|

市场调查报告书

商品编码

1755308

汽车内部环境照明系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Automotive Interior Ambient Lighting System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

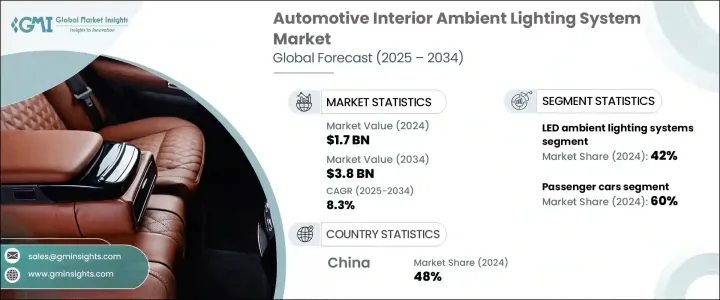

2024 年全球汽车内部环境照明系统市值为 17 亿美元,预计到 2034 年将以 8.3% 的复合年增长率增长,达到 38 亿美元,这得益于消费者对提升车内舒适度和美观度的需求不断增长、高檔汽车普及率不断上升以及 LED 和 OLED 等照明技术的进步。这些技术使得可客製化、节能且外观吸引人的照明解决方案成为可能。印度、中国、巴西和东南亚等新兴市场的汽车产业扩张促进了对包括环境照明在内的先进车载功能的需求。随着可支配收入的增加和城市化进程的加快,消费者越来越寻求能够提供个人化驾驶体验的汽车,这促使汽车製造商整合时尚且可自订的车内照明,从而促进市场成长。

LED技术凭藉其高能源效率、更长的使用寿命以及设计灵活性,在这一成长中发挥着重要作用。与传统照明解决方案相比,LED更节能,亮度更高。此外,其紧凑的尺寸支持创新的内装设计,有助于汽车製造商提升车辆的美观和功能性。 OLED和LED创新对于提升汽车内装的吸引力、提高安全性、满足消费者对高端功能的需求以及降低能源消耗至关重要。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 17亿美元 |

| 预测值 | 38亿美元 |

| 复合年增长率 | 8.3% |

2024年,LED环境照明系统市场占有42%的份额,预计2034年的复合年增长率将达到9%。 LED技术的普及得益于其低功耗、更长的使用寿命和灵活的设计。 LED灯的优点尤其在于其可提供可自订的色彩选项和动态照明效果,从而提升车内美学体验。对于希望在竞争激烈的市场中脱颖而出的汽车製造商来说,这种客製化功能是一个强大的卖点。由于能够将这些灯整合到中阶车型中,对于那些希望以较低成本提供豪华配置的汽车製造商来说,LED灯是一个相当吸引人的选择。

2024年,乘用车市场占了60%的市场份额,这得益于高产量以及消费者对舒适性、安全性和美观性日益增长的需求。随着可支配收入的增加,消费者越来越追求能够提供高端驾驶体验的车辆。气氛灯可以增强车内环境,已成为高端和大众市场汽车的关键配置。汽车製造商正在扩大此类照明系统在紧凑型和中檔车等一系列车型中的应用,以吸引更年轻、更精通科技的买家。诸如可自订颜色、与娱乐系统同步以及车门照明增强等功能正成为标配。

中国汽车内装气氛照明系统市场占48%的市场份额,2024年市场规模达4.482亿美元,这得益于消费者对个人化座舱体验的偏好、技术进步以及政府扶持政策的推动。电动车对先进氛围照明系统的需求尤其强劲,製造商正在整合尖端照明功能,以增强内装的未来感。政府推出的节能技术奖励措施也推动了LED照明系统的普及,从而促进了兼顾美观和驾驶员安全性的氛围照明解决方案的成长。

汽车内部环境照明系统市场的主要参与者包括法雷奥、史丹利电气、Innotec Group、玛涅蒂·马瑞利、小纟製作所、欧司朗、Lumileds Holding、麦格纳国际和海拉。为了巩固市场地位,汽车内部环境照明系统产业的公司正专注于产品创新,尤其是在 LED 和 OLED 等节能照明技术方面。製造商正在扩展其产品组合,以包括可自订的照明解决方案,以增强车辆美感并满足消费者对个人化车内体验的需求。此外,这些公司正在投资研发,以提高能源效率,延长照明系统的使用寿命,并创造有助于提升驾驶体验的动态照明效果。与汽车製造商建立策略合作伙伴关係也至关重要,因为这些合作有助于将先进的照明功能整合到各种车型中。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 原物料供应商

- 零件製造商

- 系统整合商

- 技术提供者

- OEM

- 售后市场供应商和经销商

- 利润率分析

- 川普政府关税

- 对贸易的影响

- 贸易量中断

- 其他国家的报復措施

- 对产业的影响

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 展望与未来考虑

- 对贸易的影响

- 技术与创新格局

- 价格趋势

- 按产品

- 按地区

- 成本細項分析

- 专利分析

- 重要新闻和倡议

- 监管格局

- 衝击力

- 成长动力

- 车辆个性化需求不断成长

- 照明技术进步

- 新兴市场汽车产业快速成长

- 增强美感和舒适度

- 安全和驾驶辅助功能

- 产业陷阱与挑战

- 初始成本高

- 安装维护复杂

- 成长动力

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 竞争定位矩阵

- 战略展望矩阵

第五章:市场估计与预测:依产品,2021 - 2034 年

- 主要趋势

- LED 环境照明系统

- OLED环境照明系统

- 光纤环境照明系统

- 雷射环境照明系统

第六章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 搭乘用车

- 掀背车

- 轿车

- 越野车

- 商用车

- 轻型商用车

- 中型商用车

- 重型商用车

- 电动车(Evs)

第七章:市场估计与预测:按安装区域,2021 - 2034 年

- 主要趋势

- 仪表板照明

- 脚部空间照明

- 门板照明

- 其他的

第八章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- OEM

- 售后市场安装

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第十章:公司简介

- CML Innovative

- HELLA

- Innotec Group

- Jiangsu Jingliang

- Koito Electric

- Koito Manufacturing

- Lumenpulse

- Lumileds Holding

- Magna International

- Magneti Marelli

- Mitsubishi Electric

- OSRAM

- Stanley Electric

- STANLEY Electric

- TCL Automotive

- Valeo

- Varroc Lighting Systems

- Wells Vehicle Electronics

- Xenon Automotives

- ZKW Group

The Global Automotive Interior Ambient Lighting System Market was valued at USD 1.7 billion in 2024 and is estimated to grow at a CAGR of 8.3% to reach USD 3.8 billion by 2034, driven by increasing consumer demand for enhanced in-vehicle comfort and aesthetics, rising adoption of premium vehicles, and advancements in lighting technologies like LED and OLED. These technologies allow for customizable, energy-efficient, and visually appealing lighting solutions. The expansion of the automotive sector in emerging markets such as India, China, Brazil, and Southeast Asia contributes to the demand for advanced in-vehicle features, including ambient lighting. With rising disposable incomes and urbanization, consumers are increasingly seeking vehicles that offer personalized driving experiences, which has pushed automakers to integrate stylish and customizable interior lighting, contributing to market growth.

LED technology plays a significant role in this growth due to its energy efficiency, longer lifespan, and the flexibility it offers in design. LEDs are more power-efficient and provide greater brightness compared to traditional lighting solutions. Furthermore, their compact size supports innovative interior designs, which helps automakers enhance vehicle aesthetics and functionality. OLED and LED innovations are crucial for boosting the appeal of automotive interiors, improving safety, and meeting consumer demand for premium features while lowering energy consumption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.7 billion |

| Forecast Value | $3.8 billion |

| CAGR | 8.3% |

In 2024, the LED ambient lighting systems segment held a 42% share and is expected to grow at a CAGR of 9% during 2034. The popularity of LED technology can be attributed to its low power consumption, longer lifespan, and design flexibility. LED lights are particularly advantageous as they can offer customizable color options and dynamic lighting effects, which elevate the aesthetic experience inside vehicles. This customization is a strong selling point for automakers looking to differentiate their vehicles in a competitive market. The ability to integrate these lights into mid-range vehicles has made them an appealing choice for automakers aiming to offer luxury features at a lower cost.

In 2024, the passenger car segment held a 60% share, driven by high production volumes and growing consumer demand for comfort, safety, and aesthetic features. As disposable incomes rise, consumers are increasingly seeking vehicles that offer a premium driving experience. Ambient lighting, which enhances the interior environment, has become a key feature in high-end and mass-market vehicles. Automakers are expanding the availability of these lighting systems across a range of models, including compact and mid-range cars, to appeal to younger, tech-savvy buyers. Features such as customizable colors, synchronization with entertainment systems, and door lighting enhancements are becoming standard offerings.

China Automotive Interior Ambient Lighting System Market held 48% share and generated USD 448.2 million in 2024 driven by a combination of consumer preferences for personalized in-cabin experiences, technological advancements, and supportive government policies. The demand for advanced ambient lighting systems is particularly strong in electric vehicles, where manufacturers are integrating cutting-edge lighting features to enhance the futuristic appeal of their interiors. Government incentives promoting energy-efficient technologies have encouraged the adoption of LED lighting systems, contributing to the growth of ambient lighting solutions that improve both aesthetics and driver safety.

Key players in the Automotive Interior Ambient Lighting System Market include Valeo, Stanley Electric, Innotec Group, Magneti Marelli, Koito Manufacturing, OSRAM, Lumileds Holding, Magna International, and HELLA. To strengthen their market presence, companies in the automotive interior ambient lighting system industry are focusing on product innovation, particularly in energy-efficient lighting technologies like LED and OLED. Manufacturers are expanding their portfolios to include customizable lighting solutions that enhance vehicle aesthetics and meet consumer demand for personalized in-cabin experiences. Additionally, these companies are investing in research and development to improve energy efficiency, prolong the lifespan of lighting systems, and create dynamic lighting effects that contribute to an enhanced driving experience. Strategic partnerships with automakers are also key, as these collaborations help integrate advanced lighting features into a wide range of vehicle models.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 System integrators

- 3.2.4 Technology providers

- 3.2.5 OEM

- 3.2.6 Aftermarket suppliers and distributors

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Price trends

- 3.6.1 By Product

- 3.6.2 By Region

- 3.7 Cost breakdown analysis

- 3.8 Patent analysis

- 3.9 Key news & initiatives

- 3.10 Regulatory landscape

- 3.11 Impact forces

- 3.11.1 Growth drivers

- 3.11.1.1 Rising demand for vehicle personalization

- 3.11.1.2 Technological advancements in lighting

- 3.11.1.3 Rapid growth of the automotive industry in emerging markets

- 3.11.1.4 Enhanced aesthetic appeal and comfort

- 3.11.1.5 Safety and driver assistance features

- 3.11.2 Industry pitfalls & challenges

- 3.11.2.1 High initial costs

- 3.11.2.2 Complex installation and maintenance

- 3.11.1 Growth drivers

- 3.12 Growth potential analysis

- 3.13 Porter's analysis

- 3.14 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 LED ambient lighting systems

- 5.3 OLED ambient lighting systems

- 5.4 Fiber optic ambient lighting systems

- 5.5 Laser ambient lighting systems

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger cars

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Commercial vehicles

- 6.3.1 Light commercial vehicles

- 6.3.2 Medium commercial vehicles

- 6.3.3 Heavy commercial vehicles

- 6.4 Electric vehicles (Evs)

Chapter 7 Market Estimates & Forecast, By Installation Area, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Dashboard lighting

- 7.3 Footwell lighting

- 7.4 Door panel lighting

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket installations

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 CML Innovative

- 10.2 HELLA

- 10.3 Innotec Group

- 10.4 Jiangsu Jingliang

- 10.5 Koito Electric

- 10.6 Koito Manufacturing

- 10.7 Lumenpulse

- 10.8 Lumileds Holding

- 10.9 Magna International

- 10.10 Magneti Marelli

- 10.11 Mitsubishi Electric

- 10.12 OSRAM

- 10.13 Stanley Electric

- 10.14 STANLEY Electric

- 10.15 TCL Automotive

- 10.16 Valeo

- 10.17 Varroc Lighting Systems

- 10.18 Wells Vehicle Electronics

- 10.19 Xenon Automotives

- 10.20 ZKW Group

汽车电子製造服务市场:按服务类型、车辆类型、技术和应用划分-2026-2032年全球市场预测汽车电子编程系统市场:按车辆类型、技术、工具类型、最终用途、部署模式和应用划分,全球预测,2026-2032年

汽车电子製造服务市场:按服务类型、车辆类型、技术和应用划分-2026-2032年全球市场预测汽车电子编程系统市场:按车辆类型、技术、工具类型、最终用途、部署模式和应用划分,全球预测,2026-2032年 全球汽车电子元件市场:按应用、销售管道、动力方式、车辆类型、类型、国家和地区划分-产业分析、市场规模、份额及2025年至2032年未来预测

全球汽车电子元件市场:按应用、销售管道、动力方式、车辆类型、类型、国家和地区划分-产业分析、市场规模、份额及2025年至2032年未来预测 2026-2034年全球汽车内装环境照明系统市场规模、份额、趋势及成长分析报告汽车偏光滤镜市场:按材料、偏光滤镜类型、车辆类型、应用和销售管道,全球预测,2026-2032年汽车级胎压监测晶片市场:按应用、类型、车辆类型和技术分類的全球预测(2026-2032年)车用级蓝牙晶片市场:按应用、晶片类型、整合类型、车辆类型、分销管道和范围划分 - 全球预测,2026-2032年全球汽车电子市场规模、份额、趋势和成长分析报告(2026-2034)

2026-2034年全球汽车内装环境照明系统市场规模、份额、趋势及成长分析报告汽车偏光滤镜市场:按材料、偏光滤镜类型、车辆类型、应用和销售管道,全球预测,2026-2032年汽车级胎压监测晶片市场:按应用、类型、车辆类型和技术分類的全球预测(2026-2032年)车用级蓝牙晶片市场:按应用、晶片类型、整合类型、车辆类型、分销管道和范围划分 - 全球预测,2026-2032年全球汽车电子市场规模、份额、趋势和成长分析报告(2026-2034) 汽车电子导电塑胶市场:市场机会、成长要素、产业趋势分析及2026-2035年预测

汽车电子导电塑胶市场:市场机会、成长要素、产业趋势分析及2026-2035年预测 日本汽车电子市场规模、份额、趋势和预测:按零件、车辆类型、分销管道、应用和地区划分,2026-2034年

日本汽车电子市场规模、份额、趋势和预测:按零件、车辆类型、分销管道、应用和地区划分,2026-2034年