|

市场调查报告书

商品编码

1766359

自备氢气发电市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Captive Hydrogen Generation Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

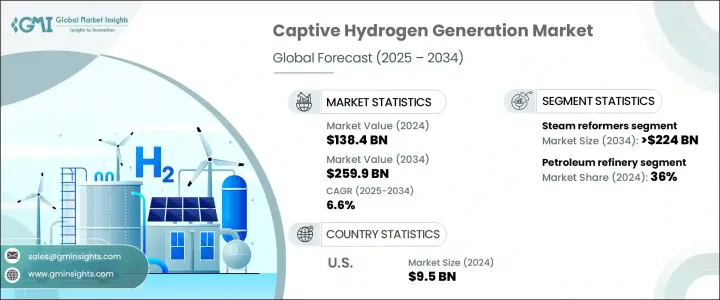

2024 年全球自备製氢市场规模达 1,384 亿美元,预计到 2034 年将以 6.6% 的复合年增长率成长,达到 2,599 亿美元。向可持续能源实践的转变和日益增长的脱碳动力,正鼓励各行各业采用现场製氢解决方案。这一趋势在炼油、化工和运输等关键产业尤为突出,这些产业对更清洁、更有效率的燃料替代品的需求日益增长。随着全球各行各业致力于减少温室气体排放,自备氢气系统的角色变得更加关键。清洁氢气生产技术的进步透过提高可扩展性、降低营运成本和提高整体系统效率,促进了这一发展势头,使现场氢气生产成为对工业用户越来越有吸引力的选择。

随着氢气需求稳定成长,尤其是在需要高纯度燃料的製程中,市场预计将受益于对紧凑型和模组化系统的大量投资。这些系统具有安装灵活性,可根据不同的生产能力进行定制,这对于寻求减少对外部氢气供应商依赖的中型工厂尤其具有吸引力。除了技术进步之外,政府的支持政策也在加速成长。税收减免、补助和碳定价机制等激励措施正在帮助工业企业透过抵消前期资本成本,向更清洁的燃料解决方案转型。自备氢气生产也在更广泛的净零排放议程中发挥战略作用,可靠的本地化燃料生产与长期能源目标一致。所有这些因素共同为全球市场的强劲成长奠定了基础。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1384亿美元 |

| 预测值 | 2599亿美元 |

| 复合年增长率 | 6.6% |

市场依製程分为蒸汽重整、电解和其他技术。其中,蒸汽重整器占据主导地位,预计到2034年将创造超过2,240亿美元的市场价值。该製程因其能够高效、大规模地将天然气等碳氢化合物原料转化为氢气而广受青睐。工业界对高产氢气的持续偏好,加上现有的蒸汽重整基础设施,继续增强了该领域的吸引力。此外,蒸汽重整器与炼油等行业现有能源系统的兼容性,进一步促进了其广泛应用,确保了整个预测期内的持续需求。

从应用角度来看,自备製氢市场细分为石油炼油厂、化学加工、金属和其他工业领域。石油炼油厂在2024年占据市场主导地位,市占率达36%,预计到2034年,其复合年增长率将超过6.3%。这一增长源于对可靠且经济高效的氢气供应的需求,以支持加氢裂解和脱硫等製程。炼油厂越来越多地采用现场氢气生产解决方案,以降低物流成本并提高能源可靠性。向内部燃料生产的过渡有助于降低供应中断带来的风险,同时符合减排目标。自备製氢为炼油厂提供了战略优势,使其能够在控製成本和合规性的同时保持生产连续性。

从地区来看,美国正成为全球市场的强大贡献者,其估值在 2022 年为 90 亿美元,2023 年为 92 亿美元,2024 年为 95 亿美元。 2024 年,北美约占全球市场份额的 9%,随着清洁能源的加速普及,预计这一比例将上升。美国市场受益于多个产业寻求降低能源成本和提高营运效率的需求成长。为此,国内企业正在开发能够按需生产氢气以满足各种最终用途的先进系统。发电机设计的创新使更紧凑、更可扩展的解决方案成为可能,鼓励在商业和工业环境中更广泛地部署。同时,对氢气生产和储存基础设施的资本投资不断增加,为该地区的长期产业成长铺平了道路。

自备製氢领域的领导企业专注于永续性、效率和适应性,以满足不断变化的行业需求。这些公司正投入资源开发创新技术,并加强其全球影响力。他们积极寻求新的商业机会,推出先进系统,拓展新兴市场,并建立合作伙伴关係,以加速清洁氢能解决方案的部署。随着现场製氢需求的预期成长,产业领导者已具备策略优势,有望从未来的市场发展中获益。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统

- 川普政府关税分析

- 对贸易的影响

- 贸易量中断

- 报復措施

- 对产业的影响

- 供应方影响(原料)

- 主要材料价格波动

- 供应链重组

- 生产成本影响

- 需求面影响(售价)

- 价格传导至终端市场

- 市占率动态

- 消费者反应模式

- 供应方影响(原料)

- 受影响的主要公司

- 策略产业反应

- 供应链重组

- 定价和产品策略

- 政策参与

- 展望与未来考虑

- 对贸易的影响

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率

- 战略仪表板

- 策略倡议

- 竞争基准测试

- 创新与永续发展格局

第五章:市场规模及预测:依工艺,2021 年至 2034 年

- 主要趋势

- 蒸气重整器

- 电解

- 其他的

第六章:市场规模及预测:依应用,2021 年至 2034 年

- 主要趋势

- 石油炼油厂

- 化学

- 金属

- 其他的

第七章:市场规模及预测:依地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 义大利

- 荷兰

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 中东和非洲

- 沙乌地阿拉伯

- 伊朗

- 阿联酋

- 南非

- 拉丁美洲

- 巴西

- 阿根廷

- 智利

第八章:公司简介

- Air Products and Chemicals

- Cummins

- Enapter

- Hitachi Zosen Corporation

- HoSt Group

- Linde

- McPhy Energy

- Messer Group

- NEL Hydrogen

- NEXT Hydrogen

- Siemens Energy

- Teledyne Energy Systems

The Global Captive Hydrogen Generation Market was valued at USD 138.4 billion in 2024 and is estimated to grow at a CAGR of 6.6% to reach USD 259.9 billion by 2034. The transition toward sustainable energy practices and the increasing push for decarbonization are encouraging industries to adopt on-site hydrogen production solutions. This trend is especially prominent across key sectors like refining, chemicals, and transportation, where the demand for cleaner, more efficient fuel alternatives is gaining traction. As global industries aim to reduce greenhouse gas emissions, the role of captive hydrogen systems has become more pivotal. Advancements in clean hydrogen production technology are contributing to this momentum by enhancing scalability, lowering operational costs, and boosting overall system efficiency, making on-site generation an increasingly attractive option for industrial users.

With demand for hydrogen steadily rising, particularly for use in processes that require high-purity fuel, the market is expected to benefit from significant investments in compact and modular systems. These systems offer installation flexibility and can be tailored to varying production capacities, which is particularly appealing for medium-sized facilities seeking to reduce reliance on external hydrogen suppliers. In addition to technological evolution, supportive government policies are amplifying growth. Incentives like tax breaks, grants, and carbon pricing mechanisms are helping industrial players transition toward cleaner fuel solutions by offsetting upfront capital costs. Captive hydrogen generation is also playing a strategic role in broader net-zero emissions agendas, where reliable and localized fuel production aligns with long-term energy goals. Collectively, these factors are laying the groundwork for robust growth across global markets.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $138.4 Billion |

| Forecast Value | $259.9 Billion |

| CAGR | 6.6% |

The market is categorized by process into steam reforming, electrolysis, and other technologies. Among these, steam reformers hold a dominant position and are anticipated to generate over USD 224 billion by 2034. This process is widely favored due to its ability to convert hydrocarbon feedstocks such as natural gas into hydrogen efficiently and at scale. The ongoing industrial preference for high-yield hydrogen generation, combined with the availability of established infrastructure for steam reforming, continues to strengthen the segment's appeal. Additionally, the compatibility of steam reformers with existing energy systems in industries like refining further contributes to its widespread adoption, ensuring sustained demand throughout the forecast period.

In terms of application, the captive hydrogen generation market is segmented into petroleum refineries, chemical processing, metals, and other industrial domains. Petroleum refineries led the market in 2024 with a 36% share and are forecast to grow at a CAGR exceeding 6.3% through 2034. This growth is driven by the need for a dependable and cost-efficient hydrogen supply to support operations like hydrocracking and desulfurization. Refineries are increasingly turning to on-site hydrogen solutions to cut logistics costs and enhance energy reliability. The transition toward in-house fuel generation helps mitigate risks associated with supply disruptions while aligning with emissions reduction targets. Captive generation offers a strategic edge for refiners aiming to maintain production continuity while managing expenses and regulatory compliance.

Regionally, the United States is emerging as a strong contributor to the global market, with valuations of USD 9 billion in 2022, USD 9.2 billion in 2023, and USD 9.5 billion in 2024. North America accounted for approximately 9% of the global market share in 2024, and this proportion is expected to increase as clean energy adoption accelerates. The U.S. market is benefiting from increased demand across multiple sectors seeking to reduce energy costs and improve operational efficiency. In response, domestic firms are developing advanced systems capable of producing hydrogen on demand for various end-use applications. Innovations in generator design are enabling more compact and scalable solutions, encouraging broader deployment in commercial and industrial settings. At the same time, growing capital investment in hydrogen production and storage infrastructure is paving the way for long-term industry growth in the region.

Leading companies in the captive hydrogen generation space are focused on sustainability, efficiency, and adaptability to meet evolving industrial requirements. These firms are dedicating resources to develop innovative technologies and strengthen their global footprint. They are actively pursuing new business opportunities by launching advanced systems, expanding into emerging regions, and forming partnerships aimed at accelerating the deployment of clean hydrogen solutions. With demand for on-site generation expected to rise, industry leaders are strategically positioned to benefit from future market developments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Trump administration tariff analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Company market share

- 4.3 Strategic dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Process, 2021 – 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Steam reformer

- 5.3 Electrolysis

- 5.4 Others

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Petroleum refinery

- 6.3 Chemical

- 6.4 Metal

- 6.5 Others

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Italy

- 7.3.3 Netherlands

- 7.3.4 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 Iran

- 7.5.3 UAE

- 7.5.4 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

- 7.6.3 Chile

Chapter 8 Company Profiles

- 8.1 Air Products and Chemicals

- 8.2 Cummins

- 8.3 Enapter

- 8.4 Hitachi Zosen Corporation

- 8.5 HoSt Group

- 8.6 Linde

- 8.7 McPhy Energy

- 8.8 Messer Group

- 8.9 NEL Hydrogen

- 8.10 NEXT Hydrogen

- 8.11 Siemens Energy

- 8.12 Teledyne Energy Systems

2026年全球沼气氢气生产市场报告

2026年全球沼气氢气生产市场报告 全球氢气生产市场规模、份额、趋势和成长分析报告(2026-2034年)

全球氢气生产市场规模、份额、趋势和成长分析报告(2026-2034年) 氢气生产市场规模、份额、趋势及预测(按技术、应用、系统类型及地区划分,2026-2034年)2026年全球氢气生产市场报告

氢气生产市场规模、份额、趋势及预测(按技术、应用、系统类型及地区划分,2026-2034年)2026年全球氢气生产市场报告 氢气生产:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

氢气生产:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 氢气生产市场规模、份额和趋势分析报告:按技术、系统、应用、地区和细分市场预测,2026-2033年

氢气生产市场规模、份额和趋势分析报告:按技术、系统、应用、地区和细分市场预测,2026-2033年 蒸气重组(SMR)市场规模、份额和成长分析(按原料、重整技术、终端用户产业、营运规模和地区划分)-2026-2033年产业预测日本氢气生产市场规模、份额、趋势及预测(按技术、系统类型、应用和地区划分,2026-2034年)

蒸气重组(SMR)市场规模、份额和成长分析(按原料、重整技术、终端用户产业、营运规模和地区划分)-2026-2033年产业预测日本氢气生产市场规模、份额、趋势及预测(按技术、系统类型、应用和地区划分,2026-2034年) 氢气生产市场规模、份额及成长分析(按技术、原料、应用及地区划分)-2026-2033年产业预测

氢气生产市场规模、份额及成长分析(按技术、原料、应用及地区划分)-2026-2033年产业预测 全球氢气生产市场-产业规模、份额、趋势、机会及预测(依来源、技术(蒸汽甲烷重整、煤气化及其他)、应用、区域及竞争格局划分,2020-2030年预测)

全球氢气生产市场-产业规模、份额、趋势、机会及预测(依来源、技术(蒸汽甲烷重整、煤气化及其他)、应用、区域及竞争格局划分,2020-2030年预测)