|

市场调查报告书

商品编码

1773221

干式烟气脱硫系统市场机会、成长动力、产业趋势分析及2025-2034年预测Dry Flue Gas Desulfurization System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

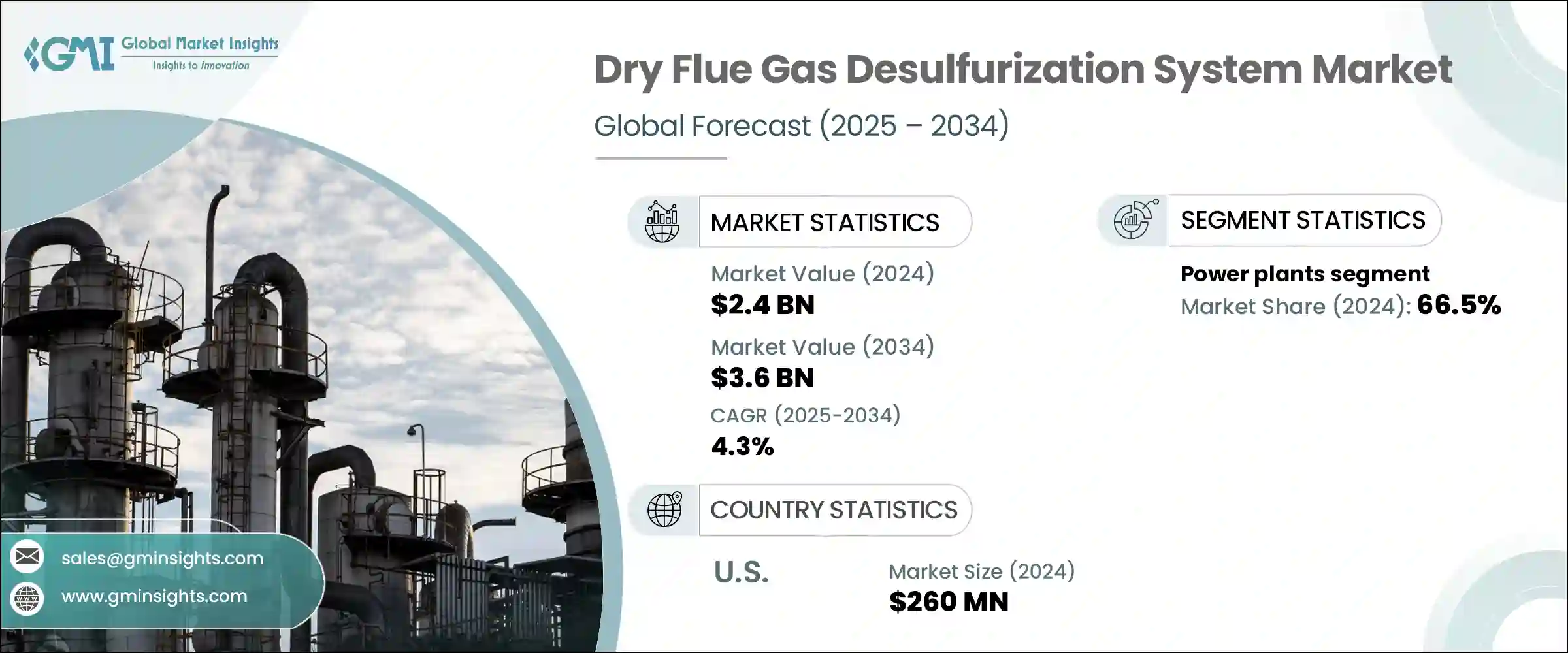

2024年,全球干式烟气脱硫系统市场规模达24亿美元,预计到2034年将以4.3%的复合年增长率成长,达到36亿美元。受日益严格的环境法规和全球清洁生产理念的推动,工业领域对高效二氧化硫(SO2)排放控制的需求不断增长,推动了市场成长。干式烟气脱硫技术具有许多优势,包括耗水量低、系统复杂性降低以及易于与现有基础设施整合。发电、化工製造、水泥生产和金属加工等行业越来越多地安装此类系统,将其作为合规和永续发展策略的一部分。

科技升级不断提升干式烟气脱硫系统的性能和可靠性,使其成为那些希望在不影响生产力的情况下降低排放的企业的首选。随着公众和监管机构对减少空气污染的压力日益增大,快速发展经济体的各行各业对这些系统的需求日益增长。由于干式烟气脱硫技术紧凑的设计和模组化功能,现有设施的改造变得更加容易。在欧洲和北美等地区,强有力的政策执行和绿色环保倡议正在推动干式烟气脱硫系统得到广泛采用,尤其是在法规合规性和环境绩效受到优先考虑的地区。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 24亿美元 |

| 预测值 | 36亿美元 |

| 复合年增长率 | 4.3% |

在应用方面,发电领域在2024年占据最大的市场份额,达到66.5%,预计到2034年将以3.6%的复合年增长率成长。这项成长主要受严格的排放法规驱动,这些法规要求对老旧的燃煤电厂进行快速且经济高效的改造。干式烟气脱硫系统仍是理想的选择,其耗水量极低、设计精简、安装时间更短。其可扩展和模组化的特性使公用事业公司能够灵活地满足排放标准,而无需在土木工程或电厂大修方面投入巨资,尤其是在全球能源转型日益深化的背景下。

2024年,美国干式烟气脱硫系统市场产值达2.6亿美元。该市场的强劲成长得益于严格的美国环保署(EPA)法规以及对减少工业过程中硫排放的重视。干式烟气脱硫技术凭藉其节水特性、易于在现有烟气管道中安装以及升级期间减少运行中断的优势,在该市场中脱颖而出。随着环境责任的加强,这些系统在帮助美国工业有效满足合规要求方面发挥着至关重要的作用。

塑造干式烟气脱硫系统市场的知名企业包括三菱重工、通用电气 Vernova、希柯环境和巴布科克威尔科克斯企业。干式烟气脱硫系统市场的公司正专注于策略性倡议,例如与能源生产商建立合作伙伴关係、提供交钥匙改造解决方案,以及扩展服务组合,包括数位监控和预测性维护工具。

透过优先考虑模组化系统设计和节水技术,企业正在满足缺水地区各行各业的实际需求。研发投入旨在提高系统效率、降低能耗并提高二氧化硫捕集率。製造商也正透过瞄准新兴市场来拓展其全球业务,这些市场正经历产业扩张和严格的空气品质法规的考验。利用自动化和智慧控制集成,这些公司能够提供更具客製化、合规性的解决方案,以满足特定行业的排放控制标准和营运限制。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 监管格局

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 成长潜力分析

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 策略仪表板

- 策略倡议

- 竞争基准测试

- 创新与技术格局

第五章:市场规模及预测:依应用,2021 - 2034

- 主要趋势

- 发电厂

- 化工和石化

- 水泥

- 金属加工和采矿

- 製造业

- 其他的

第六章:市场规模及预测:依地区,2021 - 2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿联酋

- 南非

- 拉丁美洲

- 巴西

- 智利

- 阿根廷

第七章:公司简介

- Babcock & Wilcox Enterprises

- CECO Environmental

- Duconenv

- GE Vernova

- GEA Group Aktiengesellschaft

- Hitachi Zosen Inova AG

- John Cockerill

- KC Cottrell India

- MET

- Mitsubishi Heavy Industries

- Nederman Holding AB

- Thermax Limited.

- Tri-Mer Corporation

- Valmet

- Verantis Environmental Solutions Group

The Global Dry Flue Gas Desulfurization System Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 4.3% to reach USD 3.6 billion by 2034. The market growth is fueled by increasing industrial demand for efficient sulfur dioxide (SO2 ) emission control, driven by tightening environmental regulations and the global push toward cleaner production. These dry FGD technologies provide several advantages, including low water consumption, reduced system complexity, and simplified integration into existing infrastructure. Industries such as power generation, chemical manufacturing, cement production, and metal processing are increasingly installing these systems as part of compliance and sustainability strategies.

Technological upgrades continue to improve the performance and reliability of dry FGD systems, making them a preferred choice for businesses aiming to lower emissions without compromising productivity. As public and regulatory pressure mounts to cut air pollution, industries in fast-developing economies are seeing growing demand for these systems. Retrofitting existing facilities has become easier due to the compact design and modular capabilities of dry FGD technologies. In regions like Europe and North America, strong policy enforcement and green initiatives are leading to widespread adoption, especially where regulatory compliance and environmental performance are prioritized.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $3.6 Billion |

| CAGR | 4.3% |

In terms of application, the power generation segment held the largest market share at 66.5% in 2024 and is projected to grow at a CAGR of 3.6% through 2034. This growth is primarily driven by aggressive emission mandates that require older coal-based plants to be retrofitted quickly and cost-effectively. Dry FGD systems remain an ideal fit, offering minimal water usage, streamlined design, and quicker installation timelines. Their scalable, modular nature provides utilities with the flexibility to meet emission standards without heavy investment in civil engineering or plant overhaul, especially amid a broader global energy transition.

United States Dry Flue Gas Desulfurization System Market generated USD 260 million in 2024. The market's strength is supported by rigorous EPA regulations and a strong emphasis on reducing sulfur emissions in industrial processes. Dry FGD technologies stand out in this market for their water-saving features, ease of installation in pre-existing flue gas channels, and reduced operational interruptions during upgrades. As environmental accountability intensifies, these systems are playing a vital role in helping U.S. industries meet compliance requirements with efficiency.

Prominent players shaping the Dry Flue Gas Desulfurization System Market include Mitsubishi Heavy Industries, GE Vernova, CECO Environmental, and Babcock & Wilcox Enterprises. Companies in the dry flue gas desulfurization system market are focusing on strategic initiatives such as forming partnerships with energy producers, offering turnkey retrofit solutions, and expanding service portfolios to include digital monitoring and predictive maintenance tools.

By prioritizing modular system designs and water-efficient technologies, firms are addressing the practical needs of industries operating in water-scarce regions. Investments in R&D aim to enhance system efficiency, reduce energy consumption, and improve SO2 capture rates. Manufacturers are also expanding their global footprints by targeting emerging markets with industrial expansion and strict air quality regulations. Leveraging automation and smart control integration has allowed these companies to deliver more tailored, compliance-ready solutions that align with industry-specific emission control standards and operational constraints.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis, 2024

- 4.3 Strategy dashboard

- 4.4 Strategic initiative

- 4.5 Competitive benchmarking

- 4.6 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Application, 2021 - 2034, (USD Billion)

- 5.1 Key trends

- 5.2 Power plants

- 5.3 Chemical & petrochemical

- 5.4 Cement

- 5.5 Metal processing & mining

- 5.6 Manufacturing

- 5.7 Others

Chapter 6 Market Size and Forecast, By Region, 2021 - 2034, (USD Billion)

- 6.1 Key trends

- 6.2 North America

- 6.2.1 U.S.

- 6.2.2 Canada

- 6.2.3 Mexico

- 6.3 Europe

- 6.3.1 Germany

- 6.3.2 UK

- 6.3.3 France

- 6.3.4 Spain

- 6.3.5 Italy

- 6.3.6 Netherlands

- 6.4 Asia Pacific

- 6.4.1 China

- 6.4.2 India

- 6.4.3 Japan

- 6.4.4 South Korea

- 6.4.5 Australia

- 6.5 Middle East & Africa

- 6.5.1 Saudi Arabia

- 6.5.2 UAE

- 6.5.3 South Africa

- 6.6 Latin America

- 6.6.1 Brazil

- 6.6.2 Chile

- 6.6.3 Argentina

Chapter 7 Company Profiles

- 7.1 Babcock & Wilcox Enterprises

- 7.2 CECO Environmental

- 7.3 Duconenv

- 7.4 GE Vernova

- 7.5 GEA Group Aktiengesellschaft

- 7.6 Hitachi Zosen Inova AG

- 7.7 John Cockerill

- 7.8 KC Cottrell India

- 7.9 MET

- 7.10 Mitsubishi Heavy Industries

- 7.11 Nederman Holding AB

- 7.12 Thermax Limited.

- 7.13 Tri-Mer Corporation

- 7.14 Valmet

- 7.15 Verantis Environmental Solutions Group

工业废气脱硫塔市场:依技术、材料、安装、塔型和最终用户划分,全球预测(2026-2032)

工业废气脱硫塔市场:依技术、材料、安装、塔型和最终用户划分,全球预测(2026-2032) 2026年全球湿式烟气脱硫系统市场报告2026年全球烟道气体脱硫系统市场报告

2026年全球湿式烟气脱硫系统市场报告2026年全球烟道气体脱硫系统市场报告 烟气脱硫市场 - 全球产业规模、份额、趋势、机会及预测(按类型、终端用户产业、安装量、地区和竞争格局划分,2021-2031年)

烟气脱硫市场 - 全球产业规模、份额、趋势、机会及预测(按类型、终端用户产业、安装量、地区和竞争格局划分,2021-2031年) 排烟脱硫(FGD)市场按材料类型、最终用途行业和地区划分沼气脱硫市场依技术、应用、原料、终端用户及工厂产能划分,全球预测(2026-2032年)

排烟脱硫(FGD)市场按材料类型、最终用途行业和地区划分沼气脱硫市场依技术、应用、原料、终端用户及工厂产能划分,全球预测(2026-2032年) 排烟脱硫系统市场规模、份额及成长分析(依技术、应用、吸附剂类型、安装类型及地区划分)-2026-2033年产业预测

排烟脱硫系统市场规模、份额及成长分析(依技术、应用、吸附剂类型、安装类型及地区划分)-2026-2033年产业预测 全球排烟脱硫市场-2025-2030年预测排烟脱硫系统市场:按最终用户、类型、安装类型和组件划分 - 全球预测 2025-2032

全球排烟脱硫市场-2025-2030年预测排烟脱硫系统市场:按最终用户、类型、安装类型和组件划分 - 全球预测 2025-2032 2025-2029年全球排烟脱硫系统市场

2025-2029年全球排烟脱硫系统市场