|

市场调查报告书

商品编码

1750283

发电厂重型燃气涡轮机市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Power Plants Heavy Duty Gas Turbine Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

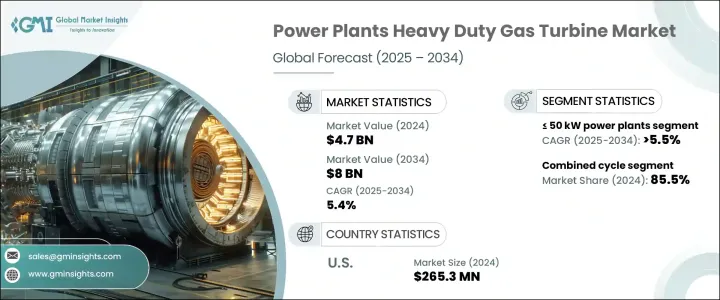

2024 年全球发电厂重型燃气涡轮机市场价值为 47 亿美元,预计到 2034 年将以 5.4% 的复合年增长率增长,达到 80 亿美元,这得益于向可靠、按需能源的持续转变,这促使主要公用事业和公共部门机构增加对燃气发电的投资。在快速工业化和全球能源需求的推动下,对尖峰负载和基荷能源解决方案的需求不断增长,该市场正在获得发展动力。对能源安全的日益关注,加上天然气勘探和贸易活动的增加,正在进一步塑造市场。此外,随着各国寻求提高能源基础设施的效率,整合数位技术和智慧电网解决方案正在加速应用。降低排放和减少大型电厂资本支出的推动支持向燃气涡轮机发电的过渡。

重型燃气涡轮机因其能够产生高功率输出,同时保持营运灵活性和环保合规性而备受青睐。这些燃气涡轮机透过先进的空气压缩、燃料混合和点火工艺运行,产生高压气体,使涡轮叶片高速旋转,从而提供卓越的发电性能。该行业面临一些阻力,尤其是由于最近实施的贸易关税,这提高了铝、钢和特殊合金等关键原材料的成本。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 47亿美元 |

| 预测值 | 80亿美元 |

| 复合年增长率 | 5.4% |

预计到2034年,50千瓦及以下发电厂重型燃气涡轮机市场的复合年增长率将超过5.5%,这得益于其在分散式能源系统中的日益普及。这些紧凑型机组对于需要可靠现场发电的工业和偏远地区至关重要。其灵活性、运作效率和紧凑的占地面积使其成为电网连接有限或不稳定的分散式电网的理想选择。随着工业设施寻求经济高效的方式来确保不间断供电,同时最大限度地减少碳排放,这些低容量燃气涡轮机的吸引力持续增强。

在技术方面,联合循环发电领域在2024年将占据85.5%的市场份额,这得益于联合循环系统的卓越效率,该系统利用燃气涡轮机和蒸汽涡轮机从同一燃料源中获取最大能量。这些系统显着减少了排放并优化了燃料使用,符合环境目标和严格的监管标准。向清洁能源发电的转变促使公用事业公司和独立电力生产商逐步淘汰传统燃煤电厂,并采用联合循环解决方案作为更永续的替代方案。

2024年,美国重型燃气涡轮机市场规模达2.653亿美元,反映出美国对可靠清洁电力的需求日益增长。快速的工业化进程、人工智慧资料中心等能源密集产业的兴起,以及煤炭向天然气的广泛转型,是推动这一成长的关键因素。页岩气供应的不断增加,进一步巩固了美国作为天然气强国的地位,为燃气涡轮机运作提供了稳定的供应链。

市场领导者包括瓦锡兰、西门子能源、通用电气 Vernova、Vericor、MAN Energy Solutions、Flex Energy Solutions、南京蒸汽涡轮机电机(集团)、索拉透平、川崎重工、凯普斯通绿色能源控股、贝克休斯、三菱重工、斗山能源、劳斯莱斯、巴拉特重型电气、Destinus Energy Energy、安萨尔多能源、滨电电气。为了提升市场份额,各企业正专注于多项策略,包括透过数位化升级和远端监控解决方案扩展服务组合,从而优化涡轮机性能并减少停机时间。企业投资模组化涡轮机设计,以便在公用事业和工业场所灵活部署。与能源供应商的策略合作和长期供应协议有助于巩固市场地位。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 战略仪表板

- 策略倡议

- 公司市占率分析

- 竞争基准测试

- 创新与永续发展格局

第五章:市场规模及预测:依产能,2021 - 2034 年

- 主要趋势

- ≤ 50 千瓦

- > 50 千瓦至 500 千瓦

- > 500 千瓦至 1 兆瓦

- > 1 兆瓦至 30 兆瓦

- > 30 兆瓦至 70 兆瓦

- > 70 兆瓦至 200 兆瓦

- > 200 兆瓦

第六章:市场规模及预测:依技术分类,2021 - 2034 年

- 主要趋势

- 开放式循环

- 复合循环

第七章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 英国

- 法国

- 德国

- 俄罗斯

- 义大利

- 荷兰

- 芬兰

- 希腊

- 丹麦

- 罗马尼亚

- 波兰

- 瑞典

- 亚太地区

- 中国

- 澳洲

- 日本

- 韩国

- 印尼

- 泰国

- 马来西亚

- 孟加拉

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 卡达

- 科威特

- 阿曼

- 埃及

- 土耳其

- 巴林

- 伊拉克

- 约旦

- 南非

- 奈及利亚

- 阿尔及利亚

- 肯亚

- 迦纳

- 拉丁美洲

- 巴西

- 阿根廷

- 秘鲁

- 智利

第八章:公司简介

- Ansaldo Energia

- Baker Hughes

- Bharat Heavy Electricals

- Capstone Green Energy Holdings

- Destinus Energy

- Doosan Enerbility

- Flex Energy Solutions

- GE Vernova

- Harbin Electric

- Kawasaki Heavy Industries

- MAN Energy Solutions

- Mitsubishi Heavy Industries

- Nanjing Steam Turbine Motor (Group)

- Rolls Royce

- Siemens Energy

- Solar Turbines

- Vericor

- Wartsilä

The Global Power Plants Heavy Duty Gas Turbine Market was valued at USD 4.7 billion in 2024 and is estimated to grow at a CAGR of 5.4% to reach USD 8 billion by 2034, driven by the ongoing shift toward reliable, on-demand energy sources is prompting major utilities and public sector bodies to increase investments in gas-based power generation. This market is gaining momentum with the rising demand for peak-load and base-load energy solutions, driven by rapid industrialization and global energy needs. The growing focus on energy security, combined with increasing natural gas exploration and trade activity, is further shaping the market. Additionally, as countries look to enhance the efficiency of their energy infrastructure, integrating digital technologies and smart grid solutions is accelerating adoption. The push for lower emissions and reduced capital expenditure on large-scale plants supports the transition toward gas turbine-based generation.

Heavy-duty gas turbines are favored for their ability to produce high power outputs while maintaining operational flexibility and environmental compliance. These turbines function through an advanced process of air compression, fuel mixing, and ignition, resulting in high-pressure gases that spin turbine blades at intense speeds, delivering remarkable power generation performance. The industry has faced some headwinds, particularly due to trade tariffs introduced recently, which raised the cost of key input materials such as aluminum, steel, and specialized alloys.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.7 Billion |

| Forecast Value | $8 Billion |

| CAGR | 5.4% |

The <= 50 kW power plants heavy-duty gas turbine segment is forecasted to grow at a CAGR of over 5.5% through 2034, driven by its increasing adoption in decentralized energy systems. These compact units are proving vital for industries and remote facilities that require reliable, on-site power generation. Their flexibility, operational efficiency, and compact footprint make them ideal for distributed power networks where grid connectivity is limited or inconsistent. As industrial facilities seek cost-effective ways to ensure uninterrupted power while minimizing carbon output, the appeal of these lower-capacity turbines continues to strengthen.

On the technology front, the combined cycle segment held 85.5% share in 2024, driven by the superior efficiency of combined cycle systems, which utilize gas and steam turbines to extract maximum energy from the same fuel source. These systems significantly cut emissions and optimize fuel usage, aligning with environmental goals and stringent regulatory standards. The shift toward clean energy generation prompts utilities and independent power producers to phase out conventional coal plants and adopt combined cycle solutions as a more sustainable alternative.

United States Heavy Duty Gas Turbine Market was valued at USD 265.3 million in 2024, reflecting the country's accelerating demand for reliable and clean electricity. Rapid industrialization, the rise of energy-intensive sectors like artificial intelligence data centers, and the widespread transition from coal to natural gas are key contributors to this growth. The increasing availability of shale gas has further strengthened the U.S. position as a natural gas powerhouse, enabling stable supply chains for gas turbine operations.

Leading companies in the market include Wartsila, Siemens Energy, GE Vernova, Vericor, MAN Energy Solutions, Flex Energy Solutions, Nanjing Steam Turbine Motor (Group), Solar Turbines, Kawasaki Heavy Industries, Capstone Green Energy Holdings, Baker Hughes, Mitsubishi Heavy Industries, Doosan Enerbility, Rolls Royce, Bharat Heavy Electricals, Destinus Energy, Ansaldo Energia, Harbin Electric, and others. To enhance market presence, companies are focusing on several strategies. These include expanding their service portfolios through digital upgrades and remote monitoring solutions, which optimize turbine performance and reduce operational downtime. Firms invest in modular turbine designs for flexible deployment across utility and industrial sites. Strategic collaborations with energy providers and long-term supply agreements are helping solidify market positions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiatives

- 4.4 Company market share analysis, 2024

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million & MW)

- 5.1 Key trends

- 5.2 ≤ 50 kW

- 5.3 > 50 kW to 500 kW

- 5.4 > 500 kW to 1 MW

- 5.5 > 1 MW to 30 MW

- 5.6 > 30 MW to 70 MW

- 5.7 > 70 MW to 200 MW

- 5.8 > 200 MW

Chapter 6 Market Size and Forecast, By Technology, 2021 - 2034 (USD Million & MW)

- 6.1 Key trends

- 6.2 Open cycle

- 6.3 Combined cycle

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million & MW)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 France

- 7.3.3 Germany

- 7.3.4 Russia

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.3.7 Finland

- 7.3.8 Greece

- 7.3.9 Denmark

- 7.3.10 Romania

- 7.3.11 Poland

- 7.3.12 Sweden

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Australia

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Indonesia

- 7.4.6 Thailand

- 7.4.7 Malaysia

- 7.4.8 Bangladesh

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 Qatar

- 7.5.4 Kuwait

- 7.5.5 Oman

- 7.5.6 Egypt

- 7.5.7 Turkey

- 7.5.8 Bahrain

- 7.5.9 Iraq

- 7.5.10 Jordan

- 7.5.11 South Africa

- 7.5.12 Nigeria

- 7.5.13 Algeria

- 7.5.14 Kenya

- 7.5.15 Ghana

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Peru

- 7.6.4 Chile

Chapter 8 Company Profiles

- 8.1 Ansaldo Energia

- 8.2 Baker Hughes

- 8.3 Bharat Heavy Electricals

- 8.4 Capstone Green Energy Holdings

- 8.5 Destinus Energy

- 8.6 Doosan Enerbility

- 8.7 Flex Energy Solutions

- 8.8 GE Vernova

- 8.9 Harbin Electric

- 8.10 Kawasaki Heavy Industries

- 8.11 MAN Energy Solutions

- 8.12 Mitsubishi Heavy Industries

- 8.13 Nanjing Steam Turbine Motor (Group)

- 8.14 Rolls Royce

- 8.15 Siemens Energy

- 8.16 Solar Turbines

- 8.17 Vericor

- 8.18 Wartsilä

全球大型燃气涡轮机市场规模、份额、趋势和成长分析报告:2026-2034年

全球大型燃气涡轮机市场规模、份额、趋势和成长分析报告:2026-2034年 大型燃气涡轮机市场机会、成长要素、产业趋势分析及2026年至2035年预测

大型燃气涡轮机市场机会、成长要素、产业趋势分析及2026年至2035年预测 重型燃气涡轮机机服务市场规模、份额和成长分析(按服务类型、应用、涡轮机、最终用户产业、零件和地区划分)-2026-2033年产业预测

重型燃气涡轮机机服务市场规模、份额和成长分析(按服务类型、应用、涡轮机、最终用户产业、零件和地区划分)-2026-2033年产业预测 大型燃气涡轮机市场规模、份额和成长分析(按燃料类型、功率输出、应用、涡轮机类型和地区划分)-2026-2033年产业预测

大型燃气涡轮机市场规模、份额和成长分析(按燃料类型、功率输出、应用、涡轮机类型和地区划分)-2026-2033年产业预测 全球重型燃气涡轮机服务市场全球重型燃气涡轮机市场

全球重型燃气涡轮机服务市场全球重型燃气涡轮机市场 到 2030 年大型燃气涡轮机服务市场预测:按服务类型、涡轮机容量、涡轮机类型、最终用户和地区进行的全球分析

到 2030 年大型燃气涡轮机服务市场预测:按服务类型、涡轮机容量、涡轮机类型、最终用户和地区进行的全球分析