|

市场调查报告书

商品编码

1750518

即饮茶市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测RTD Tea Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

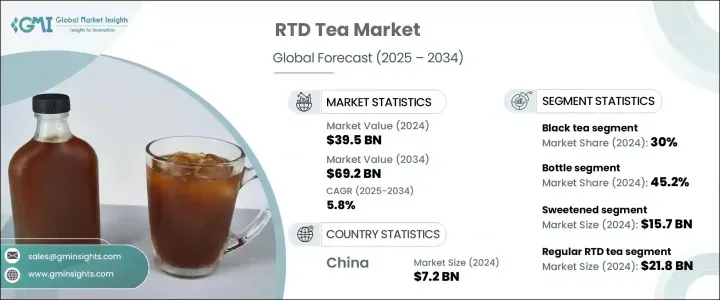

2024年,全球即饮茶市场规模达395亿美元,预计到2034年将以5.8%的复合年增长率增长,达到692亿美元,这得益于消费者健康意识的不断提升以及对便捷饮品的需求不断增长。随着越来越多的人寻求更健康的含糖饮料替代品,即饮茶因其富含绿茶、抹茶和花草茶等天然成分而广受欢迎。消费者越来越青睐清洁标章产品,并寻求能够提供额外健康益处的饮料,例如抗氧化剂、益生菌和适应原。永续性也发挥着重要作用,可回收包装材料已成为影响购买决策的关键因素。

与软性饮料和含糖果汁相比,即饮茶是一种更健康、低卡路里的选择,深受上班族、运动员和注重健康的人士的喜爱。它在超市、便利商店、自动贩卖机和线上平台随处可见,适合所有年龄层的人。根据种类不同,即饮茶具有多种健康益处,从提神醒脑的绿茶和红茶,到帮助消化的草本茶或康普茶。它便于携带、口味多样,且具有许多健康益处,是许多寻求美味便捷饮品的消费者的理想之选。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 395亿美元 |

| 预测值 | 692亿美元 |

| 复合年增长率 | 5.8% |

瓶装包装占据即饮茶市场的最大份额,2024 年将占据 45.2% 的市场份额,预计到 2034 年将以 6% 的复合年增长率稳步增长。瓶装即饮茶之所以受到消费者的青睐,很大程度上得益于其用户友好的设计,尤其是可重复密封的瓶盖,使其成为活跃、忙碌生活方式的理想选择。这些瓶装茶能够有效抵抗外在因素,长期维持产品的口感、新鲜度和营养完整性。瓶装茶结构坚固,易于搬运和储存,特别适用于零售和自动贩卖机环境。

2024年,加糖即饮茶市场规模达157亿美元。这个类别在广泛的消费者群体中引起了强烈共鸣,提供各种口味,既能满足微甜口味,也能满足重甜口味的偏好。其受欢迎程度源自于其清爽的口感和熟悉感,使其成为追求即时口味满足的人士的首选饮品。儘管加糖即饮茶占据主导地位,但随着越来越多注重健康的消费者要求降低糖含量并提供更健康的选择,该细分市场正在逐渐演变。这种转变促使各大品牌不断创新,推出天然甜味剂和低卡路里配方,以平衡享受与健康。

2024年,亚太地区即饮茶市场规模达72亿美元,预计到2034年复合年增长率将达5.6%。中国在该市场的领先地位深深植根于其对茶的文化热爱、强大的国内生产能力以及消费者对功能性茶益处日益增长的认知。随着中国城镇人口的成长和生活节奏的加快,即饮茶的便利性和便携性正成为随时随地补充水分的必需品。此外,传统风味与现代健康益处的融合,使即饮茶成为年轻健康人群的首选饮品。

联合利华、雀巢、三得利控股、百事可乐和可口可乐等公司专注于拓展产品线,尤其是在功能性茶领域。这些公司正在投资永续包装解决方案,提供风味创新,并与当地经销商合作,以加强其在关键市场的影响力。透过提高零售和线上通路的可及性,并专注于以健康为重点的创新,这些公司旨在在不断增长的即饮茶市场中占据更大的份额。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计(HS编码)

- 2021-2024年主要出口国

- 2021-2024年主要进口国

註:以上贸易统计仅针对重点国家。

- 产业价值链分析

- 产品概述

- 茶叶加工方法

- 即饮茶生产流程

- 保存技术

- 风味增强技术

- 市场动态

- 市场驱动因素

- 对健康和功能性饮料的需求不断增长

- 都市化进程加快,生活方式更加忙碌

- 口味和茶混合的创新

- 市场限制

- 来自其他 RTD 饮料的激烈竞争

- 原料(茶叶)价格波动

- 市场机会

- 市场挑战

- 市场驱动因素

- 产业衝击力

- 成长潜力分析

- 产业陷阱与挑战

- 监管框架和标准

- 食品安全法规

- 标籤要求

- 有机和天然产品认证

- 健康声明法规

- 製造流程分析

- 茶叶萃取方法

- 混合和配方

- 巴氏杀菌与保存

- 封装技术

- 原料分析与采购策略

- 定价分析

- 永续性和环境影响评估

- PESTLE 分析

- 波特五力分析

第四章:竞争格局

- 介绍

- 战略框架

- 併购

- 合资与合作

- 新产品开发

- 扩张策略

- 竞争基准测试

- 供应商格局

- 竞争定位矩阵

- 战略仪表板

- 品牌定位与消费者认知分析

- 新参与者的市场进入策略

第五章:市场规模及预测:依产品类型 2021 - 2034

- 主要趋势

- 红茶

- 甜红茶

- 无糖红茶

- 调味红茶

- 绿茶

- 加糖绿茶

- 无糖绿茶

- 调味绿茶

- 凉茶

- 洋甘菊

- 薄荷

- 路易波士茶

- 其他草药茶

- 水果茶

- 柑橘

- 莓果

- 热带

- 混合水果

- 乌龙茶

- 白茶

- 抹茶

- 康普茶

- 其他

第六章:市场规模及预测:依包装,2021 - 2034

- 主要趋势

- 瓶子

- PET瓶

- 玻璃瓶

- 其他瓶型

- 罐头

- 铝罐

- 钢罐

- 纸箱

- 无菌纸盒

- 山墙顶纸箱

- 袋装

- 其他

第七章:市场规模及预测:依甜度划分,2021 - 2034

- 主要趋势

- 加糖

- 普通糖

- 高果糖玉米糖浆

- 蜂蜜和天然甜味剂

- 减少糖

- 无醣

- 人工甜味剂

- 阿斯巴甜

- 三氯蔗糖

- 甜菊糖

- 其他

第八章:市场规模及预测:依功能优势,2021 - 2034 年

- 主要趋势

- 一般即饮茶

- 强化即饮茶

- 富含维生素

- 富含矿物质

- 抗氧化增强

- 功能性即饮茶

- 提升能量

- 免疫支持

- 消化健康

- 放鬆和缓解压力

- 有机即饮茶

- 清洁标籤即饮茶

第九章:市场规模及预测:按配销通路,2021 - 2034

- 主要趋势

- 超市和大卖场

- 便利商店

- 专卖店

- 网路零售

- 餐饮服务

- 咖啡馆和餐厅

- 速食连锁店

- 机构餐饮

- 自动贩卖机

- 其他

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲的Rets

第 11 章:公司简介

- The Coca-Cola Company

- PepsiCo, Inc

- Unilever PLC

- Nestle SA

- Suntory Holdings Limited

- ITO EN, Ltd.

- Danone SA

- Arizona Beverages USA

- Keurig Dr Pepper Inc.

- Tata Consumer Products Limited

- Starbucks Corporation

- Honest Tea (Coca-Cola)

- Lipton (Unilever/PepsiCo)

- Tejava (Crystal Geyser Water Company)

- Harney & Sons

- The Republic of Tea

- Numi Organic Tea

- Pokka Corporation

- Oi Ocha (ITO EN)

- Vita Coco

- GT's Living Foods (Kombucha)

- Health-Ade Kombucha

- Steaz

- Pure Leaf (Unilever/PepsiCo)

- Gold Peak (Coca-Cola)

- Snapple (Keurig Dr Pepper)

- Tazo (Unilever)

- Fuze Tea (Coca-Cola)

The Global RTD Tea Market was valued at USD 39.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 69.2 billion by 2034, driven by increasing health awareness among consumers and the rising demand for convenient beverage options. As more people look for healthier alternatives to sugary drinks, RTD tea has gained popularity for its natural ingredients like green tea, matcha, and herbal teas. There is a growing preference for clean-label products, and consumers are seeking beverages that offer added health benefits such as antioxidants, probiotics, and adaptogens. Sustainability also plays a significant role, with recyclable packaging materials becoming a key factor in purchasing decisions.

RTD tea serves as a healthier, low-calorie option compared to soft drinks and sugary juices, making it a favorite among office workers, athletes, and health-conscious individuals. It is widely accessible through supermarkets, convenience stores, vending machines, and online platforms, catering to people of all ages. Depending on the variant, RTD tea offers various health benefits, from boosting mental alertness with green and black teas to aiding digestion with herbal or kombucha options. Its portability, variety of flavors, and health advantages make it an ideal choice for many consumers looking for a tasty, convenient drink.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $39.5 Billion |

| Forecast Value | $69.2 Billion |

| CAGR | 5.8% |

The bottle-based packaging segment commands the largest portion of the RTD tea market, holding a substantial 45.2% share in 2024 and projected to grow steadily at a 6% CAGR through 2034. Bottled RTD teas are preferred by consumers largely due to their user-friendly design, particularly the resealable caps that make them ideal for active, on-the-go lifestyles. These bottles offer superior protection against external elements, preserving the product's taste, freshness, and nutritional integrity over time. Their sturdy build, easy handling, and storage, especially in retail and vending environments.

The sweetened RTD tea segment generated USD 15.7 billion in 2024. This category resonates strongly with a wide consumer base, offering a variety of flavors that cater to both mildly sweet and heavily sweetened preferences. Its popularity stems from its refreshing taste and familiarity, making it a go-to beverage for those seeking instant gratification in flavor. Despite its dominance, the segment is gradually evolving as more health-conscious consumers demand reduced sugar content and better-for-you options. This shift has prompted brands to innovate with naturally sweetened and low-calorie formulations to balance indulgence with wellness.

Asia-Pacific RTD Tea Market generated USD 7.2 billion in 2024 and is anticipated to have a CAGR of 5.6% through 2034. China's leadership in the market is deeply rooted in its cultural affinity for tea, strong domestic production capabilities, and increasing consumer awareness around the benefits of functional teas. As the nation's urban population grows and lifestyles become more fast-paced, the convenience and portability of RTD teas are becoming essential for on-the-go hydration. Additionally, the fusion of traditional flavors with modern health benefits has positioned RTD teas as a preferred beverage among the younger, health-aware population.

Companies like Unilever PLC, Nestle S.A., Suntory Holdings, PepsiCo Inc., and The Coca-Cola Company focus on expanding their product ranges, particularly in the functional tea segment. These companies are investing in sustainable packaging solutions, offering flavors, and partnering with local distributors to strengthen their presence in key markets. By improving accessibility through retail and online channels and focusing on health-focused innovations, these players aim to capture more of the growing RTD tea market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS Code)

- 3.3.1 Major exporting countries, 2021-2024 (Kilo Tons)

- 3.3.2 Major importing countries, 2021-2024 (Kilo Tons)

Note: the above trade statistics will be provided for key countries only.

- 3.4 Industry value chain analysis

- 3.5 Product overview

- 3.5.1 Tea processing methods

- 3.5.2 RTD tea production process

- 3.5.3 Preservation technologies

- 3.5.4 Flavor enhancement techniques

- 3.6 Market dynamics

- 3.6.1 Market drivers

- 3.6.1.1 Rising demand for healthy and functional beverages

- 3.6.1.2 Increasing urbanization and busy lifestyles

- 3.6.1.3 Innovation in flavors and tea blends

- 3.6.2 Market Restraints

- 3.6.2.1 High competition from other RTD beverages

- 3.6.2.2 Fluctuating raw material (tea leaf) prices

- 3.6.3 Market opportunities

- 3.6.4 Market challenges

- 3.6.1 Market drivers

- 3.7 Industry impact forces

- 3.7.1 Growth potential analysis

- 3.7.2 Industry pitfalls & challenges

- 3.8 Regulatory framework & standards

- 3.8.1 Food safety regulations

- 3.8.2 Labeling requirements

- 3.8.3 Organic & natural product certifications

- 3.8.4 Health claim regulations

- 3.9 Manufacturing process analysis

- 3.9.1 Tea extraction methods

- 3.9.2 Blending & formulation

- 3.9.3 Pasteurization & preservation

- 3.9.4 Packaging technologies

- 3.10 Raw material analysis & procurement strategies

- 3.11 Pricing analysis

- 3.12 Sustainability & environmental impact assessment

- 3.13 PESTLE analysis

- 3.14 Porter's Five Forces Analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic framework

- 4.2.1 Mergers & acquisitions

- 4.2.2 Joint ventures & collaborations

- 4.2.3 New product developments

- 4.2.4 Expansion strategies

- 4.3 Competitive benchmarking

- 4.4 Vendor landscape

- 4.5 Competitive positioning matrix

- 4.6 Strategic dashboard

- 4.7 Brand positioning & consumer perception analysis

- 4.8 Market entry strategies for new players

Chapter 5 Market Size and Forecast, By Product Type 2021 - 2034 (USD Billion, Kilo Tons)

- 5.1 Key trends

- 5.2 Black tea

- 5.2.1 Sweetened black tea

- 5.2.2 Unsweetened black tea

- 5.2.3 Flavored black tea

- 5.3 Green tea

- 5.3.1 Sweetened green tea

- 5.3.2 Unsweetened green tea

- 5.3.3 Flavored green tea

- 5.4 Herbal tea

- 5.4.1 Chamomile

- 5.4.2 Mint

- 5.4.3 Rooibos

- 5.4.4 Other herbal teas

- 5.5 Fruit tea

- 5.5.1 Citrus

- 5.5.2 Berry

- 5.5.3 Tropical

- 5.5.4 Mixed fruit

- 5.6 Oolong Tea

- 5.7 White Tea

- 5.8 Matcha Tea

- 5.9 Kombucha

- 5.10 Other

Chapter 6 Market Size and Forecast, By Packaging, 2021 - 2034 (USD Billion, Kilo Tons)

- 6.1 Key trends

- 6.2 Bottles

- 6.2.1 PET bottles

- 6.2.2 Glass bottles

- 6.2.3 Other bottle types

- 6.3 Cans

- 6.3.1 Aluminum cans

- 6.3.2 Steel cans

- 6.4 Cartons

- 6.4.1 Aseptic cartons

- 6.4.2 Gable top cartons

- 6.5 Pouches

- 6.6 Other

Chapter 7 Market Size and Forecast, By Sweetness Level, 2021 - 2034 (USD Billion, Kilo Tons)

- 7.1 Key trend

- 7.2 Sweetened

- 7.2.1 Regular sugar

- 7.2.2 High fructose corn syrup

- 7.2.3 Honey & natural sweeteners

- 7.3 Reduced sugar

- 7.4 Unsweetened

- 7.5 Artificially sweetened

- 7.5.1 Aspartame

- 7.5.2 Sucralose

- 7.5.3 Stevia

- 7.5.4 Other

Chapter 8 Market Size and Forecast, By Functional Benefits, 2021 - 2034 (USD Billion, Kilo Tons)

- 8.1 Key trend

- 8.2 Regular RTD tea

- 8.3 Fortified RTD tea

- 8.3.1 Vitamin-enriched

- 8.3.2 Mineral-enriched

- 8.3.3 Antioxidant-enhanced

- 8.4 Functional RTD tea

- 8.4.1 Energy-boosting

- 8.4.2 Immunity-supporting

- 8.4.3 Digestive health

- 8.4.4 Relaxation & stress relief

- 8.5 Organic RTD tea

- 8.6 Clean Label RTD tea

Chapter 9 Market Size and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion, Kilo Tons)

- 9.1 Key trend

- 9.2 Supermarkets & hypermarkets

- 9.3 Convenience stores

- 9.4 Specialty stores

- 9.5 Online retail

- 9.6 Foodservice

- 9.6.1 Cafes & restaurants

- 9.6.2 Fast food chains

- 9.6.3 Institutional catering

- 9.7 Vending machines

- 9.8 Other

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rets of Middle East & Africa

Chapter 11 Company Profiles

- 11.1 The Coca-Cola Company

- 11.2 PepsiCo, Inc

- 11.3 Unilever PLC

- 11.4 Nestle S.A.

- 11.5 Suntory Holdings Limited

- 11.6 ITO EN, Ltd.

- 11.7 Danone S.A.

- 11.8 Arizona Beverages USA

- 11.9 Keurig Dr Pepper Inc.

- 11.10 Tata Consumer Products Limited

- 11.11 Starbucks Corporation

- 11.12 Honest Tea (Coca-Cola)

- 11.13 Lipton (Unilever/PepsiCo)

- 11.14 Tejava (Crystal Geyser Water Company)

- 11.15 Harney & Sons

- 11.16 The Republic of Tea

- 11.17 Numi Organic Tea

- 11.18 Pokka Corporation

- 11.19 Oi Ocha (ITO EN)

- 11.20 Vita Coco

- 11.21 GT's Living Foods (Kombucha)

- 11.22 Health-Ade Kombucha

- 11.23 Steaz

- 11.24 Pure Leaf (Unilever/PepsiCo)

- 11.25 Gold Peak (Coca-Cola)

- 11.26 Snapple (Keurig Dr Pepper)

- 11.27 Tazo (Unilever)

- 11.28 Fuze Tea (Coca-Cola)