|

市场调查报告书

商品编码

1755214

电致变色材料市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Electrochromic Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

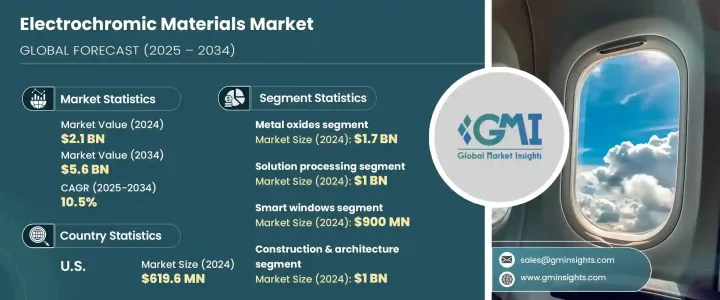

2024年,全球电致变色材料市场规模达21亿美元,预计2034年将以10.5%的复合年增长率成长,达到56亿美元。这得归功于住宅和商业建筑中日益普及的智慧窗户需求的不断增长。智慧窗户透过控制光和热来帮助降低能耗,使其成为旨在满足能源效率标准的绿色建筑专案的关键组成部分。

此外,电致变色材料在汽车产业的应用日益广泛,尤其是在自动调光后视镜、自适应天窗和侧窗领域。这些创新不仅提升了用户舒适度、减少了眩光,也提升了汽车品牌形象。包括导电聚合物和混合复合材料在内的材料科学的进步,提高了电致变色材料的性能和成本效益,推动了其应用。随着节能日益重要,尤其是在永续发展标准严格的地区,对这些材料的需求正在大幅增长。它们能够提高能源效率,使其成为各种应用的关键组成部分,并成为寻求降低能耗的行业的重要解决方案。从旨在获得绿色认证的建筑项目到专注于提高燃油效率的汽车应用,这些材料在实现环境和经济目标方面发挥着至关重要的作用。它们的多功能性、日益增长的监管压力以及消费者对永续解决方案的需求,推动了它们的广泛应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 21亿美元 |

| 预测值 | 56亿美元 |

| 复合年增长率 | 10.5% |

2024年,溶液加工细分市场规模达10亿美元,预计到2034年将以9.6%的复合年增长率成长。这一增长得益于溶液加工方法的成本效益和可扩展性,这些方法在智慧窗户和显示器等应用领域的应用日益广泛。这些方法用途广泛,可与各种基材相容,进一步推动建筑和汽车行业的成长。

智慧窗户市场规模预计在2024年将达到9亿美元,预计也将在节能产品需求不断增长的推动下快速成长。这些窗户有助于降低建筑能耗,提升舒适度。智慧镜子和天窗因其舒适性和安全性而日益普及。

2024年,美国电致变色材料市场规模达6.196亿美元,预计到2034年将以10%的复合年增长率成长,这得益于智慧建筑和汽车领域对节能技术日益增长的需求。美国市场受益于政府对永续性和节能技术的强大监管,以及产业领导者积极参与,推动创新和技术进步。

全球电致变色材料市场的主要参与者包括 Gentex Corporation、AGC Inc.、Sage Electrochromics, Inc. (Saint-Gobain)、PPG Industries, Inc. 和 View, Inc. 为了巩固其在电致变色材料市场的地位,各公司正专注于多种策略。一个关键方法是持续投资研发,以创造创新的高效能产品,满足日益增长的节能应用需求。透过提高电致变色材料的性能,公司旨在增强其市场竞争力。许多公司正在扩展其产品组合,包括用于住宅、商业和汽车应用的智慧窗户解决方案。此外,与建筑公司、汽车製造商和政府建立合作伙伴关係对于获得新的市场机会和确保将这些技术整合到大型专案中至关重要。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 市场介绍

- 川普政府关税的影响—结构化概述

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 贸易统计资料(HS 编码) 註:以上贸易统计仅提供主要国家。

- 主要出口国

- 国家 1

- 国家 2

- 国家 3

- 主要进口国

- 国家 1

- 国家 2

- 国家 3

- 主要出口国

- 产业价值链分析

- 材料概述

- 电致变色:原理与机制

- 氧化还原反应和颜色变化过程

- 光调製特性

- 切换速度和着色效率

- 耐用性和循环稳定性

- 能源效率特性

- 与其他智慧材料的比较

- 市场动态

- 市场驱动因素

- 节能智慧窗户需求不断增长

- 在汽车应用的采用率不断提高

- 电致变色材质的技术进步

- 日益重视绿建筑认证

- 市场限制

- 电致变色装置的初始成本高

- 某些材料类型的切换速度有限

- 市场机会

- 市场挑战

- 市场驱动因素

- 产业衝击力

- 成长潜力分析

- 产业陷阱与挑战

- 监管框架和标准

- 能源效率法规

- 建筑规范和标准

- 汽车安全标准

- 环境法规

- 性能测试标准

- 製造流程分析

- 材料合成方法

- 薄膜沉积技术

- 装置製造工艺

- 品质控製程式

- 原料分析与采购策略

- 定价分析

- 永续性和环境影响评估

- 杵分析

- 波特五力分析

第四章:竞争格局

- 市占率分析

- 战略框架

- 併购

- 合资与合作

- 新产品开发

- 扩张策略

- 竞争基准化分析

- 供应商格局

- 竞争定位矩阵

- 战略仪表板

- 专利分析与创新评估

- 新参与者的市场进入策略

- 研发强度分析

第五章:市场估计与预测:依材料类型,2021 年至 2034 年

- 主要趋势

- 金属氧化物

- 氧化钨(WO3)

- 氧化镍(NiO)

- 二氧化钛(TiO2)

- 五氧化二钒(V2O5)

- 氧化钼(MoO3)

- 其他金属氧化物

- 导电聚合物

- 聚苯胺(PANI)

- 聚吡咯(PPy)

- 聚(3,4-乙撑二氧噻吩)(PEDOT)

- 其他导电聚合物

- 紫罗兰碱

- 普鲁士蓝类似物

- 液晶

- 混合及复合材料

- 其他电致变色材料

第六章:市场估计与预测:按技术,2021 年至 2034 年

- 主要趋势

- 溶液处理

- 溶胶-凝胶法

- 电沉积

- 旋涂

- 其他溶液处理方法

- 气相沉积

- 物理气相沉积(PVD)

- 化学气相沉积(CVD)

- 溅射

- 其他气相沉积方法

- 印刷技术

- 喷墨列印

- 网版印刷

- 其他印刷方法

- 其他技术

第七章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 智慧窗户

- 建筑窗户

- 天窗和屋顶窗

- 隔间和隐私玻璃

- 其他智慧窗应用

- 智慧镜子

- 汽车后视镜

- 建筑镜子

- 其他镜子应用

- 显示器

- 电子纸显示器

- 资讯显示

- 其他显示应用

- 汽车应用

- 天窗

- 后视镜

- 侧窗

- 其他汽车应用

- 航太应用

- 穿戴式装置

- 储能设备

- 其他应用

第八章:市场估计与预测:按最终用途产业,2021 年至 2034 年

- 主要趋势

- 建筑与建筑

- 住宅建筑

- 商业建筑

- 机构建筑

- 其他建筑类型

- 汽车与运输

- 搭乘用车

- 商用车

- 其他交通

- 航太与国防

- 电子产品和显示器

- 海洋

- 医疗保健

- 其他最终用途产业

第九章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十章:公司简介

- Gentex Corporation

- View, Inc.

- ChromoGenics AB

- Sage Electrochromics, Inc. (Saint-Gobain)

- AGC Inc.

- Magna Glass and Window Company

- Guardian Industries Corp.

- PPG Industries, Inc.

- Kinestral Technologies, Inc.

- E Ink Holdings Inc.

- Gesimat GmbH

- EControl-Glas GmbH & Co. KG

- Merck KGaA

- 3M Company

- Nippon Sheet Glass Co., Ltd.

- Halio, Inc.

- Pleotint LLC

- Research Frontiers Inc.

- Heliotrope Technologies

- SAGE Electrochromics, Inc.

- Polytronix, Inc.

- Chromogenics AB

- Innovative Glass Corporation

- Gauzy Ltd.

- Smart Glass International Ltd.

- SPD Control Systems Corporation

- Diamond Glass

- InvisiShade

- Continental AG

The Global Electrochromic Materials Market was valued at USD 2.1 billion in 2024 and is estimated to grow at a CAGR of 10.5% to reach USD 5.6 billion by 2034, driven by the increasing demand for smart windows, which are gaining popularity in both residential and commercial buildings. These windows help reduce energy consumption by controlling light and heat, making them a key component in green building projects aiming to meet energy efficiency standards.

Additionally, electrochromic materials are seeing increased applications in the automotive industry, particularly in self-dimming mirrors, adaptive sunroofs, and side windows. These innovations not only improve user comfort and reduce glare but also enhance vehicle branding. The advancement of material science, including conducting polymers and hybrid composites, has improved the performance and cost-efficiency of electrochromic materials, driving their adoption. As energy conservation gains importance, particularly in regions with stringent sustainability standards, the demand for these materials is experiencing a significant surge. Their ability to enhance energy efficiency makes them a key component in applications, positioning them as a vital solution for industries seeking to reduce energy consumption. From construction projects aiming for green certifications to automotive applications focused on improving fuel efficiency, these materials play a crucial role in meeting environmental and economic goals. Their versatility, growing regulatory pressure, and consumer demand for sustainable solutions, drive their widespread adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.1 Billion |

| Forecast Value | $5.6 Billion |

| CAGR | 10.5% |

In 2024, the solution processing segment accounted for USD 1 billion and is expected to grow at a CAGR of 9.6% through 2034. This growth is attributed to the cost-effectiveness and scalability of solution processing methods, which are increasingly used for applications like smart windows and displays. These methods offer versatility, making them compatible with a wide range of substrates, further boosting growth in the architectural and automotive sectors.

The smart windows segment, valued at USD 900 million in 2024, is also projected to expand rapidly, driven by the growing demand for energy-efficient products. These windows help reduce energy consumption in buildings and enhance comfort. Smart mirrors and sunroofs are gaining popularity for their comfort and safety benefits.

U.S. Electrochromic Materials Market was valued at USD 619.6 million in 2024 and is expected to grow at a 10% CAGR through 2034 driven by the increasing demand for energy-saving technologies in smart buildings and vehicles. The U.S. market benefits from strong governmental regulations focused on sustainability and energy-efficient technologies, and the active involvement of leading industry players driving innovation and technical advancements.

Key players in the Global Electrochromic Materials Market include Gentex Corporation, AGC Inc., Sage Electrochromics, Inc. (Saint-Gobain), PPG Industries, Inc., and View, Inc. To strengthen their position in the electrochromic materials market, companies are focusing on multiple strategies. One key approach is the continued investment in research and development to create innovative, high-performance products that cater to the growing demand for energy-efficient applications. By advancing the capabilities of electrochromic materials, companies aim to enhance their market competitiveness. Many are expanding their product portfolios to include smart window solutions for residential, commercial, and automotive applications. In addition, partnerships with construction firms, automotive manufacturers, and governments are vital for securing new market opportunities and ensuring the integration of these technologies into large-scale projects.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research methodology

- 1.2 Research scope & assumptions

- 1.3 List of data sources

- 1.4 Market estimation technique

- 1.5 Market segmentation & breakdown

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Market snapshot

- 2.2 Segment highlights

- 2.3 Competitive landscape snapshot

- 2.4 Regional market outlook

- 2.5 Key market trends

- 2.6 Future market outlook

Chapter 3 Industry Insights

- 3.1 Market Introduction

- 3.2 Impact of trump administration tariffs – structured overview

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1.1 Supply-side impact (raw materials)

- 3.2.2.1.2 Price volatility in key materials

- 3.2.2.1.3 Supply chain restructuring

- 3.2.2.1.4 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (hs code) Note: The above trade statistics will be provided for key countries only.

- 3.3.1 Major exporting countries

- 3.3.1.1 Country 1

- 3.3.1.2 Country 2

- 3.3.1.3 Country 3

- 3.3.2 Major importing countries

- 3.3.2.1 Country 1

- 3.3.2.2 Country 2

- 3.3.2.3 Country 3

- 3.3.1 Major exporting countries

- 3.4 Industry value chain analysis

- 3.5 Material overview

- 3.5.1 Electrochromism: principles & mechanisms

- 3.5.2 Redox reactions & color change processes

- 3.5.3 Optical modulation properties

- 3.5.4 Switching speed & coloration efficiency

- 3.5.5 Durability & cycling stability

- 3.5.6 Energy efficiency characteristics

- 3.5.7 Comparison with other smart materials

- 3.6 Market dynamics

- 3.6.1 Market drivers

- 3.6.1.1 Rising demand for energy-efficient smart windows

- 3.6.1.2 Increasing adoption in automotive applications

- 3.6.1.3 Technological advancements in electrochromic materials

- 3.6.1.4 Growing emphasis on green building certifications

- 3.6.2 Market restraints

- 3.6.2.1 High initial cost of electrochromic devices

- 3.6.2.2 Limited switching speed for some material types

- 3.6.3 Market opportunities

- 3.6.4 Market challenges

- 3.6.1 Market drivers

- 3.7 Industry impact forces

- 3.7.1 Growth potential analysis

- 3.7.2 Industry pitfalls & challenges

- 3.8 Regulatory framework & standards

- 3.9 Energy efficiency regulations

- 3.9.1 Building codes & standards

- 3.9.2 Automotive safety standards

- 3.9.3 Environmental regulations

- 3.9.4 Performance testing standards

- 3.10 Manufacturing process analysis

- 3.10.1 Material synthesis methods

- 3.10.2 Thin film deposition techniques

- 3.10.3 Device fabrication processes

- 3.10.4 Quality control procedures

- 3.11 Raw material analysis & procurement strategies

- 3.12 Pricing analysis

- 3.13 Sustainability & environmental impact assessment

- 3.14 Pestle analysis

- 3.15 Porter's five forces analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Market Share Analysis

- 4.2 Strategic Framework

- 4.2.1 Mergers & Acquisitions

- 4.2.2 Joint Ventures & Collaborations

- 4.2.3 New Product Developments

- 4.2.4 Expansion Strategies

- 4.3 Competitive Benchmarking

- 4.4 Vendor Landscape

- 4.5 Competitive Positioning Matrix

- 4.6 Strategic Dashboard

- 4.7 Patent Analysis & Innovation Assessment

- 4.8 Market Entry Strategies for New Players

- 4.9 Research & Development Intensity Analysis

Chapter 5 Market Estimates and Forecast, By Material Type, 2021 – 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Metal oxides

- 5.2.1 Tungsten oxide (WO3)

- 5.2.2 Nickel oxide (NiO)

- 5.2.3 Titanium dioxide (TiO2)

- 5.2.4 Vanadium pentoxide (V2O5)

- 5.2.5 Molybdenum oxide (MoO3)

- 5.2.6 Other metal oxides

- 5.3 Conducting polymers

- 5.3.1 Polyaniline (PANI)

- 5.3.2 Polypyrrole (PPy)

- 5.3.3 Poly(3,4-ethylenedioxythiophene) (PEDOT)

- 5.3.4 Other conducting polymers

- 5.4 Viologens

- 5.5 Prussian blue analogs

- 5.6 Liquid crystals

- 5.7 Hybrid & composite materials

- 5.8 Other electrochromic materials

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Solution processing

- 6.2.1 Sol-gel method

- 6.2.2 Electrodeposition

- 6.2.3 Spin coating

- 6.2.4 Other solution processing methods

- 6.3 Vapor deposition

- 6.3.1 Physical vapor deposition (PVD)

- 6.3.2 Chemical vapor deposition (CVD)

- 6.3.3 Sputtering

- 6.3.4 Other vapor deposition methods

- 6.4 Printing technologies

- 6.4.1 Inkjet printing

- 6.4.2 Screen printing

- 6.4.3 Other printing methods

- 6.5 Other technologies

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Smart windows

- 7.2.1 Architectural windows

- 7.2.2 Skylights & roof windows

- 7.2.3 Partitions & privacy glass

- 7.2.4 Other smart window applications

- 7.3 Smart mirrors

- 7.3.1 Automotive mirrors

- 7.3.2 Architectural mirrors

- 7.3.3 Other mirror applications

- 7.4 Displays

- 7.4.1 E-paper displays

- 7.4.2 Information displays

- 7.4.3 Other display applications

- 7.5 Automotive applications

- 7.5.1 Sunroofs

- 7.5.2 Rearview mirrors

- 7.5.3 Side windows

- 7.5.4 Other automotive applications

- 7.6 Aerospace applications

- 7.7 Wearable devices

- 7.8 Energy storage devices

- 7.9 Other applications

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 – 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Construction & architecture

- 8.2.1 Residential buildings

- 8.2.2 Commercial buildings

- 8.2.3 Institutional buildings

- 8.2.4 Other building types

- 8.3 Automotive & transportation

- 8.3.1 Passenger vehicles

- 8.3.2 Commercial vehicles

- 8.3.3 Other transportation

- 8.4 Aerospace & defense

- 8.5 Electronics & displays

- 8.6 Marine

- 8.7 Healthcare & medical

- 8.8 Other end-use industries

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Gentex Corporation

- 10.2 View, Inc.

- 10.3 ChromoGenics AB

- 10.4 Sage Electrochromics, Inc. (Saint-Gobain)

- 10.5 AGC Inc.

- 10.6 Magna Glass and Window Company

- 10.7 Guardian Industries Corp.

- 10.8 PPG Industries, Inc.

- 10.9 Kinestral Technologies, Inc.

- 10.10 E Ink Holdings Inc.

- 10.11 Gesimat GmbH

- 10.12 EControl-Glas GmbH & Co. KG

- 10.13 Merck KGaA

- 10.14 3M Company

- 10.15 Nippon Sheet Glass Co., Ltd.

- 10.16 Halio, Inc.

- 10.17 Pleotint LLC

- 10.18 Research Frontiers Inc.

- 10.19 Heliotrope Technologies

- 10.20 SAGE Electrochromics, Inc.

- 10.21 Polytronix, Inc.

- 10.22 Chromogenics AB

- 10.23 Innovative Glass Corporation

- 10.24 Gauzy Ltd.

- 10.25 Smart Glass International Ltd.

- 10.26 SPD Control Systems Corporation

- 10.27 Diamond Glass

- 10.28 InvisiShade

- 10.29 Continental AG

2026年全球电动变色智慧玻璃市场报告

2026年全球电动变色智慧玻璃市场报告 电致变色材料市场:按材料、应用、最终用户和产品划分-2026-2032年全球市场预测电致变色玻璃及装置市场:按产品类型、技术、安装方式、控制模式和最终用途分類的全球预测,2026年至2032年

电致变色材料市场:按材料、应用、最终用户和产品划分-2026-2032年全球市场预测电致变色玻璃及装置市场:按产品类型、技术、安装方式、控制模式和最终用途分類的全球预测,2026年至2032年 电致变色材料市场规模、份额及成长分析(按产品、应用、最终用户及地区划分)-产业预测,2026-2033年

电致变色材料市场规模、份额及成长分析(按产品、应用、最终用户及地区划分)-产业预测,2026-2033年 电致变色玻璃市场规模、份额及成长分析(依材料、产品、终端用户产业及地区划分)-2026-2033年产业预测

电致变色玻璃市场规模、份额及成长分析(依材料、产品、终端用户产业及地区划分)-2026-2033年产业预测 电致变色玻璃市场 - 预测 2025-2030

电致变色玻璃市场 - 预测 2025-2030 全球电致变色材料市场

全球电致变色材料市场 电致变色材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年)

电致变色材料:市场份额分析、行业趋势、统计数据和成长预测(2025-2030 年) 电致变色玻璃市场:按应用、最终用途和地区划分

电致变色玻璃市场:按应用、最终用途和地区划分 电致变色智慧玻璃系统市场机会、成长动力、产业趋势分析与预测 2024 - 2032

电致变色智慧玻璃系统市场机会、成长动力、产业趋势分析与预测 2024 - 2032