment type, the encephalitis treatment market includes antibiotics, steroid injections, immunoglobulin therapy, plasmapheresis, antiviral agents, and other therapies. Among these, antiviral agents generated USD 6.3 billion in 2024, emerging as a dominant segment. The strong demand for antiviral medications is primarily fueled by the rising number of viral encephalitis cases worldwide. These drugs have become a critical part of standard treatment regimens due to their proven efficacy in managing inflammation and preventing serious brain damage. Increasing research and development efforts toward novel antiviral compounds, along with supportive government initiatives and enhanced diagnostic tools, are expected to strengthen this segment's growth trajectory over the next decade.

The United States Encephalitis Treatment Market accounted for a substantial 92.6% share in 2024, generating USD 8 billion, and is forecasted to reach USD 12.9 billion by 2034. Growth in the U.S. is driven by heightened disease awareness, rapid diagnostic advancements, and widespread availability of innovative treatments. The country's robust healthcare infrastructure, coupled with significant healthcare spending, ensures that patients have access to cutting-edge therapies, reinforcing the nation's position as a leader in the encephalitis treatment space.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of encephalitis

- 3.2.1.2 Growing awareness about encephalitis treatment

- 3.2.1.3 Increased investment in research and development by pharmaceutical companies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost associated with treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pipeline analysis

- 3.6 Porter's analysis

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Disease Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Primary encephalitis

- 5.3 Secondary encephalitis

Chapter 6 Market Estimates and Forecast, By Treatment, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Antiviral agents

- 6.3 Steroid injections

- 6.4 Antibiotics

- 6.5 Immunoglobulin therapy

- 6.6 Plasmapheresis

- 6.7 Other treatments

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Parenteral

- 7.4 Other routes of administration

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Specialty clinics

- 8.4 Other end use

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 Allergan

- 10.3 Basilea Pharmaceutica

- 10.4 F. Hoffmann-La Roche

- 10.5 GlaxoSmithKline

- 10.6 Melinta Therapeutics

- 10.7 Merck

- 10.8 Pfizer

- 10.9 Sanofi

- 10.10 Teva Pharmaceutical Industries