|

市场调查报告书

商品编码

1740899

柔性保护包装市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Flexible Protective Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

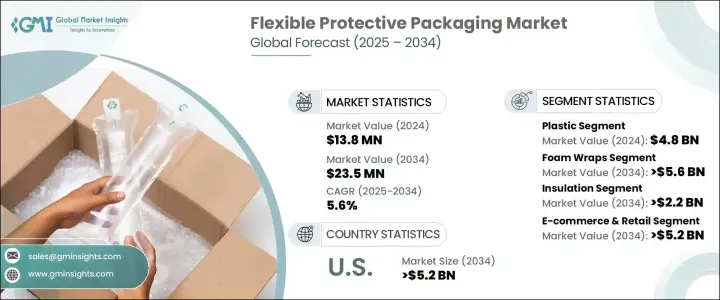

2024年,全球柔性保护性包装市场规模达138亿美元,预计到2034年将以5.6%的复合年增长率成长,达到235亿美元,这得益于电子商务产业的蓬勃发展和「最后一公里」配送网路的进步。随着全球各行各业纷纷转向轻盈、耐用、可持续的包装替代品,以提供成本效益和高效的产品保护,市场正经历快速转变。线上购物平台的日益普及改变了商品的储存、运输和配送方式,这推动了对包装的强烈需求,这种包装不仅能为运输中的物品提供缓衝,还能轻鬆适应各种产品的形状和尺寸。消费者要求更快的配送速度和最小的环境影响,这使得柔性保护性包装成为寻求在性能和永续性之间取得平衡的企业的首选解决方案。可回收、可堆肥和可生物降解包装领域的创新正在稳步涌现,帮助品牌满足监管标准和消费者期望。随着零售商优先考虑全通路履行,灵活的包装提供了策略优势——减轻运输重量、减少浪费并提高整体营运灵活性。

减少塑胶垃圾和推广环保实践的监管压力日益加大,已成为市场成长的关键催化剂。许多企业正积极从刚性、重型包装转向更聪明、更灵活的包装形式,这些包装形式易于定制,运输成本更低。在新兴经济体(尤其是亚太地区),这些趋势尤其明显,线上零售活动的激增加速了对兼具保护性和经济性的包装的需求。气泡膜、泡棉内衬、加垫邮寄袋和气枕等柔性保护包装形式正日益受到青睐,因为它们在减少材料消耗的同时,能够提供强大的缓衝作用。它们节省空间的特性不仅降低了物流成本,还有助于减少运输过程中的碳排放。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 138亿美元 |

| 预测值 | 235亿美元 |

| 复合年增长率 | 5.6% |

美国贸易管理部门先前推出的持续关税政策,为依赖进口原料的国内製造商增加了成本压力。这些关税促使企业重新思考其供应链,导致采购策略和对区域製造中心的投资转变。如此一来,製造商在提升自身韧性的同时,也优化了成本效率。柔性保护性包装在此背景下发挥着至关重要的作用——它有助于减少材料使用量,降低立体运输成本,并实现跨产品线的轻鬆扩展,从而帮助企业在不断变化的市场中占据竞争优势。

在材料类型中,塑胶继续主导柔性保护包装领域,2024 年市场规模达 48 亿美元。聚乙烯、聚丙烯和聚苯乙烯等常见塑胶树脂因其低成本、耐用性和高抗衝击性而仍广受欢迎。这些材料广泛应用于气垫、泡棉内衬和气泡膜等包装解决方案,对于在长途运输过程中保护易碎物品至关重要。随着数位零售的兴起,尤其是在消费性电子产品和化妆品等领域,对这些轻质高性能材料的需求丝毫没有放缓的迹象。

预计到2034年,泡棉包装市场规模将达到56亿美元,成为柔性保护包装领域成长最快的领域之一。泡棉包装因其轻盈和强大的缓衝性能而被广泛应用,是运输过程中保护易碎物品的理想选择。这些包装可以轻鬆塑形成不规则形状,确保物品稳固地受到缓衝,而不会增加体积。处理精密设备的行业(例如医疗设备、电子产品和高檔玻璃器皿)越来越依赖泡沫包装来降低破损、退货和客户不满意的风险。

在美国,预计到2034年,柔性保护性包装市场规模将达到52亿美元,这得益于强大的电商生态系统以及美国对永续包装日益增长的重视。随着网购习惯的日益普及,企业正迅速采用可生物降解的包装、纸质缓衝材料和可回收的塑胶邮寄袋,以满足食品、药品和消费品等行业的需求。这些产业所需的包装解决方案不仅要保护产品的完整性,还要符合环保价值和合规要求。

为了保持竞争优势,安姆科、Smurfit Kappa、Mondi、希悦尔和 Pregis 等行业领导者正在大力投资研发、永续性创新和客製化包装系统。他们还在扩大区域製造业务,以更好地服务全通路零售模式并满足复杂的物流需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 产业衝击力

- 成长动力

- 电子商务扩张

- 永续性和法规遵从性

- 成本和营运效率

- 材料科学的进步

- 消费性电子产品和易腐商品的成长

- 产业陷阱与挑战

- 回收基础设施缺口

- 原物料价格波动

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 未来市场趋势

- 差距分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

第五章:市场估计与预测:按材料类型,2021 - 2034 年

- 塑胶

- 纸和纸板

- 泡棉

- 铝箔

第六章:市场估计与预测:依产品类型,2021 - 2034 年

- 气垫

- 气泡膜

- 泡棉包装

- 邮件程式

- 收缩包装

- 拉伸膜

- 其他的

第七章:市场估计与预测:依功能,2021 - 2034 年

- 空隙填充

- 阻挡和支撑

- 包装

- 绝缘

- 缓衝

- 表面保护

第八章:市场估计与预测:依最终用途,2021 - 2034 年

- 电子商务与零售

- 食品和饮料

- 製药和医疗保健

- 消费者

- 汽车

- 工业的

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Sealed Air Corporation

- Pregis LLC

- Smurfit Kappa Group

- Amcor plc

- Mondi Group

- Huhtamaki Oyj

- Sonoco Products Company

- ProAmpac LLC

- Storopack Hans Reichenecker GmbH

- DS Smith Plc

- Winpak Ltd.

- Mondi Flexible Packaging

- Rengo Co., Ltd.

- AptarGroup, Inc.

- Toray Plastics (America), Inc.

- Schur Flexibles Group

The Global Flexible Protective Packaging Market was valued at USD 13.8 billion in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 23.5 billion by 2034, driven by the expanding e-commerce sector and advancements in last-mile delivery networks. The market is experiencing a rapid shift as industries across the globe lean toward lightweight, durable, and sustainable packaging alternatives that offer cost-efficiency and high product protection. The growing penetration of online shopping platforms has transformed how goods are stored, shipped, and delivered-fueling a strong need for packaging that not only cushions items in transit but also adapts easily to varying product shapes and sizes. Consumers are demanding faster deliveries with minimal environmental impact, making flexible protective packaging a preferred solution for businesses looking to strike a balance between performance and sustainability. Innovations in recyclable, compostable, and biodegradable packaging are emerging at a steady pace, helping brands meet regulatory benchmarks and consumer expectations alike. As retailers prioritize omnichannel fulfillment, flexible packaging is offering a strategic advantage-reducing shipping weights, limiting waste, and enhancing overall operational agility.

Rising regulatory pressure on reducing plastic waste and promoting eco-friendly practices has become a key growth catalyst for the market. Many businesses are proactively shifting from rigid, heavy-duty formats to smarter, flexible options that can be easily customized and shipped at lower costs. Across emerging economies-especially in Asia-Pacific-these trends are even more pronounced, where the spike in online retail activity is accelerating demand for packaging that is both protective and economical. Flexible protective packaging formats such as bubble wraps, foam inserts, padded mailers, and air pillows are gaining traction because they offer strong cushioning with less material consumption. Their space-saving nature not only drives down logistics costs but also helps reduce carbon emissions during transportation.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $13.8 billion |

| Forecast Value | $23.5 billion |

| CAGR | 5.6% |

Ongoing tariff policies introduced during earlier U.S. trade administrations have added cost pressures on domestic manufacturers relying on imported raw materials. These tariffs have prompted companies to rethink their supply chains, leading to a shift in sourcing strategies and investments in regional manufacturing hubs. In doing so, manufacturers are enhancing their resilience while optimizing cost-efficiency. Flexible protective packaging plays a vital role in this landscape-it helps reduce material usage, lowers dimensional shipping costs, and allows easy scalability across product lines, giving businesses a competitive edge in an evolving market.

Among material types, plastic continues to dominate the flexible protective packaging space, generating USD 4.8 billion in 2024. Common plastic resins such as polyethylene, polypropylene, and polystyrene remain popular due to their low cost, durability, and high impact resistance. These materials are extensively used in packaging solutions like air pillows, foam inserts, and bubble wraps, which are essential for protecting fragile items during long-haul shipments. With the rise of digital retail, particularly in sectors like consumer electronics and cosmetics, the demand for these lightweight, high-performance materials shows no signs of slowing down.

The foam wraps segment is projected to generate USD 5.6 billion by 2034, making it one of the fastest-growing areas in flexible protective packaging. Foam wraps are widely used due to their lightweight nature and strong cushioning properties, which are ideal for safeguarding delicate items during transit. These wraps effortlessly mold to irregular shapes, ensuring that items remain securely cushioned without adding excessive bulk. Industries handling precision equipment-such as medical devices, electronics, and luxury glassware-are increasingly depending on foam wraps to reduce the risk of breakage, returns, and customer dissatisfaction.

In the U.S., the flexible protective packaging market is forecasted to generate USD 5.2 billion by 2034, fueled by a strong e-commerce ecosystem and the nation's growing emphasis on sustainable packaging. As online shopping habits intensify, businesses are rapidly adopting biodegradable wraps, paper-based cushioning, and recyclable poly mailers to meet demand across industries such as food, pharmaceuticals, and consumer goods. These sectors require packaging solutions that not only protect product integrity but also align with eco-conscious values and compliance requirements.

To maintain a competitive edge, industry leaders like Amcor, Smurfit Kappa, Mondi, Sealed Air, and Pregis are heavily investing in R&D, sustainability innovation, and customized packaging systems. They are also expanding their regional manufacturing footprint to better serve omnichannel retail models and address complex logistics demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 E-commerce expansion

- 3.3.1.2 Sustainability and regulatory compliance

- 3.3.1.3 Cost and operational efficiency

- 3.3.1.4 Advancements in material science

- 3.3.1.5 Growth in consumer electronics and perishables

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 Recycling infrastructure gaps

- 3.3.2.2 Volatility in raw material prices

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates & Forecast, By Material Type, 2021 - 2034 (USD Million and Units)

- 5.1 Plastic

- 5.2 Paper & paperboard

- 5.3 Foam

- 5.4 Aluminum foil

Chapter 6 Market estimates & forecast, By Product Type, 2021 - 2034 (USD Billion and Units)

- 6.1 Air cushions

- 6.2 Bubble wraps

- 6.3 Foam wraps

- 6.4 Mailers

- 6.5 Shrink wraps

- 6.6 Stretch films

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Function, 2021 - 2034 (USD Billion and Units)

- 7.1 Void Fill

- 7.2 Blocking & bracing

- 7.3 Wrapping

- 7.4 Insulation

- 7.5 Cushioning

- 7.6 Surface protection

Chapter 8 Market estimates & forecast, By End Use, 2021 - 2034 (USD Billion and Units)

- 8.1 E-commerce & retail

- 8.2 Food & beverages

- 8.3 Pharmaceuticals & healthcare

- 8.4 Consumer

- 8.5 Automotive

- 8.6 Industrial

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion and Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Sealed Air Corporation

- 10.2 Pregis LLC

- 10.3 Smurfit Kappa Group

- 10.4 Amcor plc

- 10.5 Mondi Group

- 10.6 Huhtamaki Oyj

- 10.7 Sonoco Products Company

- 10.8 ProAmpac LLC

- 10.9 Storopack Hans Reichenecker GmbH

- 10.10 DS Smith Plc

- 10.11 Winpak Ltd.

- 10.12 Mondi Flexible Packaging

- 10.13 Rengo Co., Ltd.

- 10.14 AptarGroup, Inc.

- 10.15 Toray Plastics (America), Inc.

- 10.16 Schur Flexibles Group

生物降解缓衝材料(花生)市场分析及预测(至2035年):按类型、产品类型、材质、应用、技术、最终用户、功能、製程、安装类型及解决方案划分

生物降解缓衝材料(花生)市场分析及预测(至2035年):按类型、产品类型、材质、应用、技术、最终用户、功能、製程、安装类型及解决方案划分 2026年全球防护包装市场报告

2026年全球防护包装市场报告 2026-2030年全球防护包装市场

2026-2030年全球防护包装市场 高性能防护发泡包装市场(按材料类型、产品类型、通路、应用和最终用户产业划分)-2026-2032年全球预测

高性能防护发泡包装市场(按材料类型、产品类型、通路、应用和最终用户产业划分)-2026-2032年全球预测 防护包装市场规模、份额和成长分析(按类型、材料、功能、最终用途和地区划分)—产业预测(2026-2033 年)按产品类型、应用、分销管道、用途和最终用户分類的防护包装市场—2025-2032年全球预测

防护包装市场规模、份额和成长分析(按类型、材料、功能、最终用途和地区划分)—产业预测(2026-2033 年)按产品类型、应用、分销管道、用途和最终用户分類的防护包装市场—2025-2032年全球预测 全球包装花生市场:预测(至 2032 年)-按产品、材料、类型、分销管道和地区进行分析

全球包装花生市场:预测(至 2032 年)-按产品、材料、类型、分销管道和地区进行分析 全球纸边保护器市场

全球纸边保护器市场 保护性包装市场规模、份额和趋势分析报告:按类型、材料、功能、最终用途、地区和细分市场预测,2025 年至 2033 年

保护性包装市场规模、份额和趋势分析报告:按类型、材料、功能、最终用途、地区和细分市场预测,2025 年至 2033 年 防护包装:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)

防护包装:市场占有率分析、产业趋势、统计数据和成长预测(2025-2030 年)