|

市场调查报告书

商品编码

1740914

再生能源变压器市场机会、成长动力、产业趋势分析及2025-2034年预测Renewable Energy Transformer Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

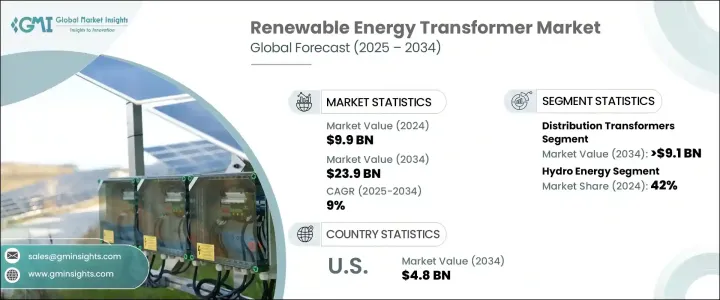

2024年,全球再生能源变压器市场规模达99亿美元,预计2034年将以9%的复合年增长率成长,达到239亿美元。在全球积极向清洁能源转型的推动下,该市场正呈现强劲成长动能。世界各国都在大力投资太阳能、风能和水力发电项目,这导致对能够高效应对再生能源输入动态变化的变压器的需求激增。随着公用事业供应商对老化基础设施进行现代化改造,以及各国政府实施更严格的再生能源目标,对能够确保电网稳定的先进技术变压器的需求也空前高涨。

分散式能源 (DER) 和微电网的兴起,加上储能技术的进步,进一步提升了专用变压器的重要性。越来越多的企业将人工智慧驱动的监控系统和物联网感测器整合到变压器设计中,旨在优化电网性能、最大限度地减少能源损耗并实现预测性维护。电动车的稳定成长、分散式发电的不断扩张以及对智慧城市的投资,都强化了高性能再生能源变压器的需求,为全球市场创造了广阔的机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 99亿美元 |

| 预测值 | 239亿美元 |

| 复合年增长率 | 9% |

太阳能和风能的日益普及,以及全球对清洁能源的大力推广,正在推动这一市场的扩张。随着储能係统获得更多投资以及电网的现代化升级,对能够有效管理再生能源流量波动的变压器的需求日益增长。数位监控系统和智慧电网技术的发展正在推动变压器设计的创新,进一步促进市场成长。政府强制规定和公用事业公司设定的再生能源使用目标继续在刺激需求方面发挥重要作用。

儘管前景乐观,但复杂的监管环境、持续的供应链中断以及原材料价格波动等挑战仍然是关键问题。该行业正致力于开发先进的、可客製化的变压器设计,以满足不断变化的能源和环境标准。贸易政策,包括川普政府时期对进口钢铁、铝和电气元件征收的关税,已显着影响生产成本,迫使製造商调整策略。许多公司正在将生产设施迁移或扩大至台湾、墨西哥和越南等成本效益较高的地区,以更好地管理成本并最大限度地降低风险。

就产品类型而言,配电变压器占据市场主导地位,预计2034年将创造91亿美元的市场价值。这些变压器在将太阳能和风能等再生能源整合到现有电网中发挥着至关重要的作用。物联网感测器和即时效能监控等创新技术正在提升其可靠性和运作效率。电力变压器对于将大容量电力从大型再生能源装置输送到城市中心至关重要,在绝缘和冷却技术的进步推动下,电力变压器也正在强劲增长。

2024年,水力发电领域再生能源变压器市场占比达到42%,预计2034年将以8%的复合年增长率成长。水力发电项目的扩张以及海上和陆上风电装置容量的增加是市场成长的关键驱动力。用于应对太阳能光电系统波动输出的变压器的需求也在大幅成长。

2024 年,美国再生能源变压器市场产值将达 19 亿美元。随着太阳能和风能技术的日益普及,再加上基础设施现代化建设和智慧电网整合,美国市场可望持续扩张。

全球再生能源变压器市场的主要公司包括 Aditya Energy、ABC Transformers、GE Vernova、ACTOM、Acutran、AEP Group、Celme、Hammond Power Solutions、CG Power、Daelim、Deltron Electricals、Eaton、Elsewedy Electric、HD Hyundai Energy Electric、Hitachi Energy、Hyosung Heaton、Elsewedy Electric、HD Hyundai Energy Electric、Hitachi Energy、Hyosung Hebacers、MMGidak、MMGcakak、Siyosung Hekakers、MMGidak、MMGcyekiak、Hyosung Heakem. Energy、Virginia Transformer 和 WEG。这些公司优先考虑能源效率和永续性方面的产品创新,采用先进的监控系统,并策略性地向新兴市场扩张,以满足日益增长的再生能源基础设施需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 战略仪表板

- 创新与永续发展格局

第五章:市场规模及预测:依产品,2021 - 2034

- 主要趋势

- 配电变压器

- 电源变压器

- 逆变变压器

- 其他的

第六章:市场规模及预测:依冷气方式,2021 - 2034

- 主要趋势

- 干式

- 油浸式

第七章:市场规模及预测:依评级,2021 - 2034

- 主要趋势

- ≤10兆伏安

- > 10 MVA 至 ≤ 100 MVA

- > 100 MVA 至 ≤ 600 MVA

- > 600 兆伏安

第 8 章:市场规模与预测:按应用,2021 - 2034 年

- 主要趋势

- 水能

- 风力发电场

- 太阳能光电

- 其他的

第九章:市场规模及预测:按地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 法国

- 俄罗斯

- 英国

- 义大利

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 埃及

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

第十章:公司简介

- ABC Transformers

- ACTOM

- Acutran

- Aditya Energy

- AEP Group

- Celme

- CG Power

- Daelim

- Deltron Electricals

- Eaton

- Elsewedy Electric

- GE Vernova

- Hammond Power Solutions

- HD Hyundai Electric

- Hitachi Energy

- Hyosung Heavy Industries

- MGM Transformers

- Mitsubishi Electric

- Ormazabal

- Prolec Energy

- Siemens Energy

- Virginia Transformer

- WEG

The Global Renewable Energy Transformer Market was valued at USD 9.9 billion in 2024 and is estimated to grow at a CAGR of 9% to reach USD 23.9 billion by 2034. Driven by an aggressive global transition toward clean energy sources, the market is witnessing substantial momentum. Countries across the world are investing heavily in solar, wind, and hydroelectric power projects, leading to a massive demand for transformers capable of efficiently handling the dynamic nature of renewable energy inputs. As utility providers modernize aging infrastructure and governments enforce stricter renewable energy targets, the need for technologically advanced transformers that can ensure grid stability has never been higher.

The rise of distributed energy resources (DERs) and microgrids, combined with advancements in energy storage technologies, are further boosting the importance of specialized transformers. Companies are increasingly integrating AI-driven monitoring systems and IoT-enabled sensors into transformer designs, aiming to optimize grid performance, minimize energy loss, and enable predictive maintenance. The steady growth of electric vehicles, expanding decentralized power generation, and investments in smart cities are reinforcing the necessity for high-performance renewable energy transformers, creating promising opportunities across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.9 Billion |

| Forecast Value | $23.9 Billion |

| CAGR | 9% |

The increasing shift toward solar and wind power, along with a worldwide push for cleaner energy adoption, is fueling this market expansion. As energy storage systems receive more investments and power grids are modernized, there is a growing need for transformers that can efficiently manage the variability of renewable energy flows. The development of digital monitoring systems and smart grid technologies is driving innovations in transformer designs, further contributing to market growth. Government mandates and renewable energy usage targets set by utility companies continue to play a major role in boosting demand.

Despite the positive outlook, challenges such as complex regulatory environments, ongoing supply chain disruptions, and fluctuating raw material prices remain critical concerns. The industry is responding by focusing on advanced, customizable transformer designs that meet evolving energy and environmental standards. Trade policies, including tariffs on imported steel, aluminum, and electrical components enacted during the Trump administration, have significantly impacted production costs, pushing manufacturers to adjust strategies. Many companies are relocating or expanding production facilities to cost-effective regions like Taiwan, Mexico, and Vietnam to better manage expenses and minimize risks.

In terms of product types, distribution transformers dominate the market and are projected to generate USD 9.1 billion by 2034. These transformers play a vital role in integrating renewable energy sources like solar and wind into the existing grid. Innovations such as IoT sensors and real-time performance monitoring are enhancing their reliability and operational efficiency. Power transformers, which are critical for transmitting high-capacity electricity from large-scale renewable installations to urban centers, are also seeing robust growth, supported by advancements in insulation and cooling technologies.

The renewable energy transformers market from the hydro energy segment accounted for a 42% share in 2024 and is anticipated to grow at a CAGR of 8% by 2034. Expanding hydropower projects, along with increasing offshore and onshore wind installations, are key drivers for market growth. The demand for transformers designed to handle the fluctuating outputs of solar photovoltaic systems is also rising significantly.

The U.S. Renewable Energy Transformer Market generated USD 1.9 billion in 2024. With a growing adoption of solar and wind technologies, coupled with infrastructure modernization efforts and smart grid integration, the U.S. market is poised for sustained expansion.

Key companies operating in the Global Renewable Energy Transformer Market include Aditya Energy, ABC Transformers, GE Vernova, ACTOM, Acutran, AEP Group, Celme, Hammond Power Solutions, CG Power, Daelim, Deltron Electricals, Eaton, Elsewedy Electric, HD Hyundai Electric, Hitachi Energy, Hyosung Heavy Industries, MGM Transformers, Mitsubishi Electric, Ormazabal, Prolec Energy, Siemens Energy, Virginia Transformer, and WEG. These companies are prioritizing product innovation in energy efficiency and sustainability, incorporating advanced monitoring systems, and strategically expanding into emerging markets to meet the rising demand for renewable energy infrastructure.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's Analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Product, 2021 - 2034 (USD Million, ‘000 Units)

- 5.1 Key trends

- 5.2 Distribution transformer

- 5.3 Power transformer

- 5.4 Inverter duty transformer

- 5.5 Others

Chapter 6 Market Size and Forecast, By Cooling, 2021 - 2034 (USD Million, ‘000 Units)

- 6.1 Key trends

- 6.2 Dry type

- 6.3 Oil immersed

Chapter 7 Market Size and Forecast, By Rating, 2021 - 2034 (USD Million, ‘000 Units)

- 7.1 Key trends

- 7.2 ≤ 10 MVA

- 7.3 > 10 MVA to ≤ 100 MVA

- 7.4 > 100 MVA to ≤ 600 MVA

- 7.5 > 600 MVA

Chapter 8 Market Size and Forecast, By Application, 2021 - 2034 (USD Million, ‘000 Units)

- 8.1 Key trends

- 8.2 Hydro energy

- 8.3 Wind farm

- 8.4 Solar PV

- 8.5 Others

Chapter 9 Market Size and Forecast, By Region, 2021 - 2034 (USD Million, ‘000 Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 Russia

- 9.3.4 UK

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 Saudi Arabia

- 9.5.2 UAE

- 9.5.3 Qatar

- 9.5.4 Egypt

- 9.5.5 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 ABC Transformers

- 10.2 ACTOM

- 10.3 Acutran

- 10.4 Aditya Energy

- 10.5 AEP Group

- 10.6 Celme

- 10.7 CG Power

- 10.8 Daelim

- 10.9 Deltron Electricals

- 10.10 Eaton

- 10.11 Elsewedy Electric

- 10.12 GE Vernova

- 10.13 Hammond Power Solutions

- 10.14 HD Hyundai Electric

- 10.15 Hitachi Energy

- 10.16 Hyosung Heavy Industries

- 10.17 MGM Transformers

- 10.18 Mitsubishi Electric

- 10.19 Ormazabal

- 10.20 Prolec Energy

- 10.21 Siemens Energy

- 10.22 Virginia Transformer

- 10.23 WEG

可再生能源证书/信用额度(REC)市场-全球及区域分析:按应用、产品和地区划分-分析与预测(2025-2035)

可再生能源证书/信用额度(REC)市场-全球及区域分析:按应用、产品和地区划分-分析与预测(2025-2035) 再生能源保险市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年)

再生能源保险市场机会、成长驱动因素、产业趋势分析及预测(2025-2034年) 2032 年可再生能源创新市场预测:按组件、技术、应用、最终用户和地区进行的全球分析绿色/可再生能源市场预测至2032年:按能源来源、技术、应用、最终用户和地区分類的全球分析

2032 年可再生能源创新市场预测:按组件、技术、应用、最终用户和地区进行的全球分析绿色/可再生能源市场预测至2032年:按能源来源、技术、应用、最终用户和地区分類的全球分析 全球绿色电力市场(按技术、产量、安装类型和最终用户划分)预测 2025-2032

全球绿色电力市场(按技术、产量、安装类型和最终用户划分)预测 2025-2032 2025年全球节能设备市场报告2032年替代能源市场预测:按能源来源、最终用户和地区分類的全球分析2025年全球能源咨询市场报告2025年全球可再生能源保险市场报告

2025年全球节能设备市场报告2032年替代能源市场预测:按能源来源、最终用户和地区分類的全球分析2025年全球能源咨询市场报告2025年全球可再生能源保险市场报告 再生能源市场:产业趋势·全球预测 (~2035年):再生能源类型·用途·投资类型·企业类型·各地区

再生能源市场:产业趋势·全球预测 (~2035年):再生能源类型·用途·投资类型·企业类型·各地区