|

市场调查报告书

商品编码

1755368

製造业碳管理系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Manufacturing Carbon Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

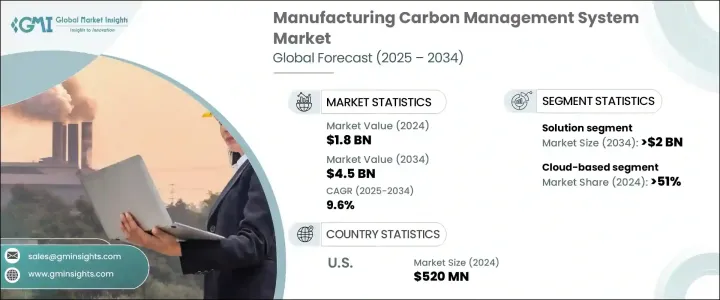

2024年,全球製造业碳管理系统市场规模达18亿美元,预计到2034年将以9.6%的复合年增长率增长,达到45亿美元,这得益于严格的环境政策的实施以及碳管理相关法规的不断加强。世界各国政府正在推出更严格的法律来控制碳排放,并纳入碳定价、碳税、限额与交易制度以及强制性温室气体 (GHG) 报告等机制,以实现气候变迁目标。为此,越来越多的企业开始采用碳管理解决方案,这促使製造商采用能够最大限度减少其环境影响的技术。

然而,对感测器、自动化工具和节能机械等进口零件征收贸易关税可能会提高碳管理系统升级的成本。虽然这可能会限制中型製造商的准入,但随着企业努力减轻进口成本上升的影响,它也可能推动国内创新,并增加对本地采购碳管理解决方案的需求。同时,人工智慧、资料分析、物联网和区块链等技术的进步正在提高碳管理解决方案的效率,使企业能够监控、管理和报告排放。这些创新正在加速各行各业对这些系统的采用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 18亿美元 |

| 预测值 | 45亿美元 |

| 复合年增长率 | 9.6% |

受日益增长的监管要求和对稳健环境报告需求的推动,碳管理系统市场的解决方案部分预计到2034年将达到20亿美元。这些解决方案提供即时排放资料,支援脱碳情境建模,并支援温室气体会计系统和环境、社会和治理 (ESG) 揭露等报告框架,这些框架对于企业维持合规并履行环境责任至关重要。随着企业努力满足更严格的永续发展法规并减少碳足迹,对这些先进工具的需求持续成长。

到2024年,基于云端的碳管理平台细分市场将占据51%的份额。这些平台能够提供灵活、可扩展的解决方案,使企业能够即时追踪和分析碳排放,这使得它们尤其具有吸引力。这些平台不仅支持追踪,还符合产业永续发展目标和环境标准,使其成为企业提高透明度、提升绩效并满足不断变化的监管要求的关键工具。

受快速的技术创新、产业变革以及对减缓气候变迁日益重视的推动,美国製造业碳管理系统市场在2024年创造了5.2亿美元的产值。环境、社会和治理 (ESG) 原则的日益普及,以及揭露碳足迹的法律压力日益加大,进一步推动了该市场的发展。随着美国企业在实现永续发展目标和监管要求方面面临越来越大的压力,碳管理解决方案市场持续成长。

全球製造业碳管理系统产业的主要参与者包括 Accuvio、Carbon Footprint Ltd.、Dakota Software、Enablon、EnergyCap、Engie、Enviance、Envirosoft、ESP、IBM、Intelex、Isometrix、Locus Technologies、NativeEnergy、Salesforce、SAP、施耐德电气和 Trinity Consants。全球製造业碳管理系统产业的公司为提升其市场影响力而采取的关键策略包括整合人工智慧、区块链和物联网等尖端技术。这有助于公司改善其资料追踪、排放报告和永续发展工作。与政府机构和行业监管机构建立策略伙伴关係对于遵守日益增长的环境政策也至关重要。透过提供可扩展的基于云端的解决方案并利用资料分析,公司正在满足对即时排放监测和透明报告日益增长的需求。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供给侧影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 供给侧影响(原料)

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率

- 战略仪表板

- 策略倡议

- 竞争基准测试

- 创新与永续发展格局

第五章:市场规模及预测:依组件划分,2021 - 2034 年

- 主要趋势

- 解决方案

- 服务

第六章:市场规模及预测:依部署,2021 - 2034 年

- 主要趋势

- 云

- 本地

第七章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 法国

- 英国

- 西班牙

- 义大利

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 拉丁美洲

- 巴西

- 阿根廷

第八章:公司简介

- Accuvio

- Carbon Footprint Ltd.

- Dakota Software

- Enablon

- EnergyCap.

- Engie

- Enviance

- Envirosoft

- ESP

- IBM

- Intelex

- Isometrix

- Locus Technlogies

- NativeEnergy

- Salesforce

- SAP

- Schneider Electric

- Trinity Consultants

The Global Manufacturing Carbon Management System Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 9.6% to reach USD 4.5 billion by 2034, attributed to the implementation of stringent environmental policies and rising regulations surrounding carbon management. Governments worldwide are introducing stricter laws to curb carbon emissions, incorporating mechanisms like carbon pricing, taxes, cap-and-trade systems, and mandatory greenhouse gas (GHG) reporting to meet climate change goals. In response, organizations are increasingly adopting carbon management solutions, driving manufacturers to embrace technologies that minimize their environmental impact.

However, trade tariffs on imported components, such as sensors, automation tools, and energy-efficient machinery, could potentially raise the cost of carbon management system upgrades. While this might restrict access for mid-sized manufacturers, it may also drive domestic innovation and increase demand for locally sourced carbon management solutions as companies strive to mitigate the impact of higher import costs. Meanwhile, advancements in technologies like AI, data analytics, IoT, and blockchain are enhancing the efficiency of carbon management solutions, allowing companies to monitor, manage, and report emissions. These innovations are accelerating the adoption of these systems across industries.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $4.5 Billion |

| CAGR | 9.6% |

The solution segment of the carbon management system market is anticipated to reach USD 2 billion by 2034, driven by increasing regulatory demands and the need for robust environmental reporting. These solutions offer real-time emissions data, enable decarbonization scenario modeling, and support reporting frameworks like the GHG Protocol and ESG disclosures, which are becoming essential for businesses to stay compliant and demonstrate environmental responsibility. As companies strive to meet stricter sustainability regulations and reduce their carbon footprint, the demand for these advanced tools continues to rise.

Cloud-based carbon management platforms segment will hold a 51% share by 2024. Their ability to offer flexible, scalable solutions that allow businesses to track and analyze carbon emissions in real time makes them particularly attractive. These platforms not only support tracking but also align with industry sustainability goals and environmental standards, making them critical tools for businesses aiming to enhance transparency, improve performance, and meet evolving regulatory requirements.

U.S. Manufacturing Carbon Management System Market generated USD 520 million in 2024, driven by rapid technological innovations, industry shifts, and the growing emphasis on climate change mitigation. This market is further fueled by the rising adoption of Environmental, Social, and Governance (ESG) principles and the increasing legal pressures to disclose carbon footprints. As companies in the U.S. face mounting pressure to meet sustainability objectives and regulatory requirements, the market for carbon management solutions continues to gain momentum.

Key players in the Global Manufacturing Carbon Management System Industry include Accuvio, Carbon Footprint Ltd., Dakota Software, Enablon, EnergyCap, Engie, Enviance, Envirosoft, ESP, IBM, Intelex, Isometrix, Locus Technologies, NativeEnergy, Salesforce, SAP, Schneider Electric, and Trinity Consultants. Key strategies adopted by companies in the Global Manufacturing Carbon Management System Industry to enhance their market presence include integrating cutting-edge technologies like AI, blockchain, and IoT. This helps companies improve their data tracking, emissions reporting, and sustainability efforts. Strategic partnerships with governmental bodies and industry regulators are also vital for compliance with growing environmental policies. By offering scalable cloud-based solutions and leveraging data analytics, firms are meeting the increasing demand for real-time emission monitoring and transparent reporting.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (Raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.1 Supply-side impact (Raw materials)

- 3.2.3 Demand-side impact (selling price)

- 3.2.3.1.1 Price transmission to end markets

- 3.2.3.1.2 Market share dynamics

- 3.2.3.1.3 Consumer response patterns

- 3.2.4 Key companies impacted

- 3.2.5 Strategic industry responses

- 3.2.5.1 Supply chain reconfiguration

- 3.2.5.2 Pricing and product strategies

- 3.2.5.3 Policy engagement

- 3.2.6 Outlook and future Considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Component, 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Solution

- 5.3 Services

Chapter 6 Market Size and Forecast, By Deployment, 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 Cloud

- 6.3 On-premises

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034, (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Accuvio

- 8.2 Carbon Footprint Ltd.

- 8.3 Dakota Software

- 8.4 Enablon

- 8.5 EnergyCap.

- 8.6 Engie

- 8.7 Enviance

- 8.8 Envirosoft

- 8.9 ESP

- 8.10 IBM

- 8.11 Intelex

- 8.12 Isometrix

- 8.13 Locus Technlogies

- 8.14 NativeEnergy

- 8.15 Salesforce

- 8.16 SAP

- 8.17 Schneider Electric

- 8.18 Trinity Consultants

全球碳计量平台市场:预测至 2032 年-按组件、部署方式、组织规模、最终用户和地区分類的分析

全球碳计量平台市场:预测至 2032 年-按组件、部署方式、组织规模、最终用户和地区分類的分析 碳计量软体市场规模、份额和趋势分析报告:按部署方式、公司规模、最终用途、地区和细分市场预测(2025-2033 年)

碳计量软体市场规模、份额和趋势分析报告:按部署方式、公司规模、最终用途、地区和细分市场预测(2025-2033 年) 二氧化碳稳压器市场按应用、输送方式、最终用户、分销管道和压力类型划分-2025-2032年全球预测

二氧化碳稳压器市场按应用、输送方式、最终用户、分销管道和压力类型划分-2025-2032年全球预测 2025年云端碳管理系统全球市场报告2025年碳计量软体全球市场报告2025年碳管理系统全球市场报告脱碳软体市场按类型、可访问性、技术、部署类型、公司规模和最终用户行业划分 - 2025-2030 年全球预测

2025年云端碳管理系统全球市场报告2025年碳计量软体全球市场报告2025年碳管理系统全球市场报告脱碳软体市场按类型、可访问性、技术、部署类型、公司规模和最终用户行业划分 - 2025-2030 年全球预测 本地碳管理系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测2025年智慧碳全球市场报告

本地碳管理系统市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测2025年智慧碳全球市场报告 全球云端碳管理系统市场

全球云端碳管理系统市场