|

市场调查报告书

商品编码

1716609

心律管理设备市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Cardiac Rhythm Management Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

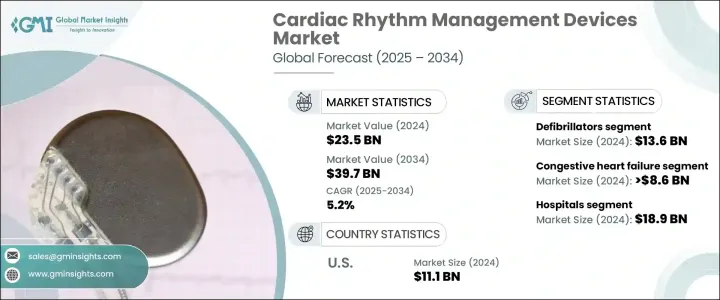

2024 年全球心律管理设备市场规模达到 235 亿美元,预估 2025 年至 2034 年期间的复合年增长率为 5.2%。全球心血管疾病发病率的上升推动了该市场的成长,包括心臟衰竭、心律不整和其他心律相关疾病。主要经济体老龄人口的稳定成长也推动了市场扩张,因为老年人更容易出现心臟併发症。久坐的生活方式、不良的饮食习惯以及高血压、糖尿病和肥胖症病例的增加等因素进一步加剧了对先进心臟护理解决方案的需求。

心血管疾病仍然是全球死亡的主要原因,对能够改善患者预后和提高生活品质的创新和有效的心律管理设备的需求日益增长。此外,远端监控和下一代植入式设备等医疗技术的不断进步正在改变医疗保健提供者管理和治疗心律不整的方式。医疗保健支出的激增,加上人们对早期诊断和预防性心臟病护理的认识的提高,预计将为市场参与者带来新的机会。人工智慧 (AI) 和机器学习 (ML) 与心臟节律管理系统的整合也有望透过实现预测分析和个人化治疗方案来推动未来的市场趋势。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 235亿美元 |

| 预测值 | 397亿美元 |

| 复合年增长率 | 5.2% |

该市场涵盖广泛的产品领域,包括心律调节器、去颤器和心臟再同步治疗 (CRT) 设备。其中,除颤器占据最大的市场份额,对整体收入贡献巨大。除颤器,尤其是植入式心律转復除颤器 (ICD),对于患有危及生命的心律不整高风险的患者至关重要。这些设备旨在持续监测心律,并在检测到异常心律时发出电击,从而防止心臟猝死。由于心血管疾病持续成为全球发病率和死亡率的主要原因,预计对除颤器的需求将稳定上升。

在应用方面,心律管理设备市场分为充血性心臟衰竭、心律不整、心搏过缓和心搏过速。其中,充血性心臟衰竭在2024年的收入为86亿美元。 ICD和CRT系统等设备在心臟衰竭管理中发挥至关重要的作用,可以改善心律协调、提高心输出量,缓解疲劳和呼吸困难等症状,从而提高患者的生活品质。

2024 年,美国心律管理设备市场规模达到 111 亿美元,占全球主导地位。该国先进的医疗保健基础设施,加上优惠的报销框架和广泛的最先进治疗选择,继续推动市场成长。强大的临床研究、持续的产品创新以及对研发的大量投资使得 CRM 设备在美国迅速普及,巩固了其在该领域的全球领先地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 心臟衰竭和其他心臟疾病的盛行率不断上升

- 心律监测技术进步与创新设备的引入

- 提高大众意识

- 久坐的生活方式日益盛行

- 有利的报销方案

- 老年人口基数不断增加,肥胖盛行率不断上升

- 产业陷阱与挑战

- 设备成本高

- 产品召回

- 严格的监管审批

- 成长动力

- 成长潜力分析

- 监管格局

- 报销场景

- 技术格局

- 未来市场趋势

- 2024年定价分析

- 管道产品

- 指示景观

- 2021年至2034年单位数量

- 起搏器

- 除颤器

- CRT 装置

- 波特的分析

- 差距分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 公司市占率分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按产品,2021 年至 2034 年

- 主要趋势

- 起搏器

- 植入式心律调节器

- 体外心律调节器

- 除颤器

- 植入式心臟復律去颤器(ICD)

- 经静脉植入式心臟復律去颤器

- 皮下植入式心臟復律去颤器

- 单腔ICD

- 双腔ICD

- 体外去颤器

- 手动体外心臟去颤器

- 自动体外心臟去颤器

- 半自动体外心臟去颤器

- 全自动体外心臟去颤器

- 穿戴式心臟復律去颤器

- 植入式心臟復律去颤器(ICD)

- 心臟再同步治疗装置

- 心臟再同步治疗装置-D

- 心臟再同步治疗装置-P

第六章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 充血性心臟衰竭

- 心律不整

- 心搏过缓

- 心跳过速

- 其他应用

第七章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 医院

- 心臟护理中心

- 门诊手术中心

- 其他最终用途

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott

- ABIOMED

- Amiitalia

- Asahi Kasei

- BIOTRONIK

- Boston Scientific

- BPL Medical Technologies

- CU Medical

- Defibtech

- LivaNova

- Medico

- Medtronic

- MicroPort

- Nihon Kohden

- Osypka Medical

- Pacetronix

- Philips

- Schiller

- Stryker

- Vitatron

The Global Cardiac Rhythm Management Devices Market reached USD 23.5 billion in 2024 and is projected to expand at a CAGR of 5.2% between 2025 and 2034. The growth of this market is fueled by the rising incidence of cardiovascular diseases worldwide, including heart failure, arrhythmias, and other rhythm-related disorders. The steady increase in aging populations across major economies is also driving market expansion, as older individuals are more prone to cardiac complications. Factors such as sedentary lifestyles, poor dietary habits, and rising cases of hypertension, diabetes, and obesity are further intensifying the need for advanced cardiac care solutions.

With cardiovascular diseases remaining the leading cause of mortality worldwide, there is a growing demand for innovative and effective cardiac rhythm management devices that can improve patient outcomes and enhance quality of life. Additionally, constant advancements in medical technology, including remote monitoring and next-generation implantable devices, are transforming the way healthcare providers manage and treat cardiac rhythm disorders. The surge in healthcare expenditure, coupled with greater awareness about early diagnosis and preventive cardiac care, is expected to open up new opportunities for market players. The integration of artificial intelligence (AI) and machine learning (ML) into cardiac rhythm management systems is also anticipated to drive future market trends by enabling predictive analytics and personalized treatment options.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.5 Billion |

| Forecast Value | $39.7 Billion |

| CAGR | 5.2% |

The market comprises a wide range of product segments, including pacemakers, defibrillators, and cardiac resynchronization therapy (CRT) devices. Among these, defibrillators hold the largest market share, contributing significantly to the overall revenue. Defibrillators, especially implantable cardioverter defibrillators (ICDs), are vital for patients at high risk of life-threatening arrhythmias. These devices are designed to monitor heart rhythms continuously and deliver electric shocks when abnormal rhythms are detected, thereby preventing sudden cardiac death. The demand for defibrillators is expected to rise steadily as cardiovascular conditions continue to be a leading cause of morbidity and mortality globally.

In terms of application, the cardiac rhythm management devices market is segmented into congestive heart failure, arrhythmias, bradycardia, and tachycardia. Among these, congestive heart failure accounted for USD 8.6 billion in 2024. Devices like ICDs and CRT systems play a crucial role in managing heart failure by improving heart rhythm coordination, enhancing cardiac output, and alleviating symptoms such as fatigue and breathlessness, thereby improving patient quality of life.

The United States Cardiac Rhythm Management Devices Market generated USD 11.1 billion in 2024, dominating the global landscape. The country's advanced healthcare infrastructure, coupled with favorable reimbursement frameworks and broad access to state-of-the-art treatment options, continues to propel market growth. Strong clinical research, ongoing product innovations, and significant investments in R&D are enabling the rapid adoption of CRM devices in the U.S., solidifying its position as a global leader in this space.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of heart failure and other cardiac disorders

- 3.2.1.2 Technological advancements and introduction of innovative devices for cardiac rhythm monitoring

- 3.2.1.3 Increasing public awareness

- 3.2.1.4 Rising sedentary lifestyle

- 3.2.1.5 Favorable reimbursement scenario

- 3.2.1.6 Growing geriatric population base coupled with rising prevalence of obesity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of devices

- 3.2.2.2 Product recalls

- 3.2.2.3 Stringent regulatory approvals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Pricing analysis, 2024

- 3.9 Pipeline products

- 3.10 Indication landscape

- 3.11 Number of units, 2021 - 2034

- 3.11.1 Pacemaker

- 3.11.2 Defibrillators

- 3.11.3 CRT devices

- 3.12 Porter's analysis

- 3.13 GAP analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Company market share analysis

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pacemakers

- 5.2.1 Implantable pacemakers

- 5.2.2 External pacemakers

- 5.3 Defibrillators

- 5.3.1 Implantable cardioverter defibrillator (ICDs)

- 5.3.1.1 Transvenous implantable cardioverter defibrillator

- 5.3.1.2 Subcutaneous implantable cardioverter defibrillator

- 5.3.1.2.1 Single-chamber ICDs

- 5.3.1.2.2 Dual-chamber ICDs

- 5.3.2 External defibrillator

- 5.3.2.1 Manual external defibrillator

- 5.3.2.2 Automated external defibrillator

- 5.3.2.2.1 Semi-automated external defibrillator

- 5.3.2.2.2 Fully automated external defibrillator

- 5.3.2.3 Wearable cardioverter defibrillator

- 5.3.1 Implantable cardioverter defibrillator (ICDs)

- 5.4 Cardiac resynchronization therapy devices

- 5.4.1 Cardiac resynchronization therapy devices- D

- 5.4.2 Cardiac resynchronization therapy devices- P

Chapter 6 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Congestive heart failure

- 6.3 Arrhythmias

- 6.4 Bradycardia

- 6.5 Tachycardia

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Cardiac care centers

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott

- 9.2 ABIOMED

- 9.3 Amiitalia

- 9.4 Asahi Kasei

- 9.5 BIOTRONIK

- 9.6 Boston Scientific

- 9.7 BPL Medical Technologies

- 9.8 CU Medical

- 9.9 Defibtech

- 9.10 LivaNova

- 9.11 Medico

- 9.12 Medtronic

- 9.13 MicroPort

- 9.14 Nihon Kohden

- 9.15 Osypka Medical

- 9.16 Pacetronix

- 9.17 Philips

- 9.18 Schiller

- 9.19 Stryker

- 9.20 Vitatron

2026-2034年全球植入式心臟节律管理设备市场规模、份额、趋势和成长分析报告

2026-2034年全球植入式心臟节律管理设备市场规模、份额、趋势和成长分析报告 2026年全球心臟节律管理(CRM)设备及器材市场报告2026年全球植入式心臟节律管理设备市场报告2026-2034年全球心臟节律管理设备市场规模、份额、趋势和成长分析报告

2026年全球心臟节律管理(CRM)设备及器材市场报告2026年全球植入式心臟节律管理设备市场报告2026-2034年全球心臟节律管理设备市场规模、份额、趋势和成长分析报告 心臟监测和心律管理设备市场 - 全球产业规模、份额、趋势、机会、预测(按心臟监测设备、心律管理设备、最终用户、地区和竞争格局划分,2021-2031)

心臟监测和心律管理设备市场 - 全球产业规模、份额、趋势、机会、预测(按心臟监测设备、心律管理设备、最终用户、地区和竞争格局划分,2021-2031) 心臟监测和心律管理设备市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2026-2033 年)

心臟监测和心律管理设备市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2026-2033 年) 心臟节律管理设备市场规模、份额及成长分析(按产品、最终用户及地区划分)-2026-2033年产业预测

心臟节律管理设备市场规模、份额及成长分析(按产品、最终用户及地区划分)-2026-2033年产业预测 心臟节律管理设备:市场洞察、竞争格局及预测(至2032年)全球心臟节律管理设备市场:市场规模、份额、趋势分析(按产品、最终用途和地区划分)、细分市场预测(2025-2033 年)

心臟节律管理设备:市场洞察、竞争格局及预测(至2032年)全球心臟节律管理设备市场:市场规模、份额、趋势分析(按产品、最终用途和地区划分)、细分市场预测(2025-2033 年) 心律管理设备市场,按产品类型、按应用、按最终用户、按配销通路、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

心律管理设备市场,按产品类型、按应用、按最终用户、按配销通路、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测