|

市场调查报告书

商品编码

1766232

糕点和蛋糕市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Pastry and Cakes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

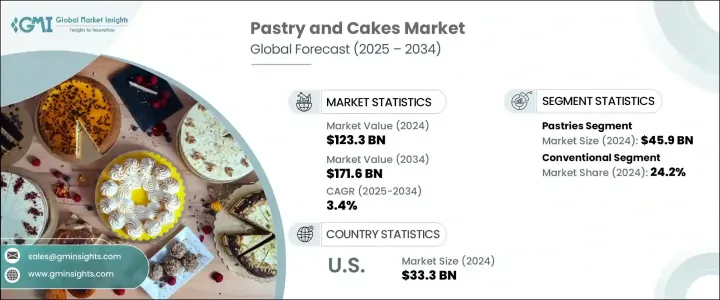

2024年,全球糕点和蛋糕市场规模达1,233亿美元,预计到2034年将以3.4%的复合年增长率成长,达到1,716亿美元。不同地区和不同收入阶层日益兴起的庆祝文化,继续在推动这一市场发展方面发挥重要作用。随着消费者越来越倾向于以奢华的食品来纪念日常时刻和特殊场合,糕点和蛋糕已成为情感消费和社交消费的首选。对日常奢侈品的渴望推动了消费重点的转变,进一步助长了这个趋势。烘焙食品已成为全球饮食习惯中不可或缺的一部分,尤其是在活动和聚会期间,它们的意义已超越了简单的营养,进入了社交表达和礼物的领域。

无论是在已开发经济体或发展中经济体,烘焙食品都持续受到广泛欢迎。便利性因素,加上生活方式的演变和城市化进程的加快,正在导致人们消费甜食的方式和时间持续变化。小巧、即食的烘焙食品越来越受欢迎,尤其是在消费者寻求能够适应快节奏生活的食品的情况下。这种转变也体现在食品零售商、超市、大型超市和专卖店业绩的提升上,它们现在提供更丰富的糕点和蛋糕产品。此外,咖啡馆、饭店和餐厅等商业部门透过提供多种形式、不同时段和不同客户群的烘焙食品,为市场收入做出了显着贡献。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1233亿美元 |

| 预测值 | 1716亿美元 |

| 复合年增长率 | 3.4% |

市场成长的很大一部分也与全球中产阶级的壮大及其对国际美食的影响息息相关。随着人们对多元化烹饪体验的认知度不断提升,对糕点和蛋糕类别多样性的需求也日益增长,无论是产品设计、食材或形式。创新趋势显而易见,人们对有机、无麸质、纯素和低糖等特定饮食类别的兴趣日益浓厚。这些产品在兼顾风味和满足感的同时,也越来越受到注重健康的消费者的青睐。推动这项需求的既有家庭消费的住宅客户,也有希望更新菜单、提供更健康、更丰富选择的商业买家。

虽然实体店在市场覆盖率和渗透率方面仍占据主导地位,但数位化格局正在成为关键的推动因素。线上零售通路在扩大覆盖不同地区消费者方面正变得越来越重要。凭藉直销模式和增强的电商能力,品牌正在释放新的人口机会,并在传统城市市场之外扩展客户群。

光是糕点细分市场,2024 年的市场价值就高达 459 亿美元,预计 2025 年至 2034 年的复合年增长率将达到 2.7%。糕点占据了整个市场的最大份额,这得益于其普遍的吸引力以及在各种消费场景(从快餐到节日小吃)中的适应性。糕点在传统零售和餐饮服务中都易于购买,这也进一步提升了其广泛的吸引力。此外,对于追求美味和便利消费的消费者来说,糕点的便携性和份量控制也是一种便捷的选择。

就配料而言,传统配料领域在2024年以298亿美元的价值领先市场,占总份额的24.2%。预计在预测期内,该领域的复合年增长率将达到3.3%。传统配料的主导地位源自于其多功能性、易于采购和消费者熟悉度。这些产品使製造商能够保持品质和口味的一致性,同时受益于规模经济。它们在已开发市场和新兴市场的广泛接受度也为他们提供了竞争优势,使其能够更深入地渗透市场并精简分销策略。

美国是全球市场的主要贡献者,其糕点和蛋糕产业在2024年的价值达到333亿美元。预计2025年至2034年期间的复合年增长率将达到3.3%。美国消费者对烘焙食品的强劲支出,加上零售烘焙店、专卖店和快餐店的蓬勃发展,使得烘焙食品的需求持续保持高位。产品创新、频繁的季节性活动以及功能性食材的加入,都是美国维持消费者兴趣的策略。数位平台和应用程式订购的便利性进一步增强了烘焙食品的可及性,尤其是在郊区和城市地区。

全球市场的竞争格局由众多专注于产品开发、品牌建立和扩大消费者覆盖范围的领导企业所塑造。竞争日益集中在针对高收入消费者的健康配方上,促使各大品牌纷纷转向以健康为导向的产品线。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 优质手工产品的需求不断增长

- 方便食品消费量增加

- 可支配所得增加和都市化

- 扩大咖啡文化和麵包连锁店

- 产业陷阱与挑战

- 健康和饮食问题

- 原物料价格波动

- 市场机会

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- Pestel 分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 蛋糕

- 千层蛋糕

- 纸杯蛋糕

- 薄饼

- 起司蛋糕

- 庆祝蛋糕

- 其他的

- 糕点

- 丹麦糕点

- 羊角麵包

- 酥皮糕点

- 闪电泡芙

- 派

- 其他的

- 甜馅饼

- 水果派

- 奶油馅饼

- 其他的

- 甜点棒和布朗尼

- 其他的

第六章:市场估计与预测:依成分,2021-2034

- 主要趋势

- 传统的

- 有机的

- 不含麸质

- 无糖/减糖

- 素食

- 其他的

第七章:市场估计与预测:按配销通路,2021-2034

- 主要趋势

- 零售麵包店

- 手工麵包店

- 连锁麵包店

- 超市和大卖场

- 便利商店

- 特色食品店

- 网路零售

- 电商平台

- 直接面向消费者的网站

- 食品服务业

- 咖啡馆和餐厅

- 饭店

- 餐饮服务

- 其他的

第八章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 住宅

- 商业的

- 咖啡馆和连锁麵包店

- 餐厅和饭店

- 餐饮服务

- 活动管理公司

- 其他的

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十章:公司简介

- AAK AB

- Archer Daniels Midland Company

- Associated British Foods plc

- Bakels Group

- BASF SE

- Cargill, Incorporated

- Corbion NV

- Dawn Food Products, Inc.

- DuPont de Nemours, Inc.

- Flowers Foods, Inc.

- General Mills, Inc.

- Grupo Bimbo, SAB de CV

- Ingredion Incorporated

- Kerry Group plc

- Koninklijke DSM NV

- Lesaffre Group

- Mondel?z International, Inc.

- Puratos Group

- DSM-Firmenich AG

- Tate & Lyle PLC

The Global Pastry and Cakes Market was valued at USD 123.3 billion in 2024 and is estimated to grow at a CAGR of 3.4% to reach USD 171.6 billion by 2034. The rising culture of celebration across regions and income brackets continues to play a significant role in driving this market. As consumers increasingly lean toward indulgent food items to commemorate daily moments and special occasions alike, pastries and cakes have become a preferred choice for both emotional and social consumption. The shift in spending priorities, driven by a desire for everyday luxuries, has fueled this trend further. With baked goods being a consistent part of global dietary habits, particularly during events and gatherings, their significance goes beyond simple nourishment and enters the territory of social expression and gifting.

In both established and developing economies, baked goods continue to witness widespread adoption. The convenience factor-combined with evolving lifestyles and increasing urbanization-is leading to consistent changes in how and when people consume sweet snacks. Compact, ready-to-eat baked items are enjoying growing popularity, especially as consumers seek out products that match their fast-paced lives. This shift is also mirrored in the rising performance of food retailers, supermarkets, hypermarkets, and specialty outlets that now feature an expanded array of pastry and cake products. Moreover, commercial sectors such as cafes, hotels, and restaurants are contributing notably to market revenues by offering these items across formats, time slots, and customer segments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $123.3 Billion |

| Forecast Value | $171.6 Billion |

| CAGR | 3.4% |

A significant portion of market growth is also tied to the growing global middle class and its exposure to international food influences. As awareness around diverse culinary experiences rises, so does the demand for variety across the pastry and cake category, whether it's in terms of product design, ingredients, or formats. A move toward innovation is visible, with increasing interest in diet-specific variants such as organic, gluten-free, vegan, and low-sugar options. These offerings are gaining favor among health-conscious consumers while still delivering on flavor and satisfaction. The demand is being fueled by both residential customers buying for home consumption and commercial buyers looking to update their menus with healthier yet indulgent choices.

While brick-and-mortar stores continue to dominate in terms of market reach and penetration, the digital landscape is emerging as a key enabler. Online retail channels are becoming increasingly crucial in expanding access to consumers across diverse geographies. With direct-to-consumer delivery models and enhanced e-commerce capabilities, brands are unlocking new demographic opportunities and increasing their customer base beyond traditional urban markets.

The pastry segment alone was valued at USD 45.9 billion in 2024 and is projected to register a CAGR of 2.7% from 2025 to 2034. This segment holds the largest share of the overall market, driven by its universal appeal and adaptability across various consumption scenarios-from quick snacks to celebratory treats. Easy availability through both traditional retail and foodservice outlets contributes to its widespread appeal. Additionally, portability and portion control make pastries a convenient choice for consumers seeking both indulgence and ease of consumption.

In terms of ingredients, the conventional segment led the market with a value of USD 29.8 billion in 2024, accounting for 24.2% of the total share. It is expected to grow at a CAGR of 3.3% over the forecast period. The dominance of conventional ingredients stems from their versatility, ease of procurement, and consumer familiarity. These products enable manufacturers to maintain consistency in quality and taste while benefiting from economies of scale. Their wide acceptance in both advanced and growing markets also provides them with a competitive edge, allowing for deeper market penetration and streamlined distribution strategies.

The United States stood out as a key contributor to the global market, with the pastry and cakes sector valued at USD 33.3 billion in 2024. It is anticipated to expand at a CAGR of 3.3% from 2025 through 2034. The country's strong consumer spending on baked goods, coupled with a robust presence of retail bakeries, specialty stores, and quick-service restaurants, keeps demand levels consistently high. Product innovation, frequent seasonal campaigns, and the inclusion of functional ingredients are strategies being used to maintain consumer interest. The convenience of digital platforms and app-based ordering has further strengthened accessibility, particularly in suburban and urban areas.

The competitive landscape of the global market is shaped by numerous leading players focused on product development, branding, and expanding their consumer reach. Competition is increasingly centered around health-forward formulations aimed at high-income consumers, leading brands to shift their offerings toward wellness-driven product lines.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1.1 Regional

- 2.2.1.2 Product type

- 2.2.1.3 Ingredient

- 2.2.1.4 Distribution channel

- 2.2.1.5 End use

- 2.3 TAM analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.5 Executive decision points

- 2.6 Critical success factors

- 2.7 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for premium and artisanal products

- 3.2.1.2 Increasing consumption of convenience foods

- 3.2.1.3 Rising disposable income and urbanization

- 3.2.1.4 Expanding cafe culture and bakery chains

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Health and dietary concerns

- 3.2.2.2 Fluctuating raw material prices

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 Pestel analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Cakes

- 5.2.1 Layer cakes

- 5.2.2 Cupcakes

- 5.2.3 Sheet cakes

- 5.2.4 Cheesecakes

- 5.2.5 Celebration cakes

- 5.2.6 Others

- 5.3 Pastries

- 5.3.1 Danish pastries

- 5.3.2 Croissants

- 5.3.3 Puff pastries

- 5.3.4 Eclairs

- 5.3.5 Tarts

- 5.3.6 Others

- 5.4 Sweet pies

- 5.4.1 Fruit pies

- 5.4.2 Cream pies

- 5.4.3 Others

- 5.5 Dessert bars and brownies

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Ingredient, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Conventional

- 6.3 Organic

- 6.4 Gluten-free

- 6.5 Sugar-free / reduced sugar

- 6.6 Vegan

- 6.7 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Retail bakeries

- 7.2.1 Artisanal bakeries

- 7.2.2 Chain bakeries

- 7.3 Supermarkets and hypermarkets

- 7.4 Convenience stores

- 7.5 Specialty food stores

- 7.6 Online retail

- 7.6.1 E-commerce platform

- 7.6.2 Direct-to-consumer websites

- 7.7 Food service sector

- 7.7.1 Cafes and restaurants

- 7.7.2 Hotels

- 7.7.3 Catering services

- 7.8 Others

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential

- 8.3 Commercial

- 8.3.1 Cafes and bakery chains

- 8.3.2 Restaurants and hotels

- 8.3.3 Catering services

- 8.3.4 Event management companies

- 8.3.5 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 AAK AB

- 10.2 Archer Daniels Midland Company

- 10.3 Associated British Foods plc

- 10.4 Bakels Group

- 10.5 BASF SE

- 10.6 Cargill, Incorporated

- 10.7 Corbion N.V.

- 10.8 Dawn Food Products, Inc.

- 10.9 DuPont de Nemours, Inc.

- 10.10 Flowers Foods, Inc.

- 10.11 General Mills, Inc.

- 10.12 Grupo Bimbo, S.A.B. de C.V.

- 10.13 Ingredion Incorporated

- 10.14 Kerry Group plc

- 10.15 Koninklijke DSM N.V.

- 10.16 Lesaffre Group

- 10.17 Mondel?z International, Inc.

- 10.18 Puratos Group

- 10.19 DSM-Firmenich AG

- 10.20 Tate & Lyle PLC