|

市场调查报告书

商品编码

1741049

自动停车系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automated Parking System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

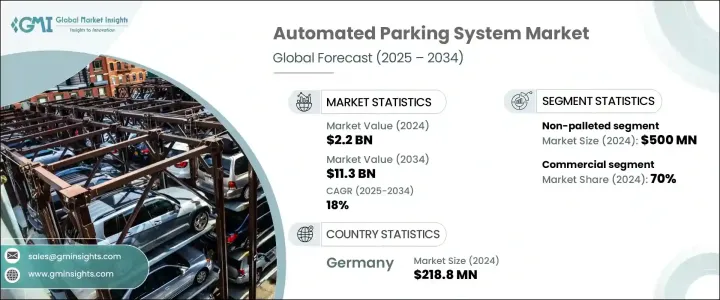

2024 年全球自动停车系统市场价值为 22 亿美元,预计到 2034 年将以 18% 的复合年增长率增长至 113 亿美元。受快速城市化、人口稠密城市停车位有限以及对智慧节省空间基础设施日益增长的需求的推动,该行业正在经历显着增长。随着汽车数量的增加和房地产的萎缩,城市面临越来越大的压力,需要更有效地管理空间。自动停车系统正在成为一种前瞻性的解决方案,它透过优化土地利用、简化交通流量和减少碳排放来应对这些挑战。这些系统提供了一种紧凑、高效的车辆存放方法,减少了对人工干预的依赖。因此,它们的部署正在扩展到各种城市应用领域——从住宅和商业开发项目到医院和交通枢纽。

自动停车系统因其能够增强安全性、提高空间利用率并最大限度地减少环境影响而日益普及。它们融合了先进的自动化和机器人技术,实现了车辆的智慧移动和储存。多层堆迭、自动车辆处理和车位管理等功能使这些系统既省时又环保。越来越多的开发商和物业经理开始采用这些系统,以降低营运成本、在有限的空间内增加停车容量,并为用户提供优质的体验。随着永续城市基础设施和智慧城市计画的日益关注,这些系统也进一步刺激了需求,因为这些系统与全球致力于实现更清洁、更有效率的城市交通的努力相契合。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 22亿美元 |

| 预测值 | 113亿美元 |

| 复合年增长率 | 18% |

就平台而言,市场细分为托盘式和非托盘式系统。非托盘式系统在2024年以约5亿美元的收入占据市场主导地位。该细分市场的主导地位归功于其节省空间的设计和更快的车辆检索能力,这在交通繁忙的大都市地区尤其重要。与托盘式系统不同,非托盘系统无需支撑平台,而是使用机器人和传送带系统直接移动车辆,从而简化了机械设置,并允许在狭窄的城市布局中灵活安装。商业建筑、机场和高层住宅开发项目对高吞吐量解决方案的需求正在增长。

从终端用户的角度来看,市场分为住宅和商业应用两大类别。 2024年,商业领域占据了70%的市场份额,这主要得益于办公大楼、零售中心、医院和饭店场所的采用。自动停车能够提升容量、缓解拥堵,并在繁忙环境中提供更快的车辆出入,这些场所将受益匪浅。城市拥挤和高昂的土地成本正促使企业投资垂直或地下停车场,以充分利用有限的空间。此外,自动停车与智慧建筑技术和增强型安防系统的融合,使其成为商业开发商眼中极具吸引力的选择。

市场也按类型划分,其中半自动化系统在2024年占据主要份额。其吸引力在于成本效益、快速设定和易用性,适用于住宅和商业领域的各种应用。这些系统在全自动和手动控制之间实现了平衡,无需像全自动系统那样进行高额的前期投资,即可提供增强的使用者体验。其低维护要求和用户友好的功能使其广受欢迎。

在系统结构方面,自动导引车 (AGV) 细分市场在 2024 年引领全球市场,创造了最大的收入份额。 AGV 系统适应性强,能够精准导航复杂的布局,是拥挤的城市环境和大型商业项目的理想选择。 AGV 系统能够无缝整合到现有基础设施中,同时提供高度的自动化和灵活性,使其成为应对现代停车挑战的首选解决方案。 AGV 尤其适用于那些对吞吐量和空间利用率最大化至关重要的环境。

就产品供应而言,硬体在2024年占据了自动停车系统市场的主导地位,占据了全球收入的最大份额。这是因为感测器、升降机、自动导引车(AGV)和传送系统等实体组件至关重要,它们构成了任何自动停车操作的核心。随着系统日益复杂,对耐用、高性能硬体的需求持续成长,尤其是在需要长期可靠性和高容量处理的专案中。

从地区来看,德国以2024年2.188亿美元的收入领先欧洲市场,预计到2034年复合年增长率将达到16.9%。德国强大的汽车工业、对智慧城市项目的投资以及先进的城市基础设施,为其在该领域的领先地位做出了重要贡献。此外,全球各地的企业都在透过投资研发、策略合作伙伴关係和尖端製造技术来扩大其影响力。市场领导者专注于模组化系统设计、能源效率以及人工智慧和物联网技术的集成,以提升用户体验和环境绩效。这些创新为下一代智慧永续停车解决方案奠定了基础。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 硬体提供者

- 软体供应商

- 服务提供者

- 技术提供者

- 最终用途

- 利润率分析

- 供应商格局

- 川普政府关税的影响

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 对贸易的影响

- 技术与创新格局

- 专利分析

- 监管格局

- 成本細項分析

- 重要新闻和倡议

- 衝击力

- 成长动力

- 北美和欧洲的自动驾驶汽车数量不断增加

- 都市化进程快速成长

- 亚太和中东地区智慧城市计画不断涌现

- 停车系统技术进步日新月异

- 产业陷阱与挑战

- 开发成本高

- 维护复杂且停机风险

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 全自动

- 半自动化

第六章:市场估计与预测:依结构,2021 - 2034 年

- 主要趋势

- AGV系统

- 筒仓系统

- 塔式系统

- 轨道引导车(RGC)系统

- 谜题系统

- 穿梭系统

第七章:市场估计与预测:依供应量,2021 - 2034 年

- 主要趋势

- 硬体

- 软体

- 服务

第八章:市场估计与预测:依平台,2021 - 2034 年

- 主要趋势

- 托盘

- 非托盘

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 住宅

- 商业的

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 南非

- 沙乌地阿拉伯

第 11 章:公司简介

- AutoMotion Parking

- City Lift Parking

- Dayang Parking

- EITO&GLOBAL

- Fata Automation

- IHI

- Klaus Multiparking

- Lodgie

- MHE Demag

- Park Assist

- Parkmatic

- ParkPlus

- Robotic Parking

- Serva Transport

- Skyline Parking

- Stolzer Parking

- TAPS

- Unitronics

- Westfalia Parking

- Wohr Parking

The Global Automated Parking System Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 18% to reach USD 11.3 billion by 2034. The industry is experiencing a significant surge, driven by rapid urbanization, limited availability of parking in densely populated cities, and a growing need for smart, space-saving infrastructure. With rising vehicle numbers and shrinking real estate, cities are facing mounting pressure to manage space more efficiently. Automated parking systems are emerging as a forward-thinking solution that tackles these challenges by optimizing land usage, streamlining traffic flow, and reducing carbon emissions. These systems provide a compact, highly efficient approach to vehicle storage with reduced reliance on human intervention. As a result, their deployment is expanding across a wide range of urban applications-from residential and commercial developments to hospitals and transport hubs.

Automated parking systems are gaining popularity due to their ability to enhance safety, improve space utilization, and minimize environmental impact. They incorporate advanced automation and robotics, allowing for intelligent vehicle movement and storage. Features such as multi-level stacking, automated vehicle handling, and slot management make these systems both time-efficient and environmentally friendly. Developers and property managers are increasingly turning to these systems to reduce operational costs, increase parking capacity in a confined footprint, and offer a premium experience to users. The rising focus on sustainable urban infrastructure and smart city initiatives is further fueling demand, as these systems align with global efforts toward cleaner, more efficient urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $11.3 Billion |

| CAGR | 18% |

In terms of platform, the market is segmented into palleted and non-palleted systems. The non-palleted category led the market with approximately USD 500 million in revenue in 2024. This segment's dominance is attributed to its space-saving design and quicker vehicle retrieval capabilities, which are especially important in high-traffic metropolitan areas. Unlike palleted systems, non-palleted ones eliminate the need for a supporting platform and use robotics and conveyor systems to move vehicles directly, simplifying the mechanical setup and allowing for flexible installation in tight urban layouts. Demand is growing in commercial buildings, airports, and high-rise residential developments where high-throughput solutions are essential.

From an end-user perspective, the market is split between residential and commercial applications. In 2024, the commercial segment held a substantial 70% market share, driven by adoption in office buildings, retail centers, hospitals, and hospitality venues. These settings benefit immensely from automated parking's ability to enhance capacity, reduce congestion, and provide quicker access to vehicles in busy environments. Urban congestion and the high cost of land are pushing businesses to invest in vertical or underground parking structures that make the most of limited space. Furthermore, the integration of automated parking with smart building technologies and enhanced security systems makes it an attractive option for commercial developers.

The market is also categorized by type, with semi-automated systems accounting for the majority share in 2024. Their appeal lies in cost efficiency, quick setup, and ease of use, making them suitable for diverse applications across both residential and commercial segments. These systems offer a balance between full automation and manual control, providing enhanced user experience without the high upfront investment of fully automated alternatives. Their low maintenance requirements and user-friendly features contribute to their widespread acceptance.

Among system structures, the Automated Guided Vehicle (AGV) segment led the global market in 2024, generating the largest revenue share. AGV systems are highly adaptable and can navigate complex layouts with precision, making them ideal for crowded urban settings and large commercial projects. Their ability to integrate seamlessly into existing infrastructure while delivering high levels of automation and flexibility has made them a preferred solution for modern parking challenges. AGVs are particularly well-suited for environments where maximizing throughput and space utilization is critical.

In terms of offerings, hardware dominated the automated parking system market in 2024, accounting for the largest share of global revenue. This is due to the essential nature of physical components such as sensors, lifts, AGVs, and conveyor systems, which form the core of any automated parking operation. As systems become more sophisticated, demand for durable, high-performance hardware continues to grow, especially in projects that require long-term reliability and high-volume handling.

Regionally, Germany led the European market with USD 218.8 million in revenue in 2024 and is forecasted to grow at a CAGR of 16.9% through 2034. The country's strong automotive industry, investment in smart city projects, and advanced urban infrastructure contribute significantly to its leadership in this sector. Additionally, companies across the globe are scaling their presence by investing in research and development, strategic partnerships, and cutting-edge manufacturing techniques. Market leaders are focusing on modular system designs, energy efficiency, and integration of AI and IoT technologies to enhance both user experience and environmental performance. These innovations are setting the stage for the next generation of smart, sustainable parking solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Hardware providers

- 3.1.1.2 Software providers

- 3.1.1.3 Service providers

- 3.1.1.4 Technology providers

- 3.1.1.5 End Use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing autonomous vehicles in north america and europe

- 3.8.1.2 The rapid increase in urbanization

- 3.8.1.3 Rising smart city projects in asia pacific and middle east

- 3.8.1.4 Increasing technological advancements in parking systems

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development cost

- 3.8.2.2 Complex maintenance and downtime risk

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Fully automated

- 5.3 Semi-automated

Chapter 6 Market Estimates & Forecast, By Structure, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 AGV system

- 6.3 Silo system

- 6.4 Tower system

- 6.5 Rail Guided Cart (RGC) system

- 6.6 Puzzle system

- 6.7 Shuttle system

Chapter 7 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates & Forecast, By Platform, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Palleted

- 8.3 Non-palleted

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AutoMotion Parking

- 11.2 City Lift Parking

- 11.3 Dayang Parking

- 11.4 EITO&GLOBAL

- 11.5 Fata Automation

- 11.6 IHI

- 11.7 Klaus Multiparking

- 11.8 Lodgie

- 11.9 MHE Demag

- 11.10 Park Assist

- 11.11 Parkmatic

- 11.12 ParkPlus

- 11.13 Robotic Parking

- 11.14 Serva Transport

- 11.15 Skyline Parking

- 11.16 Stolzer Parking

- 11.17 TAPS

- 11.18 Unitronics

- 11.19 Westfalia Parking

- 11.20 Wohr Parking

2026年全球即时停车系统市场报告2026年全球自动停车系统市场报告

2026年全球即时停车系统市场报告2026年全球自动停车系统市场报告 垂直停车系统市场:按类型、技术、最终用户、营运方式、车辆类型和容量划分,全球预测,2026-2032年垂直升降式多层车库市场:按机制、容量、安装方式、最终用户和应用划分-2026-2032年全球预测

垂直停车系统市场:按类型、技术、最终用户、营运方式、车辆类型和容量划分,全球预测,2026-2032年垂直升降式多层车库市场:按机制、容量、安装方式、最终用户和应用划分-2026-2032年全球预测 全球自动停车系统市场规模、份额、趋势和成长分析报告(2026-2034年)

全球自动停车系统市场规模、份额、趋势和成长分析报告(2026-2034年) 自动停车系统市场 - 全球产业规模、份额、趋势、机会及预测(按应用、自动化程度、组件、平台类型、结构类型、地区和竞争格局划分,2021-2031年)

自动停车系统市场 - 全球产业规模、份额、趋势、机会及预测(按应用、自动化程度、组件、平台类型、结构类型、地区和竞争格局划分,2021-2031年) 2026-2030年全球自动停车系统(APS)市场全球自动乘用车停车系统市场,2025-2031年

2026-2030年全球自动停车系统(APS)市场全球自动乘用车停车系统市场,2025-2031年 自动停车系统市场规模、份额和成长分析(按自动化程度、系统类型、最终用户、设计模型、平台类型、停车层级、结构类型和地区划分)—2026-2033年产业预测

自动停车系统市场规模、份额和成长分析(按自动化程度、系统类型、最终用户、设计模型、平台类型、停车层级、结构类型和地区划分)—2026-2033年产业预测 自动停车系统市场规模、份额、趋势分析报告:按组件、按结构类型、按平台类型、按自动化水平、按最终用途、按地区、按细分市场、预测,2025-2030 年

自动停车系统市场规模、份额、趋势分析报告:按组件、按结构类型、按平台类型、按自动化水平、按最终用途、按地区、按细分市场、预测,2025-2030 年