|

市场调查报告书

商品编码

1740995

蜂窝车联网 (C-V2X) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Cellular Vehicle-to-Everything (C-V2X) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

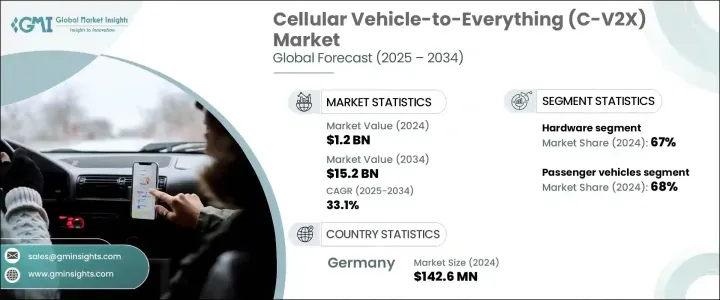

2024 年全球蜂窝车联网市场规模达 12 亿美元,预计到 2034 年将以 33.1% 的复合年增长率成长,达到 152 亿美元。这项快速扩张主要得益于对先进道路安全技术日益增长的需求,以及对高效能智慧交通管理系统日益增长的需求。由于道路交通事故仍然是全球关注的重大议题,C-V2X 技术的采用激增。这项创新促进了车辆、基础设施和行人之间的即时通信,有助于降低碰撞风险并简化交通流量。随着城市中心转向更智慧、更安全的交通解决方案,C-V2X 在实现互联交通生态系统、提高安全性和便利性方面正变得不可或缺。它在自动驾驶汽车的发展中也发挥着关键作用,确保它们在日益复杂的环境中安全且有效率地运作。

C-V2X 是自动驾驶汽车和网路连线汽车的基础。透过允许车辆交换有关其位置、速度和意图的即时资料,它支援更安全、更协调的驾驶体验。这种持续的资料传输对于自动驾驶汽车的安全运行至关重要,有助于其应对路况、危险以及视线范围之外的周边交通状况。仅靠雷达和摄影机等传统感测器无法达到这种环境感知水准。 C-V2X 可以实现更平稳的车道变换、更安全的交叉路口导航和优化路线。它甚至可以减少交通拥堵,尤其是在复杂的城市或高速公路环境中。该市场的快速成长反映了汽车产业对更高自动化程度的追求以及对增强车辆安全性日益增长的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 12亿美元 |

| 预测值 | 152亿美元 |

| 复合年增长率 | 33.1% |

就组件而言,C-V2X 市场分为硬体和软体两部分,其中硬体在 2024 年占据 67% 的主导市场份额。这个细分市场之所以如此突出,是因为硬体在实现 V2X 功能方面发挥着至关重要的作用。车载单元、感测器、天线和路边基础设施等设备对于即时资料交换至关重要。汽车製造商越来越多地将这些技术融入车辆,以提高自动化、导航和安全性。公共和私营部门对互联基础设施的持续投资正在推动硬体细分市场的成长。

乘用车在2024年占68%的市场份额,引领市场,预计复合年增长率将达到33.5%。高级驾驶辅助系统 (ADAS) 在乘用车中的广泛应用是推动 C-V2X 技术需求的关键因素。这些系统利用 C-V2X 提供的额外资料来增强危险侦测、提升态势感知能力,并增强车辆整体安全性。

在德国,C-V2X 市场规模达 1.426 亿美元,2024 年占 27%。德国在市场上的领先地位得益于其先进的汽车生态系统、广泛的 5G 部署以及政府大力推动智慧交通系统的倡议。这些政策,加上汽车和电信业的协同创新,使德国成为欧洲大规模 C-V2X 测试的首选。

市场的主要参与者包括英特尔、罗伯特·博世、高通、ATandT、华为技术、是德科技、英飞凌科技、大陆集团、中兴通讯和电装。为了保持竞争力,这些公司专注于与汽车製造商、电信营运商和基础设施公司建立策略合作伙伴关係。他们在 5G 整合、智慧城市试点计画以及参与标准化计画的投资,是加速 C-V2X 系统商业化的关键。此外,各公司正大力投入研发,以降低延迟、提高覆盖范围并增强互通性,同时不断扩展产品线,以满足乘用车和商用车平台的需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- C-V2X硬体供应商

- C-V2X软体供应商

- 汽车原厂设备製造商

- 电信服务供应商

- 最终用途

- 利润率分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 其他国家的报復措施

- 对产业的影响

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 受影响的主要公司

- 汽车OEM

- 电信设备供应商

- 半导体和模组供应商

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 展望与未来考虑

- 对贸易的影响

- 技术与创新格局

- 专利分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 全球道路交通事故数量不断上升

- 自动驾驶汽车的普及率不断提高

- 对更安全的道路交通的需求不断增长

- 车辆远端资讯处理日益普及

- 产业陷阱与挑战

- 网路安全和隐私问题

- 缺乏蜂窝信号覆盖

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依通讯方式,2021 - 2034 年

- 主要趋势

- 车对人 (V2P)

- 车辆到基础设施 (V2I)

- 车对网路(V2N)

- 车对车 (V2V)

第六章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 硬体

- 车载单元 (OBU)

- 路边单元 (RSU)

- 天线

- 通讯模组

- 软体

- 交通管理软体

- 车队管理系统

第七章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型商用车(LCV)

- 中型商用车(MCV)

- 重型商用车(HCV)

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 车队管理

- 自动驾驶

- 避免碰撞

- 智慧交通系统

- 停车管理系统

- 其他的

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- AT&T

- Autotalks

- Cohda Wireless

- Commsignia

- Continental

- Denso

- Ficosa International

- Huawei Technologies

- Infineon Technologies

- Intel

- Keysight Technologies

- Nokia

- NTT DOCOMO

- Qualcomm

- Quectel Wireless Solutions

- Robert Bosch

- Rohde & Schwarz

- Savari

- Shenzhen Genvict Technologies

- ZTE Corporation

The Global Cellular Vehicle-To-Everything Market was valued at USD 1.2 billion in 2024 and is projected to grow at a CAGR of 33.1% to reach USD 15.2 billion by 2034. This rapid expansion is primarily driven by the increasing demand for advanced road safety technologies and the growing need for efficient, intelligent traffic management systems. With road accidents remaining a significant concern worldwide, the adoption of C-V2X technology has surged. This innovation facilitates real-time communication between vehicles, infrastructure, and pedestrians, helping to reduce collision risks and streamline traffic flow. As urban centers shift toward smarter, safer transportation solutions, C-V2X is becoming integral in enabling a connected transport ecosystem that enhances both safety and convenience. It also plays a critical role in the evolution of autonomous vehicles, ensuring they operate safely and efficiently within increasingly complex environments.

C-V2X is foundational for both autonomous and connected vehicles. By allowing vehicles to exchange real-time data regarding their position, speed, and intent, it supports safer and more coordinated driving experiences. This continuous data transmission is vital for the safe operation of autonomous vehicles, helping them respond to road conditions, hazards, and surrounding traffic far beyond the line of sight. Traditional sensors like radar and cameras alone can not achieve this level of environmental awareness. C-V2X facilitates smoother lane changes, safer intersection navigation, and optimized routing. It can even reduce congestion, particularly in complex urban or highway settings. The market's rapid growth reflects the broader automotive industry's push toward increased automation and the evolving need for enhanced vehicle safety.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $15.2 Billion |

| CAGR | 33.1% |

In terms of components, the C-V2X market is divided into hardware and software, with hardware holding a dominant 67% market share in 2024. This segment's prominence is due to the essential role that hardware plays in enabling V2X functionality. Devices such as on-board units, sensors, antennas, and roadside infrastructure are integral for real-time data exchange. Automotive manufacturers are increasingly incorporating these technologies into vehicles to improve automation, navigation, and safety. The continued investment in connected infrastructure by both public and private sectors is fueling the growth of the hardware segment.

Passenger vehicles led the market with a 68% share in 2024 and are expected to grow at a CAGR of 33.5%. The widespread adoption of advanced driver-assistance systems (ADAS) in passenger cars has been a key factor driving demand for C-V2X technology. These systems leverage the additional data provided by C-V2X to enhance hazard detection, improve situational awareness, and strengthen overall vehicle safety.

In Germany, the C-V2X market generated USD 142.6 million, holding a 27% share in 2024. The country's leadership in the market can be attributed to its advanced automotive ecosystem, widespread 5G deployment, and robust government initiatives promoting intelligent transportation systems. These policies, alongside collaborative innovation across the automotive and telecommunications sectors, make Germany a prime location for large-scale C-V2X testing in Europe.

Key players in the market include Intel, Robert Bosch, Qualcomm, ATandT, Huawei Technologies, Keysight Technologies, Infineon Technologies, Continental, ZTE, and Denso. To stay competitive, these companies focus on strategic partnerships with automakers, telecom providers, and infrastructure firms. Their investments in 5G integration, smart city pilot projects, and participation in standardization initiatives are key to accelerating the commercialization of C-V2X systems. Additionally, significant RandD efforts are being made to enhance latency, coverage, and interoperability while companies continue to expand their product offerings to cater to both passenger and commercial vehicle platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 C-V2X hardware suppliers

- 3.2.2 C-V2X software suppliers

- 3.2.3 Automotive OEMs

- 3.2.4 Telecom service providers

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.3.1 Automotive OEM

- 3.4.3.2 Telecom equipment providers

- 3.4.3.3 Semiconductor and module suppliers

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising number road accidents across the globe

- 3.9.1.2 Growing adoption of autonomous vehicles

- 3.9.1.3 Rising demand for safer road travel

- 3.9.1.4 Growing popularity of vehicle telematics

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Network security and privacy issues

- 3.9.2.2 Lack of cellular coverage

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Communication, 2021 - 2034 ($Bn)

- 5.1 Key trends

- 5.2 Vehicle-to-Person (V2P)

- 5.3 Vehicle-to-Infrastructure (V2I)

- 5.4 Vehicle-to-Network (V2N)

- 5.5 Vehicle-to-Vehicle (V2V)

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn)

- 6.1 Key trends

- 6.2 Hardware

- 6.2.1 On-Board Units (OBUs)

- 6.2.2 Roadside Units (RSUs)

- 6.2.3 Antennas

- 6.2.4 Communication modules

- 6.3 Software

- 6.3.1 Traffic management software

- 6.3.2 Fleet management systems

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Medium Commercial Vehicles (MCV)

- 7.3.3 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn)

- 8.1 Key trends

- 8.2 Fleet management

- 8.3 Autonomous driving

- 8.4 Collision avoidance

- 8.5 Intelligent traffic systems

- 8.6 Parking management systems

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 AT&T

- 10.2 Autotalks

- 10.3 Cohda Wireless

- 10.4 Commsignia

- 10.5 Continental

- 10.6 Denso

- 10.7 Ficosa International

- 10.8 Huawei Technologies

- 10.9 Infineon Technologies

- 10.10 Intel

- 10.11 Keysight Technologies

- 10.12 Nokia

- 10.13 NTT DOCOMO

- 10.14 Qualcomm

- 10.15 Quectel Wireless Solutions

- 10.16 Robert Bosch

- 10.17 Rohde & Schwarz

- 10.18 Savari

- 10.19 Shenzhen Genvict Technologies

- 10.20 ZTE Corporation

2026年全球蜂窝车对车通讯市场报告

2026年全球蜂窝车对车通讯市场报告 车辆道路云端协作平台市场:按组件、通讯技术、服务类型、部署模式、应用程式和最终用户划分,全球预测(2026-2032年)

车辆道路云端协作平台市场:按组件、通讯技术、服务类型、部署模式、应用程式和最终用户划分,全球预测(2026-2032年) 蜂窝车联网市场分析及至2035年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分

蜂窝车联网市场分析及至2035年预测:按类型、产品类型、服务、技术、组件、应用、部署类型、最终用户和功能划分 全球蜂窝车联网(C-V2X)市场规模、份额、趋势和成长分析报告(2026-2034)

全球蜂窝车联网(C-V2X)市场规模、份额、趋势和成长分析报告(2026-2034) 车辆·道路·云端整合/C-V2X产业(2025年)2026 年至 2032 年蜂窝车联网 (C-V2X) 市场(按组件、通讯类型、应用、车辆类型和地区划分)

车辆·道路·云端整合/C-V2X产业(2025年)2026 年至 2032 年蜂窝车联网 (C-V2X) 市场(按组件、通讯类型、应用、车辆类型和地区划分) 蜂窝车联网市场,按通讯类型、按应用、按组件、按车辆类型、按国家和地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测C-V2X 测试的全球市场成长机会(2024-2030 年)C-V2X和CVIS产业(2024年)

蜂窝车联网市场,按通讯类型、按应用、按组件、按车辆类型、按国家和地区划分 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测C-V2X 测试的全球市场成长机会(2024-2030 年)C-V2X和CVIS产业(2024年)