|

市场调查报告书

商品编码

1766231

多格式包装线市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Multi-format Packaging Lines Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

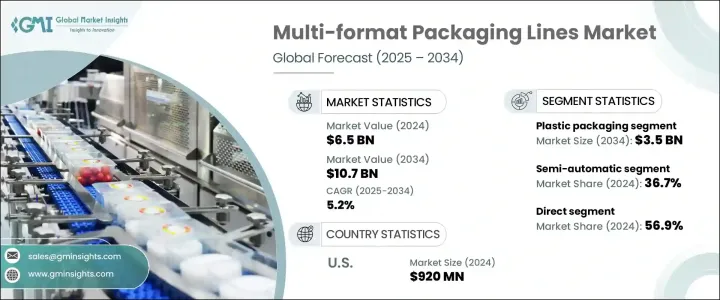

2024年,全球多规格包装生产线市场规模达65亿美元,预计到2034年将以5.2%的复合年增长率成长,达到107亿美元。这一增长源于消费者对便利性和可持续性日益增长的需求,促使食品饮料、个人护理和医药等行业广泛采用软包装。多规格包装生产线不断发展,能够适应各种包装类型、形状和材料,使製造商能够在不同规格之间切换,并最大程度地减少停机时间。这种适应性提高了营运效率,并降低了维护多台专用机器的成本。

此外,竞争激烈的零售格局促使品牌寻求能够快速回应市场需求和季节性变化的包装解决方案,这进一步凸显了对灵活包装系统的需求。这种保持相关性和即时适应性的压力促使企业优先考虑能够快速切换规格、最大限度缩短停机时间并支援多种物料处理的包装技术。随着消费趋势的快速变化——无论是节日、促销、限量版还是区域偏好——品牌都被迫调整产品的外观和规格。多规格包装生产线使製造商能够快速执行这些更改,而不会影响效率或成本控制。这种灵活性不仅增强了货架吸引力,也支持多元化的产品组合,旨在占领细分市场并在饱和的市场中最大限度地提高品牌知名度。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 65亿美元 |

| 预测值 | 107亿美元 |

| 复合年增长率 | 5.2% |

2024年,塑胶包装材料市场规模达23亿美元,占据主导地位,预计2034年将达35亿美元。塑胶包装材料的广泛应用主要归功于其适应性强、强度高、重量轻等特性,这些特性使其能够满足各种包装需求。由于塑胶材料与高速包装生产线相容,并且能够成型为各种形状和尺寸,从而适应产品展示的创新,因此将继续保持领先地位。食品饮料、药品、个人护理和家居用品等行业高度依赖塑胶包装,因为塑胶具有保质期长、防篡改和生产成本低等特征。

半自动包装线市场在2024年的市占率为36.7%,预计到2034年将以6.8%的复合年增长率成长。这些系统因其兼具手动控制和自动化效率的优势而日益受到青睐,从而创造了灵活的生产环境,而无需承担全自动化带来的高成本。它们尤其适合需要可靠、格式灵活且易于整合到现有工作流程中的设备的中小企业和合约製造商。

2024年,美国多规格包装生产线市场规模达9.2亿美元,预计2025年至2034年期间的复合年增长率将达到5.7%。美国凭藉其先进的製造设施、全自动化系统以及食品饮料、个人护理和製药等行业的显着影响力,引领北美市场。消费者对环保产品和多样化库存单位(SKU)的需求推动了智慧柔性包装技术的采用。

多格式包装生产线产业的主要参与者包括富士机械株式会社、博世包装技术公司 (Syntegon)、Coesia 集团、Haver & Boecker、IMA 集团、石田株式会社、KHS GmbH、Marchesini 集团、Multivac 集团、ProMach Inc.、Serac 集团、Sidelib 集团、SIGac集团、Sidelb 集团、Sidelb 集团、Sidelb。多格式包装生产线市场的公司正专注于多种策略来加强其影响力。这些措施包括投资研发以创造满足不断变化的消费者偏好的创新包装解决方案。公司正在与其他行业参与者建立伙伴关係和协作,以扩大产品供应并进入新市场。此外,该公司正在透过开发环保包装材料和製程来采用永续的做法,以应对日益增长的环境问题。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 机会

- 成长潜力分析

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按包装类型

- 监理框架

- 标准和认证

- 环境法规

- 进出口法规

- 贸易统计(HS 编码-8422)

- 主要进口国

- 主要出口国

- 波特五力分析

- PESTEL分析

- 消费者行为分析

- 购买模式

- 偏好分析

- 消费者行为的区域差异

- 电子商务对购买决策的影响

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按包装类型,2021 - 2034 年

- 主要趋势

- 基本的

- 次要

- 第三

第六章:市场估计与预测:依格式类型,2021 - 2034 年

- 主要趋势

- 小袋

- 瓶子

- 能

- 纸盒

- 小袋

- 管子

- 其他的

第七章:市场估计与预测:按自动化,2021 - 2034 年

- 主要趋势

- 手动的

- 半自动

- 全自动

第八章:市场估计与预测:依包装材料,2021 - 2034 年

- 主要趋势

- 塑胶

- 玻璃

- 金属

- 纸和纸板

- 其他(薄膜、箔片等)

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 食品和饮料

- 包装食品

- 乳製品

- 烘焙和糖果

- 製药

- 化妆品和个人护理

- 电子产品和消费品

- 其他(烟草、文具等)

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 直接的

- 间接

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- MEA

- 南非

- 阿联酋

- 沙乌地阿拉伯

第十二章:公司简介

- Barry-Wehmiller Companies

- Bosch Packaging Technology (Syntegon)

- Coesia Group

- Fuji Machinery Co., Ltd.

- Haver & Boecker

- IMA Group

- Ishida Co., Ltd.

- KHS GmbH

- Marchesini Group

- Multivac Group

- ProMach Inc.

- Serac Group

- Sidel Group

- SIG Combibloc Group

- Tetra Pak

The Global Multi-format Packaging Lines Market was valued at USD 6.5 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 10.7 billion by 2034. This growth is driven by the increasing consumer demand for convenience and sustainability, leading to the widespread adoption of flexible packaging across industries such as food and beverage, personal care, and pharmaceuticals. Multi-format packaging lines have evolved to accommodate various package types, shapes, and materials, allowing manufacturers to switch between different formats with minimal downtime. This adaptability enhances operational efficiency and reduces costs associated with maintaining multiple dedicated machines.

Additionally, the competitive retail landscape has led brands to seek packaging solutions that can quickly respond to market demands and seasonal changes, further emphasizing the need for flexible packaging systems. This pressure to remain relevant and adaptive in real time has driven companies to prioritize packaging technologies capable of rapid format changeovers, minimal downtime, and multi-material handling. As consumer trends evolve rapidly-whether due to holidays, promotions, limited editions, or regional preferences-brands are compelled to modify product appearance and format. Multi-format packaging lines enable manufacturers to execute these changes swiftly without compromising efficiency or cost control. This agility enhances shelf appeal but also supports diversified product portfolios aimed at capturing niche segments and maximizing brand visibility in a saturated marketplace.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.5 Billion |

| Forecast Value | $10.7 Billion |

| CAGR | 5.2% |

The plastic packaging materials segment held a dominant share of USD 2.3 billion in 2024 and is forecasted to reach USD 3.5 billion by 2034. Their widespread application is largely attributed to their adaptability, strength, and lightweight properties, which make them suitable for a broad spectrum of packaging requirements. These materials continue to lead due to their compatibility with high-speed packaging lines and ability to be molded into various shapes and sizes, accommodating innovations in product presentation. Industries such as food and beverage, pharmaceuticals, personal care, and household goods rely heavily on plastics for packaging due to their extended shelf-life protection, tamper resistance, and low production cost.

The semi-automatic packaging lines segment held a market share of 36.7% in 2024 and is projected to grow at a CAGR of 6.8% through 2034. These systems are becoming increasingly favored due to their ability to offer both manual control and automated efficiency, creating a flexible production environment without the high costs associated with full automation. They are especially suitable for SMEs and contract manufacturers who require reliable, format-adaptable equipment that can be easily integrated into existing workflows.

United States Multi-Format Packaging Lines Market was valued at USD 920 million in 2024 and is projected to grow at a CAGR of 5.7% from 2025 to 2034. The U.S. leads the North American market due to its advanced manufacturing facilities, fully automated systems, and the significant presence of industries like food and beverage, personal care, and pharmaceuticals. The adoption of smart and flexible packaging technologies is driven by consumer demand for environmentally sustainable products and a diverse range of stock-keeping units (SKUs).

Key players in the Multi-Format Packaging Lines Industry include Fuji Machinery Co., Ltd., Bosch Packaging Technology (Syntegon), Coesia Group, Haver & Boecker, IMA Group, Ishida Co., Ltd., KHS GmbH, Marchesini Group, Multivac Group, ProMach Inc., Serac Group, Sidel Group, SIG Combibloc Group, and Tetra Pak. Companies in the multi-format packaging lines market are focusing on several strategies to strengthen their presence. These include investing in research and development to create innovative packaging solutions that meet evolving consumer preferences. Partnerships and collaborations with other industry players are being pursued to expand product offerings and enter new markets. Additionally, companies are adopting sustainable practices by developing eco-friendly packaging materials and processes to align with increasing environmental concerns.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Packaging type

- 2.2.3 Format type

- 2.2.4 Automation

- 2.2.5 Packaging material

- 2.2.6 End use

- 2.2.7 Distribution channel

- 2.3 CXO perspectives: strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls & challenges

- 3.2.3 Opportunities

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By packaging type

- 3.7 Regulatory framework

- 3.7.1 Standards and certifications

- 3.7.2 Environmental regulations

- 3.7.3 Import export regulations

- 3.8 Trade statistics (HS code-8422)

- 3.8.1 Major importing countries

- 3.8.2 Major exporting countries

- 3.9 Porter's five forces analysis

- 3.10 PESTEL analysis

- 3.11 Consumer behavior analysis

- 3.11.1 Purchasing patterns

- 3.11.2 Preference analysis

- 3.11.3 Regional variations in consumer behavior

- 3.11.4 Impact of e-commerce on buying decisions

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East and Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Packaging type, 2021 - 2034 (USD Billion) (Thousand Units)

- 5.1 Key trends

- 5.2 Primary

- 5.3 Secondary

- 5.4 Tertiary

Chapter 6 Market Estimates & Forecast, By Format type, 2021 - 2034 (USD Billion) (Thousand Units)

- 6.1 Key trends

- 6.2 Pouch

- 6.3 Bottle

- 6.4 Can

- 6.5 Carton

- 6.6 Sachet

- 6.7 Tube

- 6.8 Others

Chapter 7 Market Estimates & Forecast, By Automation, 2021 - 2034 (USD Billion) (Thousand Units)

- 7.1 Key trends

- 7.2 Manual

- 7.3 Semi-automatic

- 7.4 Fully automatic

Chapter 8 Market Estimates & Forecast, By Packaging material, 2021 - 2034 (USD Billion) (Thousand Units)

- 8.1 Key trends

- 8.2 Plastic

- 8.3 Glass

- 8.4 Metal

- 8.5 Paper and paperboard

- 8.6 Others (films, foils, etc.)

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 (USD Billion) (Thousand Units)

- 9.1 Key trends

- 9.2 Food and beverages

- 9.3 Packaged food

- 9.4 Dairy products

- 9.5 Bakery and confectionery

- 9.6 Pharmaceuticals

- 9.7 Cosmetics and personal care

- 9.8 Electronics and consumer goods

- 9.9 Others (tobacco, stationery, etc.)

Chapter 10 Market Estimates & Forecast, By Distribution channel, 2021 - 2034 (USD Billion) (Thousand Units)

- 10.1 Key trends

- 10.2 Direct

- 10.3 Indirect

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 UAE

- 11.6.3 Saudi Arabia

Chapter 12 Company Profiles

- 12.1 Barry-Wehmiller Companies

- 12.2 Bosch Packaging Technology (Syntegon)

- 12.3 Coesia Group

- 12.4 Fuji Machinery Co., Ltd.

- 12.5 Haver & Boecker

- 12.6 IMA Group

- 12.7 Ishida Co., Ltd.

- 12.8 KHS GmbH

- 12.9 Marchesini Group

- 12.10 Multivac Group

- 12.11 ProMach Inc.

- 12.12 Serac Group

- 12.13 Sidel Group

- 12.14 SIG Combibloc Group

- 12.15 Tetra Pak