|

市场调查报告书

商品编码

1750312

姜饼市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Gingerbread Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

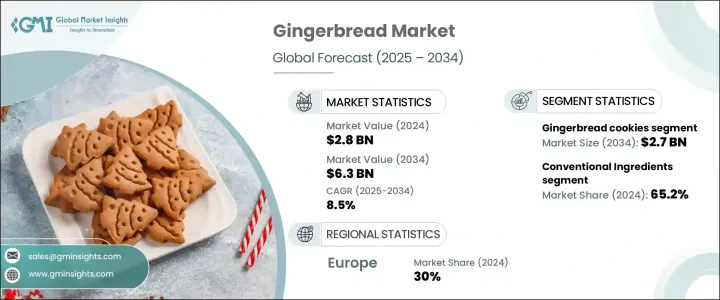

2024年,全球姜饼市场规模达28亿美元,预计到2034年将以8.5%的复合年增长率成长,达到63亿美元。这得归功于节日期间姜饼产品需求的不断增长,尤其是作为节日零食,以及姜饼在全球市场的日益普及。各大企业也将姜饼作为一种有效的促销工具,并将其应用于广告策略中,这些策略在西方节日传统日益盛行的非西方国家尤其取得了良好的反响。此外,注重健康的消费者推动了对无麸质、有机和低糖姜饼等替代产品的需求,促进了市场扩张。

包装和分销技术的进步,加上电子商务的兴起,预计将在姜饼市场的成长中发挥关键作用。消费者现在可以轻鬆获得各种保质期更长、配送方式更方便的产品。此外,向永续环保包装的转变也符合消费者日益增长的环保需求。市场适应不断变化的消费者偏好和经济状况的能力反映了其韧性,并为持续创新和成长提供了机会。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 28亿美元 |

| 预测值 | 63亿美元 |

| 复合年增长率 | 8.5% |

预计到2034年,姜饼市场规模将达到27亿美元,2025年至2034年的复合年增长率为8.7%。姜饼拥有丰富的形状、大小和口味,经久不衰,是推动其成长的主要动力。其节日特质,尤其是在假日期间,确保了持续的需求。而针对注重健康的消费者所推出的创新产品,例如无麸质、低糖和低卡路里产品,也有助于进一步扩大市场。此外,包装技术的进步提升了产品的新鲜度和吸引力,也促进了姜饼的广泛分销和消费者的接受度。

传统配料领域在2024年占据了65.2%的市场份额,预计到2034年将继续以8.6%的复合年增长率成长。儘管替代配料日益兴起,但生姜、精製麵粉和糖等传统成分仍然是姜饼市场的基石。然而,消费者日益增强的健康意识正在将需求转向有机、无麸质和植物性替代品,为该领域的创新提供了途径。随着消费者偏好的演变,人们对营养更丰富的产品的需求日益增长,这促使製造商探索更健康的配料选择,以保持竞争力。

2024年,欧洲姜饼市场将占据30%的市场份额,这得益于人们对姜饼的悠久文化渊源,尤其是在冬季节庆期间。北欧和中欧等拥有深厚姜饼烘焙传统的国家,对市场的成长贡献巨大。此外,欧洲消费者的经济稳定性和购买力,加上对优质手工烘焙食品的强烈偏好,有助于支持姜饼产业的持续扩张。

全球姜饼产业的主要参与者包括 Bahlsen、Ginger People、Kinnikinnick Foods、Pepperidge Farm 和 Stauffer's。为了维持市场地位,各公司专注于产品创新,尤其是在更健康的产品方面,例如无麸质和有机姜饼。他们也在提升线上影响力,以抓住电商成长的机会。例如,Kinnikinnick Foods 和 Pamela's Products 等公司专注于无麸质产品,而 Bahlsen 和 Ginger People 则正在扩大其高端和手工姜饼系列。与零售商合作以提高产品的知名度和供应量,以及对永续包装的投资,也有助于这些品牌满足不断变化的消费者需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 影响价值链的因素

- 利润率分析

- 製造商

- 经销商

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供给侧影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 主要出口国

- 主要进口国

- 供应商格局

- 利润率分析

- 重要新闻和倡议

- 监理环境与合规性

- 食品安全法规

- FDA 和 USDA 要求(美国)

- 欧洲食品安全局(EFSA)指南

- 丙烯酰胺法规与缓解策略

- 其他区域监管框架

- 标籤和包装法规

- 成分揭露要求

- 过敏原标示标准

- 营养资讯要求

- 环境和永续性法规

- 进出口法规

- 关税和贸易壁垒

- 文件和认证要求

- 外国供应商验证计划

- 区域贸易协定的影响

- 製造商的合规策略

- 监管监测和适应

- 品质保证计划

- 第三方认证

- 风险管理方法

- 食品安全法规

- 衝击力

- 成长动力

- 对时令食品和节庆食品的需求不断增长

- 西方节庆文化在全球的扩张

- 便捷的产品格式

- 方便且保质期更长

- 产业陷阱与挑战

- 需求的季节性

- 新鲜产品的保存期限短

- 市场机会

- 新颖的口味(例如,印度香料姜饼)

- DTC电子商务成长

- 全年品牌推广(如姜饼拿铁活动)

- 合作(例如迪士尼主题套件)

- 成长动力

- 成长潜力分析

- 波特的分析

- Pestel 分析

- 消费者分析

- 消费者人口统计和目标受众分析

- 年龄和性别分布

- 收入水平分析

- 地理分布

- 生活风格和心理细分

- 消费者购买行为

- 购买动机和触发因素

- 季节性购买模式

- 价格敏感度分析

- 品牌忠诚度评估

- 消费者偏好

- 口味和食材偏好

- 包装偏好

- 健康和营养考虑

- 永续性和道德采购问题

- 影响市场的消费趋势

- 怀旧与传统价值观

- DIY和手工艺活动

- 社群媒体影响力与可分享性

- 高端化和赠礼趋势

- 消费者人口统计和目标受众分析

- 製造和技术分析

- 生产流程概述

- 传统製造方法

- 现代工业生产技术

- 手工和小批量生产

- 製造业的技术创新

- 自动化和机器人集成

- 数位控制系统和物联网应用

- 3D列印和客製化设计技术

- 包装创新

- 品质控制和食品安全措施

- 生产中的关键控制点

- 测试和监控协议

- 保存期限延长技术

- 过敏原管理系统

- 供应链分析

- 原物料采购和供应商网络

- 库存管理策略

- 配送和物流优化

- 冷链要求和挑战

- 生产流程概述

- 市场趋势与创新

- 产品创新趋势

- 以健康为导向的配方

- 风味创新与融合概念

- 功能性成分和强化

- 质感和感官增强

- 包装和展示创新

- 永续包装解决方案

- 互动式智慧包装

- 礼品包装及优质包装

- 份量控制和便利功能

- 行销和促销趋势

- 社群媒体与影响力行销

- 体验式行销与快闪概念

- 季节性和限量策略

- 跨类别合作

- 永续发展倡议

- 永续采购实践

- 减少废弃物的策略

- 减少碳足迹

- 道德劳动实践

- 产品创新趋势

- 投资分析与策略建议

- 投资机会评估

- 扩大产能

- 技术升级

- 新产品开发

- 地理扩张

- 给製造商的策略建议

- 产品组合优化

- 供应链弹性策略

- 数位转型路线图

- 永续性整合

- 给零售商的策略建议

- 商品销售与展示策略

- 自有品牌机会

- 全通路整合

- 季节性计划优化

- 对新进入者的策略建议

- 市场进入策略

- 利基定位方法

- 伙伴关係和合作机会

- 扩展和成长策略

- 投资机会评估

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司热图分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 策略仪表板

- 主要参与者的最新发展和影响分析

- 公司分类

- 参与者概述

- 财务表现

- 产品基准测试

第五章:市场估计与预测:按产品,2021-2034

- 主要趋势

- 姜饼

- 姜饼屋和套件

- 姜饼口味产品

- 预製装饰物品

- 其他的

第六章:市场估计与预测:依成分类型,2021-2034

- 主要趋势

- 常规成分

- 有机和天然成分

- 无麸质变体

- 纯素和植物性选择

第七章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 直接消费

- 装饰和展示用途

- 礼品和纪念品市场

- 餐饮服务应用

第八章:市场估计与预测:按配销通路,2021-2034 年

- 主要趋势

- 超市和大卖场

- 专卖店和麵包店

- 网路零售与电子商务

- 便利商店

- 其他的

第九章:市场估计与预测:依包装类型,2021-2034

- 主要趋势

- 盒子和纸箱

- 袋子和包包

- 蛤壳式包装和托盘式包装

- 礼品包装

- 其他的

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Pepperidge Farm

- Archway Cookies

- Stauffer's

- Ginger People

- Pamela's Products

- Kinnikinnick Foods

- Bahlsen

- Lambertz

- Niederegger

- Hussel

- Fortnum & Mason

- Biona Organic

- Pischinger

- Krasny

- Gingerbread Folk

- Arnott's Biscuits

- Griffin's

- The Gingerbread House

- Lebkuchen Schmidt

- Daelmans

The Global Gingerbread Market was valued at USD 2.8 billion in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 6.3 billion by 2034, fueled by the rising demand for gingerbread products during the holiday season, especially as festive treats, and the increasing popularity of gingerbread in global markets. Companies are also leveraging gingerbread as an effective promotional tool, using it in advertising strategies that have resonated particularly well in non-Western countries, where Western holiday traditions are becoming more prevalent. Furthermore, health-conscious consumers drive demand for alternative options such as gluten-free, organic, and low-sugar gingerbread products, contributing to market expansion.

Technological advancements in packaging and distribution, coupled with the rise of e-commerce, are expected to play a crucial role in the gingerbread market's growth. Consumers can now easily access a variety of products with longer shelf lives and convenient delivery options. Additionally, the shift towards sustainable and eco-friendly packaging is in line with growing consumer demand for more environmentally friendly choices. The market's ability to adapt to changing consumer preferences and economic conditions reflects its resilience and provides opportunities for continued innovation and growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.8 Billion |

| Forecast Value | $6.3 Billion |

| CAGR | 8.5% |

The gingerbread cookies segment is projected to reach USD 2.7 billion by 2034, growing at a CAGR of 8.7% from 2025 to 2034. The enduring popularity of gingerbread cookies, which are available in a wide range of shapes, sizes, and flavors, is a major driver of this growth. Their festive appeal, particularly during the holiday season, ensures consistent demand, while innovations aimed at health-conscious consumers, such as gluten-free, reduced-sugar, and low-calorie options, are helping to expand the market further. Additionally, the evolution of packaging technology, which enhances product freshness and appeal, is contributing to the broader distribution and consumer acceptance of gingerbread cookies.

The conventional ingredients segment held 65.2% share in 2024 and is expected to continue growing at 8.6% CAGR through 2034. Despite the rise of alternative ingredients, traditional components such as ginger, refined flour, and sugar remain a cornerstone of the gingerbread market. However, growing health consciousness among consumers is shifting demand toward organic, gluten-free, and plant-based alternatives, providing an avenue for innovation in the sector. As consumer preferences evolve, there is a noticeable push for more nutrient-dense products, prompting manufacturers to explore healthier ingredient options to remain competitive.

Europe Gingerbread Market held a 30% share in 2024, driven by the long-standing cultural connection to gingerbread, especially during the winter holidays. Countries with deep-rooted traditions of gingerbread baking, such as those in Northern and Central Europe, contribute significantly to the market's growth. Furthermore, the economic stability and purchasing power of European consumers, combined with a strong preference for premium, artisanal baked goods, help support the ongoing expansion of the gingerbread sector.

Key players in the Global Gingerbread Industry include Bahlsen, Ginger People, Kinnikinnick Foods, Pepperidge Farm, and Stauffer's. To maintain their market position, companies focus on product innovation, especially in healthier offerings such as gluten-free and organic gingerbread options. They are also enhancing their online presence to tap into e-commerce growth. For example, companies like Kinnikinnick Foods and Pamela's Products focus on gluten-free variants, while Bahlsen and Ginger People are expanding their range of premium and artisanal options. Collaboration with retailers to improve product visibility and availability, and investments in sustainable packaging, are also helping these brands meet evolving consumer demands.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.6 Strategic industry responses

- 3.2.6.1 Supply chain reconfiguration

- 3.2.6.2 Pricing and product strategies

- 3.2.6.3 Policy engagement

- 3.2.7 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Supplier landscape

- 3.5 Profit margin analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory environment and compliance

- 3.7.1 Food safety regulations

- 3.7.1.1 FDA and USDA Requirements (US)

- 3.7.1.2 European Food Safety Authority (EFSA) Guidelines

- 3.7.1.3 Acrylamide regulations and mitigation strategies

- 3.7.1.4 Other regional regulatory frameworks

- 3.7.2 Labeling and packaging regulations

- 3.7.2.1 Ingredient disclosure requirements

- 3.7.2.2 Allergen labeling standards

- 3.7.2.3 Nutritional information requirements

- 3.7.2.4 Environmental and sustainability regulations

- 3.7.3 Import/export regulations

- 3.7.3.1 Tariffs and trade barriers

- 3.7.3.2 Documentation and certification requirements

- 3.7.3.3 Foreign supplier verification programs

- 3.7.3.4 Regional trade agreements impact

- 3.7.4 Compliance strategies for manufacturers

- 3.7.4.1 Regulatory monitoring and adaptation

- 3.7.4.2 Quality assurance programs

- 3.7.4.3 Third-party certifications

- 3.7.4.4 Risk management approaches

- 3.7.1 Food safety regulations

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for seasonal and festive foods

- 3.8.1.2 Expansion of western holiday culture globally

- 3.8.1.3 Convenient product formats

- 3.8.1.4 Convenience and longer shelf life

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 Seasonality of demand

- 3.8.2.2 Short shelf life of fresh products

- 3.8.3 Market opportunities

- 3.8.3.1 Novel flavors (e.g., chai-spiced gingerbread)

- 3.8.3.2 Dtc e-commerce growth

- 3.8.3.3 Year-round branding (e.g., gingerbread latte campaigns)

- 3.8.3.4 Collaborations (e.g., disney-themed kits)

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 Pestel analysis

- 3.12 Consumer analysis

- 3.12.1 Consumer demographics and target audience profiling

- 3.12.1.1 Age and gender distribution

- 3.12.1.2 Income level analysis

- 3.12.1.3 Geographic distribution

- 3.12.1.4 Lifestyle and psychographic segmentation

- 3.12.2 Consumer buying behavior

- 3.12.2.1 Purchase motivations and triggers

- 3.12.2.2 Seasonal purchasing patterns

- 3.12.2.3 Price sensitivity analysis

- 3.12.2.4 Brand loyalty assessment

- 3.12.3 Consumer preferences

- 3.12.3.1 Flavor and ingredient preferences

- 3.12.3.2 Packaging preferences

- 3.12.3.3 Health and nutrition considerations

- 3.12.3.4 Sustainability and ethical sourcing concerns

- 3.12.4 Consumer trends impacting the market

- 3.12.4.1 Nostalgia and traditional values

- 3.12.4.2 Diy and craft activities

- 3.12.4.3 Social media influence and shareability

- 3.12.4.4 premiumization and gifting trends

- 3.12.1 Consumer demographics and target audience profiling

- 3.13 Manufacturing and technology analysis

- 3.13.1 Production process overview

- 3.13.1.1 Traditional manufacturing methods

- 3.13.1.2 Modern industrial production techniques

- 3.13.1.3 Artisanal and small-batch production

- 3.13.2 Technological innovations in manufacturing

- 3.13.2.1 Automation and robotics integration

- 3.13.2.2 Digital control systems and IoT applications

- 3.13.2.3 3D printing and custom design technologies

- 3.13.2.4 Packaging innovations

- 3.13.3 Quality control and food safety measures

- 3.13.3.1 Critical control points in production

- 3.13.3.2 Testing and monitoring protocols

- 3.13.3.3 Shelf-life extension technologies

- 3.13.3.4 Allergen management systems

- 3.13.4 Supply chain analysis

- 3.13.4.1 Raw material sourcing and supplier networks

- 3.13.4.2 Inventory management strategies

- 3.13.4.3 Distribution and logistics optimization

- 3.13.4.4 Cold chain requirements and challenges

- 3.13.1 Production process overview

- 3.14 Market trends and innovations

- 3.14.1 Product innovation trends

- 3.14.1.1 Health-oriented formulations

- 3.14.1.2 Flavor innovations and fusion concepts

- 3.14.1.3 Functional ingredients and fortification

- 3.14.1.4 Texture and sensory enhancements

- 3.14.2 Packaging and presentation innovations

- 3.14.2.1 Sustainable packaging solutions

- 3.14.2.2 Interactive and smart packaging

- 3.14.2.3 Gift-ready and premium packaging

- 3.14.2.4 Portion control and convenience features

- 3.14.3 Marketing and promotional trends

- 3.14.3.1 Social media and influencer marketing

- 3.14.3.2 Experiential marketing and pop-up concepts

- 3.14.3.3 Seasonal and limited-edition strategies

- 3.14.3.4 Cross-category collaborations

- 3.14.4 Sustainability initiatives

- 3.14.4.1 Sustainable sourcing practices

- 3.14.4.2 Waste reduction strategies

- 3.14.4.3 Carbon footprint reduction

- 3.14.4.4 Ethical labor practices

- 3.14.1 Product innovation trends

- 3.15 Investment analysis and strategic recommendations

- 3.15.1 Investment opportunities assessment

- 3.15.1.1 Production capacity expansion

- 3.15.1.2 Technology upgradation

- 3.15.1.3 New product development

- 3.15.1.4 Geographic expansion

- 3.15.2 Strategic recommendations for manufacturers

- 3.15.2.1 Product portfolio optimization

- 3.15.2.2 Supply chain resilience strategies

- 3.15.2.3 Digital transformation roadmap

- 3.15.2.4 Sustainability integration

- 3.15.3 Strategic recommendations for retailers

- 3.15.3.1 Merchandising and display strategies

- 3.15.3.2 Private label opportunities

- 3.15.3.3 Omnichannel integration

- 3.15.3.4 Seasonal planning optimization

- 3.15.4 Strategic recommendations for new entrants

- 3.15.4.1 Market entry strategies

- 3.15.4.2 Niche targeting approaches

- 3.15.4.3 Partnership and collaboration opportunities

- 3.15.4.4 Scaling and growth strategies

- 3.15.1 Investment opportunities assessment

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Company heat map analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

- 4.7 Recent developments & impact analysis by key players

- 4.7.1 Company categorization

- 4.7.2 Participant’s overview

- 4.7.3 Financial performance

- 4.8 Product benchmarking

Chapter 5 Market Estimates & Forecast, By Product, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Gingerbread cookies

- 5.3 Gingerbread houses and kits

- 5.4 Gingerbread-flavored products

- 5.5 Pre-built decorative items

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Ingredient Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional ingredients

- 6.3 Organic and natural ingredients

- 6.4 Gluten-free variants

- 6.5 Vegan and plant-based options

Chapter 7 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Direct consumption

- 7.3 Decorative and display purposes

- 7.4 Gift and souvenir market

- 7.5 Foodservice applications

Chapter 8 Market Estimates & Forecast, By Distribution channel, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Supermarkets and hypermarkets

- 8.3 Specialty stores and bakeries

- 8.4 Online retail and e-commerce

- 8.5 Convenience Stores

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Packaging Type, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Boxes and cartons

- 9.3 Pouches and bags

- 9.4 Clamshells and trays

- 9.5 Gift packaging

- 9.6 Others

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Pepperidge Farm

- 11.2 Archway Cookies

- 11.3 Stauffer’s

- 11.4 Ginger People

- 11.5 Pamela’s Products

- 11.6 Kinnikinnick Foods

- 11.7 Bahlsen

- 11.8 Lambertz

- 11.9 Niederegger

- 11.10 Hussel

- 11.11 Fortnum & Mason

- 11.12 Biona Organic

- 11.13 Pischinger

- 11.14 Krasny

- 11.15 Gingerbread Folk

- 11.16 Arnott’s Biscuits

- 11.17 Griffin’s

- 11.18 The Gingerbread House

- 11.19 Lebkuchen Schmidt

- 11.20 Daelmans