|

市场调查报告书

商品编码

1741050

热界面材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Thermal Interface Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

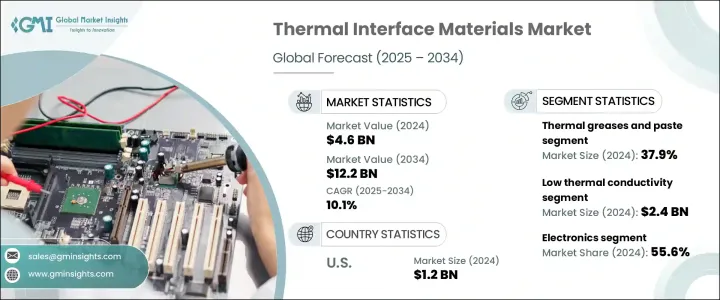

2024 年全球热界面材料市场价值为 46 亿美元,预计到 2034 年将以 10.1% 的复合年增长率增长,达到 122 亿美元,这得益于多个行业(尤其是汽车、电子和工业製造)应用的不断扩展。随着各行各业竞相发展小型化、电气化和智慧化技术,对可靠的热管理解决方案的需求激增。新时代汽车、连网设备、云端运算和智慧製造都需要能够承受更高热负荷且效能不下降的元件。热界面材料 (TIM) 已成为这种情况下的关键推动因素,支援系统效率、耐用性和安全性。对能源效率和系统优化的日益重视,以及永续发展趋势,已将 TIM 置于各行业创新的中心。随着企业对电动车、人工智慧基础设施和高性能电子产品的投资,TIM 在重塑全球技术格局方面发挥关键作用。

随着现代电动车设计整合了紧凑型组件、高输出电池和轻量化结构,汽车电气化推动了对高效热管理系统的强劲需求。随着系统发热越来越大、空间越来越狭窄,高性能热界面材料 (TIM) 有助于控制温度并确保使用寿命。在不断发展的汽车领域,人们对自动驾驶技术的兴趣日益浓厚,进一步推动了对先进热管理材料的需求,因为感测器密集系统会产生大量的热负荷。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 46亿美元 |

| 预测值 | 122亿美元 |

| 复合年增长率 | 10.1% |

同时,消费性电子、工业自动化和电信业不断突破性能界限。对高效能运算和紧凑型智慧型装置的日益依赖,提高了功率密度,也加剧了对可靠散热解决方案的需求。随着人工智慧和云端运算的扩展,资料中心大力投资下一代TIM,以保护其基础设施。

市场对导热硅脂和导热膏的需求明显增长,凭藉其卓越的导热性、多功能性和便捷的使用方式,它们在2024年占据了37.9%的市场份额。这些材料在消费性电子和工业电子产品中广受欢迎,因为它们能够消除发热元件和散热器之间的气隙,从而实现高效的散热。其柔韧性使其能够贴合微观表面缺陷,改善接触性能并降低热阻。与固态TIM不同,导热硅脂能够长期保持其有效性,不会硬化或开裂,使其成为动态热环境和频繁进行热循环的设备的理想选择。

依热导率分析,热界面材料市场可分为低导热率、中导热率和高导热率类型。低导热率材料市值在2024年达到24亿美元,预计到2034年将以10.5%的复合年增长率增长,这得益于其在空间受限的电子产品中的广泛应用,在这些电子产品中,柔性、经济高效且导热性适中的材料就已足够。这些材料因其在热性能、机械柔顺性和经济可行性方面的出色平衡而被广泛采用——这些因素是紧凑型消费设备、资讯娱乐系统和车载汽车电子设备等应用的关键因素。

北美热界面材料市场在2024年将达到17亿美元,复合年增长率达11%,这得益于其在先进製造、半导体生产以及电动车和5G基础设施快速扩张方面的稳固地位。北美拥有众多高性能电子、自动驾驶系统和电信行业的关键参与者,这些行业对高效的热管理解决方案的需求日益增长,因此北美市场受益匪浅。此外,再生能源技术和边缘运算领域投资的不断增长也进一步支撑了该地区的成长,因为这两个领域都需要稳定的温度控制,以最大限度地延长系统正常运行时间和提高组件的耐用性。

全球热界面材料市场的主要参与者包括 3M、霍尼韦尔国际公司、派克汉尼汾公司、汉高股份公司和信越化学株式会社。为了保持竞争优势,领先企业正在大力投资研发,以开发专为下一代电子产品和电动车量身定制的创新高性能热界面材料 (TIM),扩大产能,并与原始设备製造商 (OEM) 建立战略联盟,以获得重大项目的早期授权。企业也正在进行併购交易,以多元化产品组合併加速技术应用。此外,为了符合永续发展目标,增强品牌吸引力并确保在全球市场的合规性,企业正在大力推广环保材料。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 中断

- 未来展望

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业回应

- 供应链重构

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 不断发展的汽车产业

- 不断发展的电子产业

- 技术进步

- 产业陷阱与挑战

- 开发成本高

- 材料选择和相容性

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场规模及预测:依材料类型,2021 年至 2034 年

- 主要趋势

- 导热油脂和导热膏

- 导热垫及导热膜

- 相变材料

- 热黏合剂

- 热敏胶带

- 填缝剂

第六章:市场规模及预测:依热导率,2021 年至 2034 年

- 主要趋势

- 低的

- 中等的

- 高的

第七章:市场规模及预测:依应用,2021 年至 2034 年

- 主要趋势

- 电子产品

- 汽车

- 电信

- 工业的

- 航太和国防

- 其他的

第八章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第九章:公司简介

- Honeywell International

- 3M

- Henkel AG

- Parker Hannifin

- Shin-Etsu Chemical

- Momentive Performance Materials

- Wakefield-Vette

- Indium

- Panasonic

- Arctic Silver

- Fujipoly America

- Master Bond

The Global Thermal Interface Materials Market was valued at USD 4.6 billion in 2024 and is estimated to grow at a CAGR of 10.1% to reach USD 12.2 billion by 2034, driven by expanding applications across multiple industries, particularly automotive, electronics, and industrial manufacturing. As industries race toward miniaturization, electrification, and smarter technologies, the need for reliable thermal management solutions has surged. New-age vehicles, connected devices, cloud computing, and smart manufacturing all demand components that can withstand higher heat loads without performance degradation. Thermal interface materials (TIMs) have become critical enablers in this scenario, supporting system efficiency, durability, and safety. The growing emphasis on energy efficiency and system optimization, along with sustainability trends, has placed TIMs at the center of innovation across sectors. As companies invest in EVs, AI infrastructure, and high-performance electronics, TIMs are playing a pivotal role in reshaping the global technology landscape.

Electrification in vehicles has fueled a strong demand for efficient heat management systems, as modern EV designs integrate compact components, high-output batteries, and lightweight structures. As systems become more heat-intensive and confined, high-performance TIMs help manage temperatures and ensure operational longevity. In the evolving automotive landscape, rising interest in self-driving technologies has further boosted demand for advanced thermal management materials, as sensor-intensive systems generate substantial heat loads.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.6 Billion |

| Forecast Value | $12.2 Billion |

| CAGR | 10.1% |

At the same time, consumer electronics, industrial automation, and telecommunications continue to push performance boundaries. The growing reliance on high-performance computing and compact smart devices has increased power densities, escalating the need for reliable heat dissipation solutions. As artificial intelligence and cloud computing expand, data centers invest heavily in next-gen TIMs to safeguard their infrastructure.

The market has shown a clear inclination toward thermal greases and pastes, which captured a 37.9% share in 2024 due to their exceptional thermal conductivity, versatility, and ease of application. These materials are widely favored in consumer and industrial electronics because they offer highly effective heat dissipation by eliminating air gaps between heat-generating components and heat sinks. Their pliability allows them to conform to microscopic surface imperfections, improving contact and reducing thermal resistance. Unlike solid-state TIMs, thermal greases maintain their effectiveness over time without hardening or cracking, making them ideal for dynamic thermal environments and devices that undergo frequent thermal cycling.

When analyzed by thermal conductivity, the thermal interface materials market is segmented into low, medium, and high conductivity types. Low thermal conductivity materials, valued at USD 2.4 billion in 2024, are expected to grow at a CAGR of 10.5% through 2034 due to their significant use in space-constrained electronics where flexible, cost-effective, and moderately conductive materials are sufficient. These materials are commonly selected for their excellent balance of thermal performance, mechanical compliance, and economic viability-key factors in applications like compact consumer devices, infotainment systems, and onboard automotive electronics.

North America Thermal Interface Materials Market generated USD 1.7 billion in 2024 to grow at a CAGR of 11% driven by its strong foothold in advanced manufacturing, semiconductor production, and the rapid scaling of electric vehicles and 5G infrastructure. North America benefits from being home to several key players in high-performance electronics, autonomous systems, and telecommunications-industries that demand increasingly efficient thermal management solutions. Moreover, rising investments in renewable energy technologies and edge computing further support the region's growth, as both segments require stable temperature control for maximum system uptime and component durability.

Key industry players in the Global Thermal Interface Materials Market include 3M, Honeywell International Inc., Parker Hannifin Corporation, Henkel AG, and Shin-Etsu Chemical Co., Ltd. To maintain their competitive edge, leading companies are investing heavily in R&D to develop innovative, high-performance TIMs tailored for next-gen electronics and EVs, expanding production capacities, and forming strategic alliances with OEMs to gain early access to major projects. Firms are also entering into M&A deals to diversify their portfolio and accelerate technology adoption. Additionally, there is a push toward eco-friendly materials to align with sustainability goals, enhancing brand appeal and ensuring compliance in global markets.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic Industry Responses

- 3.2.4.1 Supply Chain Reconfiguration

- 3.2.4.2 Pricing and Product Strategies

- 3.2.4.3 Policy Engagement

- 3.2.5 Outlook and Future Considerations

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Supplier landscape

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Growing automotive industry

- 3.7.1.2 Growing electronics industry

- 3.7.1.3 Technology advancement

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 High development costs

- 3.7.2.2 Material selection and compatibility

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Material Type, 2021 – 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Thermal greases and paste

- 5.3 Thermal pads and films

- 5.4 Phase change materials

- 5.5 Thermal adhesives

- 5.6 Thermal tapes

- 5.7 Gap fillers

Chapter 6 Market Size and Forecast, By Thermal Conductivity, 2021 – 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Low

- 6.3 Medium

- 6.4 High

Chapter 7 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion, Kilo Tons)

- 7.1 Key trends

- 7.2 Electronics

- 7.3 Automotive

- 7.4 Telecommunications

- 7.5 Industrial

- 7.6 Aerospace and defense

- 7.7 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Honeywell International

- 9.2 3M

- 9.3 Henkel AG

- 9.4 Parker Hannifin

- 9.5 Shin-Etsu Chemical

- 9.6 Momentive Performance Materials

- 9.7 Wakefield-Vette

- 9.8 Indium

- 9.9 Panasonic

- 9.10 Arctic Silver

- 9.11 Fujipoly America

- 9.12 Master Bond

全球导热绝缘体市场(材料类型、产品形式和应用划分)预测(2026-2032年)

全球导热绝缘体市场(材料类型、产品形式和应用划分)预测(2026-2032年) 全球导热界面材料市场规模、份额、趋势及成长分析报告(2026-2034)

全球导热界面材料市场规模、份额、趋势及成长分析报告(2026-2034) 热感界面材料市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)聚合物基导热界面材料市场:依材料类型、产品形式、导热係数范围及最终用途产业划分-2026-2032年全球预测

热感界面材料市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2026-2033 年)聚合物基导热界面材料市场:依材料类型、产品形式、导热係数范围及最终用途产业划分-2026-2032年全球预测 导热界面材料市场预测至2032年:按产品类型、填充材、导热係数、应用和地区分類的全球分析

导热界面材料市场预测至2032年:按产品类型、填充材、导热係数、应用和地区分類的全球分析 日本导热界面材料市场报告(按产品类型、应用和地区划分,2026-2034年)

日本导热界面材料市场报告(按产品类型、应用和地区划分,2026-2034年) 热感界面材料市场规模、份额及成长分析(按类型、材料、应用及地区划分)-2026-2033年产业预测

热感界面材料市场规模、份额及成长分析(按类型、材料、应用及地区划分)-2026-2033年产业预测 热感界面材料(TIM)-全球市占率及排名、总收入及需求预测(2025-2031年)热感界面材料填料:全球市场占有率及排名、总收入及需求预测(2025-2031年)电动汽车电池热感介面材料:全球市场份额和排名、总销售额和需求预测(2025-2031 年)

热感界面材料(TIM)-全球市占率及排名、总收入及需求预测(2025-2031年)热感界面材料填料:全球市场占有率及排名、总收入及需求预测(2025-2031年)电动汽车电池热感介面材料:全球市场份额和排名、总销售额和需求预测(2025-2031 年)