|

市场调查报告书

商品编码

1740931

侧装式垃圾车市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Side Loader Refuse Trucks Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

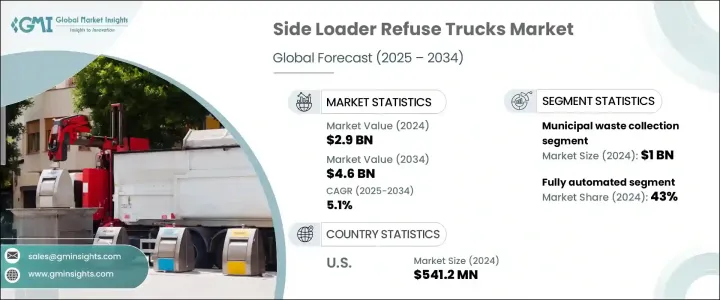

2024年,全球侧装式垃圾车市场规模达29亿美元,预计到2034年将以5.1%的复合年增长率成长,达到46亿美元。随着全球城市规模的不断扩大,对高效能、节省空间的垃圾收集车辆的需求也随之激增。城市发展必然带来人口密度的上升和固体垃圾量的增加,因此迫切需要能够在狭小空间内进行垃圾收集的系统。侧装式垃圾车凭藉其在狭窄道路和繁忙街道上的灵活机动性,已成为城市地区的首选解决方案。此外,侧装式垃圾车与标准垃圾箱相容,也使其成为致力于简化垃圾收集流程的市政当局的首选方案。城市中心正朝着更干净、更有效率的垃圾管理模式迈进,这大大加速了侧装式垃圾车的普及。

政府法规在这些车辆日益普及的过程中也发挥关键作用。更严格的环境和安全标准正促使地方政府和私人企业投资现代化的低排放技术。随着城市致力于改善空气品质和减少碳排放,由电动和混合动力系统驱动的侧装装载机正日益受到青睐。这些车辆不仅有助于实现环保目标,还能透过降低油耗和缩短维护时间来提高营运性能。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 29亿美元 |

| 预测值 | 46亿美元 |

| 复合年增长率 | 5.1% |

从应用角度来看,市场分为工业废弃物、市政废弃物、商业废弃物以及建筑和拆除废弃物。市政废弃物收集在2024年占据主导地位,市场价值约10亿美元,占市场份额的45%以上。随着都市化进程的加快,城市地区产生的废弃物持续增加,这反映在市政收集服务需求的增加。随着废物量的增加,市政当局开始使用侧装卡车来应对其卫生系统日益增长的压力。

这些卡车的自动化设计已被证明对寻求降低劳动成本的市政府尤其重要。凭藉自动化的臂架和箱体升降机构,侧装式装载机所需的操作员更少,从而更具成本效益和效率。这些卡车能够在极少的人工干预下持续不间断地收集垃圾,从而改善劳动力管理并提高生产力。市政府越来越多地采用此类技术,这些技术通常由公共资金或拨款支持,以提高其废弃物管理系统的效率。

就装载机製而言,市场细分为全自动、半自动和手动系统。 2024年,全自动侧装卡车占据市场主导地位,约占总市场份额的43%。这些卡车只需一名操作员即可完成所有核心功能,包括起重、装载和清空垃圾箱。这种自动化不仅有助于减少劳动力,还能加快收集流程、最大限度地减少停机时间并提高准确性。随着技术的不断进步,这些全自动系统在大型城市环境中变得越来越可靠和重要。

燃料类型是另一个关键的细分领域,涵盖柴油、电动、压缩天然气 (CNG)、混合动力和其他燃料类型。 2024 年,柴油卡车引领市场。儘管替代燃料日益普及,但对于许多市政当局和私营业者而言,柴油仍然是最实用、最具成本效益的选择。柴油卡车以其耐用性、易于维护和完善的加油基础设施而闻名。对于长途运输和重型作业,与电动或压缩天然气 (CNG) 驱动的替代燃料相比,柴油仍然具有无与伦比的可靠性和更低的前期成本。

就最终用户而言,市场细分为市政服务、专业废弃物处理商、私人废弃物管理公司和其他类型。市政服务在2024年占据主导地位。地方政府负责城市地区(尤其是人口密集的社区)的大部分废弃物收集工作。侧装卡车凭藉其紧凑的设计和自动化功能,能够有效地服务这些地区。由于能够获得政府补贴和预算拨款,市政当局能够更好地投资于更新、更具成本效益的废弃物收集技术,从而支持其环境目标。

从地理上看,北美占据了主要的市场份额,2024 年占超过 35%。光是美国一国的市场价值就达到了约 5.412 亿美元。美国庞大的城市人口,加上严格的州级法规,使得自动化和清洁的垃圾收集技术成为必要。垃圾收集部门正在增加对电动和混合动力车型的投资,以符合排放法规,同时降低整体营运成本。

该领域的主要製造商如今高度重视永续性,透过提供配备智慧自动化、电动传动系统和诊断功能的车型来竞争。能够提供低排放或零排放汽车的公司在实施绿色采购政策的地区(尤其是北美和欧洲)找到了更多机会。竞争优势在于能够提供兼具性能、燃油效率、安全性和环保合规性且经济高效的汽车。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原料及零件供应商

- 卡车和设备製造商

- 技术和远端资讯处理提供者

- 最终用途

- 利润率分析

- 川普政府关税的影响

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 技术与创新格局

- 专利分析

- 价格分析

- 地区

- 推进系统

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 都市化和人口成长

- 监管推动清洁高效的垃圾收集

- 私人废弃物管理公司的成长

- 垃圾车的技术进步

- 产业陷阱与挑战

- 初始成本高

- 维护和维修成本高

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按加载机制,2021 - 2034 年

- 主要趋势

- 全自动

- 半自动化

- 手动的

第六章:市场估计与预测:依产能,2021 - 2034 年

- 主要趋势

- 少于10,000磅

- 10,000 至 20,000 磅

- 20,000 至 30,000 磅

- 超过30,000磅

第七章:市场估计与预测:按燃料,2021 - 2034 年

- 主要趋势

- 柴油引擎

- 电的

- 天然气

- 杂交种

- 其他的

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 城市垃圾收集

- 工业废弃物收集

- 商业垃圾收集

- 建筑和拆除废弃物

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 市政服务

- 私人废弃物管理公司

- 专业废弃物处理人员

- 其他的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- Amrep

- Autocar

- Bridgeport Manufacturing

- Bucher Municipal

- BYD

- Curbtender

- Dennis Eagle

- FAUN Zoeller (UK)

- Foton Motor

- Freightliner (Daimler)

- Fujian Longma Environmental Sanitation Equipment

- Heil

- Isuzu

- Labrie Trucks

- Mack Trucks

- McNeilus Truck and Manufacturing

- New Way Refuse Trucks

- NTM

- Pak-Mor

- Peterbilt Motors Company

The Global Side Loader Refuse Trucks Market was valued at USD 2.9 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 4.6 billion by 2034. As cities around the world continue to expand, the demand for efficient and space-conscious waste collection vehicles has surged. Urban development naturally brings with it higher population densities and increased volumes of solid waste, creating an urgent need for systems that can handle waste collection in tight spaces. Side loader refuse trucks have become the go-to solution in urban areas, thanks to their ability to maneuver through narrow roads and busy streets. Their compatibility with standardized waste bins also makes them a preferred option for municipalities aiming to streamline collection processes. Urban centers are moving towards cleaner and more efficient waste management practices, which has significantly accelerated the adoption of side loader trucks.

Government regulations are also playing a critical role in the growing adoption of these vehicles. Stricter environmental and safety standards are pushing local authorities and private firms to invest in modern, low-emission technologies. Side loaders powered by electric and hybrid systems are gaining traction as cities aim to improve air quality and reduce carbon emissions. These vehicles not only help meet environmental goals but also improve operational performance by consuming less fuel and reducing maintenance time.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.9 Billion |

| Forecast Value | $4.6 Billion |

| CAGR | 5.1% |

In terms of application, the market is divided into industrial waste, municipal waste, commercial waste, and construction and demolition waste. Municipal waste collection dominated in 2024, with a market value of around USD 1 billion, representing over 45% of the market share. With rapid urbanization, waste generated in city areas continues to rise, and this increase is reflected in the higher demand for municipal collection services. As waste volumes grow, municipalities are turning to side loader trucks to handle rising pressure on their sanitation systems.

The automated design of these trucks has proven to be especially valuable for city governments looking to reduce labor costs. With automated arms and bin-lifting mechanisms, side loaders require fewer operators, making them more cost-effective and efficient. These trucks allow consistent and uninterrupted waste collection with minimal human intervention, leading to better workforce management and productivity gains. City governments are increasingly adopting such technologies, often supported by public funding or grants, to improve the effectiveness of their waste management systems.

When it comes to loading mechanisms, the market is segmented into fully automated, semi-automated, and manual systems. Fully automated side loader trucks led the market in 2024, holding around 43% of the total share. These trucks are capable of performing all core functions - including lifting, loading, and emptying bins - with just one operator. This automation not only helps reduce the labor force but also speeds up collection processes, minimizes downtime, and increases accuracy. As technology continues to advance, these fully automated systems are becoming more reliable and essential in large urban settings.

Fuel type is another critical segmentation, with diesel, electric, CNG, hybrid, and other fuel types in the mix. Diesel-powered trucks led the market in 2024. Despite the growing popularity of alternative fuels, diesel remains the most practical and cost-effective choice for many municipalities and private operators. Diesel trucks are known for their durability, easier maintenance, and well-established refueling infrastructure. For long-haul routes and heavy-duty operations, diesel continues to offer unmatched reliability and lower upfront costs compared to electric or CNG-powered alternatives.

In terms of end users, the market is segmented into municipal services, specialized waste handlers, private waste management companies, and others. Municipal services took the lead in 2024. Local governments handle the majority of waste collection in urban areas, especially in densely populated neighborhoods. Side loader trucks serve these regions efficiently due to their compact design and automated capabilities. With access to government subsidies and budget allocations, municipalities are better positioned to invest in updated and cost-efficient waste collection technologies that support their environmental goals.

Geographically, North America held a major share of the market, accounting for over 35% in 2024. The U.S. alone reached a market value of approximately USD 541.2 million. The country's high urban population, combined with strict state-level regulations, has made automated and clean waste collection technologies a necessity. Waste collection authorities are increasingly investing in electric and hybrid models to comply with emission mandates while reducing overall operating costs.

Major manufacturers in this space are now focusing heavily on sustainability, competing by offering models with smart automation, electric drivetrains, and diagnostic features. Companies that can provide low or zero-emission vehicles are finding more opportunities in regions with green procurement policies, especially in North America and Europe. The competitive edge lies in offering vehicles that balance performance, fuel efficiency, safety, and environmental compliance in a cost-effective package.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material and component supplier

- 3.2.2 Truck and equipment manufacturer

- 3.2.3 Technology and telematics providers

- 3.2.4 End use

- 3.3 Profit margin analysis

- 3.4 Impact of trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook & future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Price analysis

- 3.7.1 Region

- 3.7.2 Propulsion

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Urbanization and population growth

- 3.10.1.2 Regulatory push for clean and efficient waste collection

- 3.10.1.3 Growth of private waste management companies

- 3.10.1.4 Technological advancements in refuse trucks

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost

- 3.10.2.2 High maintenance and repair costs

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter's analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Loading Mechanism, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Fully automated

- 5.3 Semi-automated

- 5.4 Manual

Chapter 6 Market Estimates & Forecast, By Capacity, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Less than 10,000 lbs

- 6.3 10,000 to 20,000 lbs

- 6.4 20,000 to 30,000 lbs

- 6.5 More than 30,000 lbs

Chapter 7 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Diesel

- 7.3 Electric

- 7.4 CNG

- 7.5 Hybrid

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Municipal waste collection

- 8.3 Industrial waste collection

- 8.4 Commercial waste collection

- 8.5 Construction and demolition waste

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Municipal services

- 9.3 Private waste management companies

- 9.4 Specialized waste handlers

- 9.5 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Amrep

- 11.2 Autocar

- 11.3 Bridgeport Manufacturing

- 11.4 Bucher Municipal

- 11.5 BYD

- 11.6 Curbtender

- 11.7 Dennis Eagle

- 11.8 FAUN Zoeller (UK)

- 11.9 Foton Motor

- 11.10 Freightliner (Daimler)

- 11.11 Fujian Longma Environmental Sanitation Equipment

- 11.12 Heil

- 11.13 Isuzu

- 11.14 Labrie Trucks

- 11.15 Mack Trucks

- 11.16 McNeilus Truck and Manufacturing

- 11.17 New Way Refuse Trucks

- 11.18 NTM

- 11.19 Pak-Mor

- 11.20 Peterbilt Motors Company

卡车后部液压缓速器 - 全球市场份额和排名、总销售量和需求预测(2025-2031 年)

卡车后部液压缓速器 - 全球市场份额和排名、总销售量和需求预测(2025-2031 年) 卡车后液压缓速器市场按煞车类型、安装方法、卡车类型和分销管道划分 - 2025-2030 年全球预测

卡车后液压缓速器市场按煞车类型、安装方法、卡车类型和分销管道划分 - 2025-2030 年全球预测 后装载式垃圾车市场报告:趋势、预测和竞争分析(至 2030 年)

后装载式垃圾车市场报告:趋势、预测和竞争分析(至 2030 年) 后装载卡车市场规模 - 按燃料(电动、汽油、柴油)、按技术(手动、自动、半自动)、按容量(10 吨以下、10-20 吨、20 吨以上)、最终用户行业& 预测,2024 - 2032侧装卡车市场规模 - 按技术(手动、自动、半自动)、按容量(最多 10 吨、10-20 吨、20 吨以上)、按最终用户(废物管理、建筑、物流和运输) ,按燃料和预测,2024 - 2032

后装载卡车市场规模 - 按燃料(电动、汽油、柴油)、按技术(手动、自动、半自动)、按容量(10 吨以下、10-20 吨、20 吨以上)、最终用户行业& 预测,2024 - 2032侧装卡车市场规模 - 按技术(手动、自动、半自动)、按容量(最多 10 吨、10-20 吨、20 吨以上)、按最终用户(废物管理、建筑、物流和运输) ,按燃料和预测,2024 - 2032