|

市场调查报告书

商品编码

1740944

汽车多模式互动开发市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Multimodal Interaction Development Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

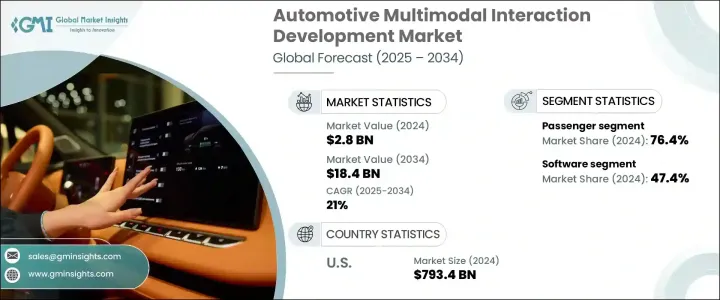

2024 年,全球汽车多模态互动开发市场规模达 28 亿美元,预计到 2034 年将以 21% 的复合年增长率成长,达到 184 亿美元。这得益于下一代汽车对智慧用户介面的强劲需求以及互联出行解决方案的广泛应用。随着汽车创新的加速,多模式互动正成为车载技术的核心,而人机之间的无缝通讯定义了未来的出行方式。对个人化、增强安全性和直觉控制的日益增长的需求正在重塑驾驶员与车辆的互动方式。人工智慧、先进的感测器整合和即时资料处理正在融合,以创建高度自适应的车载环境。随着自动驾驶、智慧城市生态系统和数位互联的转变,汽车製造商竞相嵌入能够提供自然、反应迅速的使用者体验的系统。全球各地的汽车製造商和技术供应商都在大力投资研发,以完善人机协同,确保车辆不仅能准确回应,还能预测驾驶者的需求。多模式互动——涵盖语音、触摸、手势和情绪检测——将大规模重新定义驾驶的便利性和安全性。

在全球范围内,出行计画和数位转型专案正在推动智慧交通基础设施的投资,旨在降低驾驶复杂性。各国政府正大力支持人机介面 (HMI) 技术的进步,以提升交通管理、安全性和驾驶满意度。语音指令、手势辨识和脸部认证等非接触式系统日益普及,这正在彻底改变车载体验。汽车製造商正在迅速采用能够理解驾驶员行为、环境和情绪的自适应系统,并将多模式技术整合到自动驾驶和半自动驾驶平台中。亚洲正将自己定位为强大的催化剂,为在不断扩张的市场中部署下一代互动出行解决方案提供监管激励和政策支援。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 28亿美元 |

| 预测值 | 184亿美元 |

| 复合年增长率 | 21% |

以组件计算,软体平台细分市场在2024年占据47.4%的份额,预计到2034年将以21.8%的复合年增长率成长。人工智慧功能日益复杂,推动了对高阶演算法、语音辨识工具和情境感知介面的需求。软体平台是多模式系统的大脑,支援跨通路通讯、无线更新,并支援高度客製化的驾驶环境。城市地区和互联出行生态系统正迎来旨在建立可扩展智慧互动框架的投资激增。

按车型划分,乘用车在2024年占据市场主导地位,市占率达76.4%。这得益于产量的提升、人机介面(HMI)系统的强势集成,以及消费者对高端科技驾驶体验日益增长的需求。电动车的蓬勃发展以及高级驾驶辅助系统 (ADAS) 的普及,正推动着汽车製造商整合多模式解决方案,以提升舒适性、安全性和直觉式操控性。

2024年,美国汽车多模态互动开发市场占63%的市场份额,贡献了7.934亿美元的市场规模。这一成长得益于美国先进的汽车研发现状系统、对自动驾驶汽车专案的强劲投资,以及科技公司和汽车製造商之间的深度合作。在联邦政府和私人资金的支持下,美国各地城市正积极地成为尖端人机互动技术的实际测试平台。

引领市场的主要参与者包括华为、地平线、德赛西威、Cerence、博泰、百度、腾讯、安波福、科大讯飞和大陆集团。各公司正透过策略合作伙伴关係、与人工智慧开发商成立合资企业、加强研发力度以及开发自主研发的人工智慧平台来巩固其市场地位。对区域扩张、使用者体验在地化以及云端智慧整合的重视,持续推动整个领域的创新。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 零件製造商

- 技术提供者

- 软体开发者

- 最终用途

- 川普政府关税的影响

- 贸易影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(客户成本)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 贸易影响

- 利润率分析

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 自动驾驶和半自动驾驶汽车的兴起

- 越来越关注车载安全(DMS、ADAS)

- OEM和一级供应商对智慧座舱系统的投资

- 持续的技术进步

- 产业陷阱与挑战

- 开发和整合成本高

- 使用者体验设计的复杂性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商业的

第七章:市场估计与预测:依互动,2021 - 2034 年

- 主要趋势

- 语音辨识

- 手势识别

- 脸部辨识

- 触控式介面

- 其他的

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第九章:公司简介

- ADAYO

- AISpeech

- Aptiv

- ArcSoft Technology

- Baidu

- Banma Network

- Cerence

- Cipia Vision

- Continental

- Desay SV

- Hikvision

- Horizon Robotics

- Huawei

- iFlytek

- Joyson Electronics

- Shenzhen Minieye Intelligent Technology (MINIEYE)

- Shanghai PATEO Electronic Equipment Manufacturing

- SenseTime

- Tencent

- ThunderSoft

The Global Automotive Multimodal Interaction Development Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 21% to reach USD 18.4 billion by 2034, driven by the surging demand for intelligent user interfaces in next-gen vehicles and the widespread adoption of connected mobility solutions. As automotive innovation accelerates, multimodal interaction is becoming the centerpiece of in-vehicle technology, where seamless communication between humans and machines defines the future of mobility. The growing need for personalization, enhanced safety, and intuitive control is reshaping how drivers interact with vehicles. Artificial intelligence, advanced sensor integration, and real-time data processing are all converging to create highly adaptive in-vehicle environments. With the shift toward autonomous driving, smart city ecosystems, and digital connectivity, automakers are racing to embed systems that deliver a natural, responsive user experience. Around the globe, automotive manufacturers and tech providers are investing heavily in R&D to refine human-machine synergy, ensuring vehicles not only respond accurately but also anticipate driver needs. Multimodal interaction-spanning voice, touch, gesture, and emotion detection-is poised to redefine driving convenience and safety at scale.

Globally, mobility initiatives and digital transformation programs are pushing investments in smart transport infrastructure aimed at reducing driving complexities. Governments are endorsing advancements in human-machine interface (HMI) technologies to boost traffic management, safety, and driver satisfaction. The growing transition toward touchless systems, including voice commands, gesture recognition, and facial authentication, is transforming in-vehicle experiences. Automakers are rapidly embracing adaptive systems that understand driver behavior, environment, and emotions, integrating multimodal technologies into both autonomous and semi-autonomous platforms. Asia is positioning itself as a strong catalyst, offering regulatory incentives and policy support for deploying next-generation interactive mobility solutions across expanding markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $18.4 Billion |

| CAGR | 21% |

Based on components, the software platforms segment held a 47.4% share in 2024 and is anticipated to grow at a CAGR of 21.8% through 2034. The rising complexity of AI-powered features is fueling the demand for advanced algorithms, speech recognition tools, and context-aware interfaces. Software platforms serve as the brain of multimodal systems, enabling cross-channel communication, delivering over-the-air updates, and supporting highly customized driving environments. Urban areas and connected mobility ecosystems are seeing a surge in investments aimed at building scalable, intelligent interaction frameworks.

By vehicle type, passenger vehicles dominated the market in 2024 with a 76.4% share, propelled by rising production rates, strong integration of HMI systems, and escalating consumer demand for sophisticated, tech-driven driving experiences. The boom in electric vehicles and the adoption of advanced driver-assistance systems (ADAS) are driving OEMs to integrate multimodal solutions that enhance comfort, safety, and intuitive control.

The United States Automotive Multimodal Interaction Development Market held a 63% share in 2024, contributing USD 793.4 million. This growth stems from the country's advanced automotive R&D ecosystem, robust investments in autonomous vehicle initiatives, and deep collaboration between tech firms and automakers. Cities across the U.S. are actively serving as real-world test beds for cutting-edge HMI technologies backed by federal initiatives and private funding.

Key players leading the market include Huawei, Horizon Robotics, Desay SV, Cerence, PATEO, Baidu, Tencent, Aptiv, iFlytek, and Continental. Companies are strengthening their market presence through strategic partnerships, joint ventures with AI developers, expanded R&D efforts, and proprietary AI platform developments. Emphasis on regional expansion, localization of user experiences, and integration of cloud-based intelligence continues to drive innovation across the space.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component manufacturers

- 3.2.2 Technology providers

- 3.2.3 Software developers

- 3.2.4 End use

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Trade impact

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on industry

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.2.1.1 Price volatility in key materials

- 3.3.2.1.2 Supply chain restructuring

- 3.3.2.1.3 Production cost implications

- 3.3.2.2 Demand-side impact (Cost to customers)

- 3.3.2.2.1 Price transmission to end markets

- 3.3.2.2.2 Market share dynamics

- 3.3.2.2.3 Consumer response patterns

- 3.3.2.1 Supply-side impact (raw materials)

- 3.3.3 Key companies impacted

- 3.3.4 Strategic industry responses

- 3.3.4.1 Supply chain reconfiguration

- 3.3.4.2 Pricing and product strategies

- 3.3.4.3 Policy engagement

- 3.3.5 Outlook & future considerations

- 3.3.1 Trade impact

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rise of autonomous and semi-autonomous vehicles

- 3.9.1.2 Increasing focus on in-vehicle safety (DMS, ADAS)

- 3.9.1.3 OEM and Tier-1 investment in intelligent cockpit systems

- 3.9.1.4 Ongoing technological advancements

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High development & integration cost

- 3.9.2.2 Complexity in user experience design

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Hardware

- 5.3 Software

- 5.4 Services

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial

Chapter 7 Market Estimates & Forecast, By Interaction, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Speech recognition

- 7.3 Gesture recognition

- 7.4 Facial recognition

- 7.5 Touch-based interfaces

- 7.6 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 ADAYO

- 9.2 AISpeech

- 9.3 Aptiv

- 9.4 ArcSoft Technology

- 9.5 Baidu

- 9.6 Banma Network

- 9.7 Cerence

- 9.8 Cipia Vision

- 9.9 Continental

- 9.10 Desay SV

- 9.11 Hikvision

- 9.12 Horizon Robotics

- 9.13 Huawei

- 9.14 iFlytek

- 9.15 Joyson Electronics

- 9.16 Shenzhen Minieye Intelligent Technology (MINIEYE)

- 9.17 Shanghai PATEO Electronic Equipment Manufacturing

- 9.18 SenseTime

- 9.19 Tencent

- 9.20 ThunderSoft

2025-2029年全球汽车人工智慧市场

2025-2029年全球汽车人工智慧市场 2025-2029年全球封闭式源平台模型市场

2025-2029年全球封闭式源平台模型市场 汽车人工智慧维修服务市场,按服务类型、按技术、按车辆类型、按部署模式、按应用、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测

汽车人工智慧维修服务市场,按服务类型、按技术、按车辆类型、按部署模式、按应用、按国家/地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测 汽车量子点背光单元市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

汽车量子点背光单元市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 全球行动人工智慧市场 2025-2029

全球行动人工智慧市场 2025-2029 汽车人工智慧市场报告(按组件、技术、流程、应用和地区)2025-2033

汽车人工智慧市场报告(按组件、技术、流程、应用和地区)2025-2033 2025年汽车元宇宙全球市场报告2025年汽车和运输领域人工智慧全球市场报告2025年汽车量子计算全球市场报告2025年遥感探测设备(RSD)车辆智慧系统全球市场报告

2025年汽车元宇宙全球市场报告2025年汽车和运输领域人工智慧全球市场报告2025年汽车量子计算全球市场报告2025年遥感探测设备(RSD)车辆智慧系统全球市场报告