|

市场调查报告书

商品编码

1740860

扫雪车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Snow Clearing Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

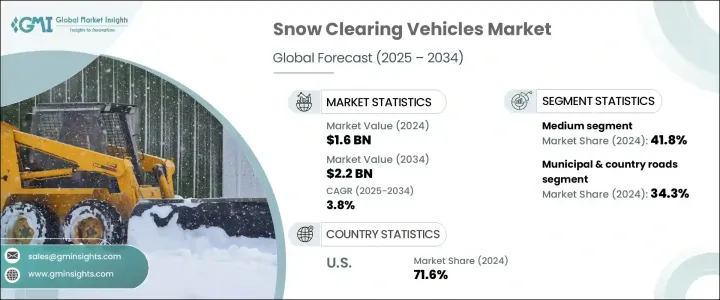

2024 年全球扫雪车市场价值为 16 亿美元,预计到 2034 年将以 3.8% 的复合年增长率增长至 22 亿美元。这一增长主要得益于机场基础设施的不断发展以及各大降雪地区道路交通网络的稳步扩张。随着机场的升级和扩建,尤其是在寒冷地区,对高性能扫雪车的需求持续成长。高效率的扫雪设备对于在严冬条件下维持不间断的服务至关重要。市场也正在更广泛地转向智慧基础设施,市政当局和服务提供者优先考虑先进可靠的扫雪技术,以提高安全性和效率。对永续性、燃油效率和低维护解决方案的日益关注正在改变城市和农村地区的扫雪作业管理方式。

从应用角度来看,扫雪车市场主要分为四大类:机场、高速公路、市政和乡村道路以及其他用途。 2024年,市政和乡村道路领域占据领先地位,市场占有率约为34.3%,预计在整个预测期内的复合年增长率将超过3.5%。该领域至关重要,因为它能够根据独特的区域条件调整和扩展扫雪技术。地方政府经常投资配备耐腐蚀零件、模组化系统和先进除冰技术的多功能车辆。这些客製化配置有助于即使在偏远、难以到达或经常受到恶劣天气影响的地区也能保持稳定的性能。清理市政道路和乡村道路上的积雪通常需要穿越陡峭的地形、未铺砌的路面和狭窄的小径。这导致对采用坚固硬体(例如铰接式铲刀、增强型悬吊和全地形轮胎)的车辆的需求日益增长,这些硬体能够在恶劣的环境条件下承受高强度的工作负荷。随着城镇采用更聪明的雪管理措施,人们对配备 GPS 导航除雪系统、自动撒盐功能和混合动力推进选项的设备的兴趣日益浓厚,以提高可持续性和有效性。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 16亿美元 |

| 预测值 | 22亿美元 |

| 复合年增长率 | 3.8% |

市场也按车型细分为紧凑型、中型和重型车辆。中型车辆细分市场在2024年成为最大的细分市场,约占市场份额的41.8%,预计到2034年将以超过4.3%的复合年增长率成长。这些车辆在清雪作业中发挥着至关重要的作用,尤其是在城市地区和大型商业区。其动力和尺寸的平衡使其能够在需要频繁精确除雪的环境中高效运作。这些车辆有多种型号可供选择,购买者可以根据地形、降雪量和所需的机动性来选择设备。现在,买家可以享受更高的定价透明度,包括可选功能和配件,使市政当局和承包商更容易在有限的预算内进行明智的投资。

按推进类型分类,市场包括内燃机 (ICE)、电动车和混合动力车。由于内燃机汽车在冰冻和恶劣条件下提供高扭矩、持续可靠性和长续航能力的卓越性能,它在 2024 年仍将是市场主导。这些车辆因其在驱动犁车和撒布机等重型除雪设备方面的出色性能而受到操作员的青睐。儘管基于内燃机的系统仍然是最常见的,但人们正逐渐转向使用现代燃油管理系统、低排放技术和导航功能来增强内燃机系统,以满足不断变化的性能和环境标准。

从地区来看,美国在2024年引领了扫雪车市场,市场规模约5亿美元,占据北美总市场份额的近71.6%。美国冬季气候多样,且注重在降雪期间维护道路安全,因此对扫雪解决方案的需求强劲且持续。完善的供应链加上持续的技术进步,使美国始终保持着扫雪车及设备市场的领先地位。

随着产业的不断发展,製造商正致力于设计采用改进材料和技术的扫雪车。强化液压系统、耐腐蚀表面和高扭矩驱动系统正成为标准配备。这些更新不仅延长了车辆寿命,还能确保车辆在严苛的冬季作业中保持顶级性能。硬化钢、轻质合金和先进复合材料等高性能部件正日益集成,以提高车辆的机动性、降低油耗,并增强车辆在极端天气和复杂地形条件下的结构耐久性。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 零件供应商

- 製造商

- 技术提供者

- 服务提供者

- 配销通路

- 最终用途

- 川普政府关税的影响

- 贸易影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(客户成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 贸易影响

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 定价分析

- 推进系统

- 地区

- 对部队的影响

- 成长动力

- 极端天气事件发生频率增加

- 扩建机场基础设施

- 都市化和市政投资

- 公路运输网的成长

- 产业陷阱与挑战

- 资本和维护成本高

- 环境法规和燃油效率标准

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 机场

- 高速公路

- 市政和乡村道路

- 其他的

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 袖珍的

- 中等的

- 重的

第七章:市场估计与预测:按推进方式,2021 - 2034 年

- 主要趋势

- 冰

- 电的

- 杂交种

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 政府和市政当局

- 私人承包商

- 农业部门

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- Aebi Schmidt Holding

- Alamo

- Boschung Holding

- Caterpillar

- Daimler (Mercedes-Benz Trucks)

- Doosan Bobcat

- Faymonville

- Hako Group

- John Deere

- Kassbohrer Gelandefahrzeug

- Kodiak America

- MB Companies

- Montana Manufacturing

- Oshkosh

- Rosenbauer International

- Schmidt Group

- Swarco

- Ventrac

- Wausau Equipment Company

- Zoomlion

The Global Snow Clearing Vehicles Market was valued at USD 1.6 billion in 2024 and is estimated to grow at a CAGR of 3.8% to reach USD 2.2 billion by 2034. This growth is largely fueled by the ongoing development of airport infrastructure and the steady rise in road transportation networks across various regions prone to heavy snowfall. As airports upgrade and expand, especially in colder areas, the demand for high-performance snow removal vehicles continues to grow. Efficient snow clearing equipment is essential to maintaining uninterrupted services during severe winter conditions. The market is also seeing a broader shift toward smart infrastructure, where municipalities and service providers are prioritizing advanced and reliable snow clearing technologies that enhance both safety and efficiency. A growing focus on sustainability, fuel efficiency, and low-maintenance solutions is transforming how snow removal operations are managed in both urban and rural settings.

In terms of application, the snow clearing vehicles market is divided into four main segments: airports, highways, municipal and country roads, and other uses. In 2024, the municipal and country roads segment took the lead with an approximate 34.3% market share and is projected to grow at over 3.5% CAGR throughout the forecast period. This segment is pivotal due to its ability to adapt and scale snow clearing technologies to suit unique regional conditions. Local governments frequently invest in multi-functional vehicles equipped with corrosion-resistant parts, modular systems, and advanced de-icing technology. These customizations help deliver consistent performance even in areas that are remote, hard to reach, or frequently impacted by adverse weather. Clearing snow from municipal routes and country roads often involves navigating steep terrain, unpaved surfaces, and narrow paths. This has led to a growing demand for vehicles built with rugged hardware like articulated blades, reinforced suspensions, and all-terrain tires that can handle intense workloads under harsh environmental conditions. As cities and towns adopt smarter snow management practices, there is a growing interest in equipment with GPS-guided plow systems, automated salting features, and hybrid propulsion options to improve both sustainability and effectiveness.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.6 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 3.8% |

The market is also segmented by vehicle type into compact, medium, and heavy vehicles. The medium vehicle segment emerged as the largest in 2024, accounting for approximately 41.8% of the market, and is expected to grow at a CAGR of over 4.3% through 2034. These vehicles play a critical role in snow clearing operations, particularly in urban areas and large commercial zones. Their balance of power and size allows them to operate efficiently in environments that require frequent and precise snow removal. Available in numerous models, these vehicles allow purchasers to select equipment based on terrain, snowfall levels and required maneuverability. Buyers now benefit from greater transparency in pricing, which includes optional features and attachments, making it easier for municipalities and contractors to invest wisely within limited budgets.

When classified by propulsion type, the market includes internal combustion engine (ICE), electric, and hybrid-powered vehicles. ICE vehicles remain the dominant choice in 2024 due to their proven ability to deliver high torque, consistent reliability, and long operational endurance in freezing and rugged conditions. These vehicles are favored by operators for their performance in driving heavy snow removal equipment such as plows and spreaders. Although ICE-based systems are still the most common, there's a gradual shift toward enhancing them with modern fuel management systems, low-emission technology, and navigation features to meet evolving performance and environmental standards.

Regionally, the United States led the snow clearing vehicles market in 2024, generating around USD 500 million and holding nearly 71.6% of the total share in North America. The country's diverse winter climate and emphasis on maintaining road safety during snow events have created a strong and consistent demand for snow clearing solutions. A well-established supply chain, coupled with ongoing technological advancements, has allowed the U.S. to remain a leading market for snow clearing vehicles and equipment.

As the industry continues to evolve, manufacturers are focusing on designing snow clearing vehicles with improved materials and technology. Reinforced hydraulics, corrosion-resistant surfaces, and high-torque drive systems are becoming standard. These updates not only extend vehicle life but also ensure top-tier performance in demanding winter operations. High-performance components such as hardened steel, lightweight alloys, and advanced composites are being increasingly integrated to boost maneuverability, reduce fuel consumption, and enhance structural durability in extreme weather and challenging landscapes.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component Suppliers

- 3.2.3 Manufacturers

- 3.2.4 Technology Providers

- 3.2.5 Service Providers

- 3.2.6 Distribution channel

- 3.2.7 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Pricing analysis

- 3.9.1 Propulsion

- 3.9.2 Region

- 3.10 Impact on forces

- 3.10.1 Growth drivers

- 3.10.1.1 Increasing frequency of extreme weather events

- 3.10.1.2 Expansion of airport infrastructure

- 3.10.1.3 Urbanization and municipal investments

- 3.10.1.4 Growth in road transportation networks

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High capital and maintenance costs

- 3.10.2.2 Environmental regulations and fuel efficiency standards

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Airports

- 5.3 Highways

- 5.4 Municipal & country roads

- 5.5 Others

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Compact

- 6.3 Medium

- 6.4 Heavy

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Government & municipalities

- 8.3 Private contractor

- 8.4 Agricultural sector

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Aebi Schmidt Holding

- 10.2 Alamo

- 10.3 Boschung Holding

- 10.4 Caterpillar

- 10.5 Daimler (Mercedes-Benz Trucks)

- 10.6 Doosan Bobcat

- 10.7 Faymonville

- 10.8 Hako Group

- 10.9 John Deere

- 10.10 Kassbohrer Gelandefahrzeug

- 10.11 Kodiak America

- 10.12 M-B Companies

- 10.13 Montana Manufacturing

- 10.14 Oshkosh

- 10.15 Rosenbauer International

- 10.16 Schmidt Group

- 10.17 Swarco

- 10.18 Ventrac

- 10.19 Wausau Equipment Company

- 10.20 Zoomlion