|

市场调查报告书

商品编码

1998705

酒窖市场机会、成长要素、产业趋势分析及 2026-2035 年预测。Wine Cellar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

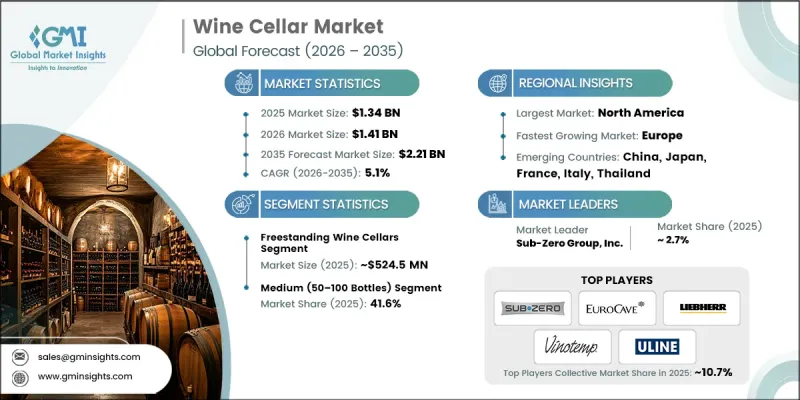

预计到 2025 年,全球葡萄酒窖市场价值将达到 13.4 亿美元,年复合成长率为 5.1%,到 2035 年将达到 22.1 亿美元。

随着葡萄酒在全球日益普及,对能够维持最佳温度、湿度和整体储存条件的专业葡萄酒储存解决方案的需求也随之增长。消费者和企业都在寻求专业的酒窖,以便长期保存优质陈年葡萄酒。饭店、餐厅和私人住宅都在增加对葡萄酒储存空间的投资,以满足商业和个人需求。电子商务和直销管道的兴起,使得优质葡萄酒的供应更加充足,也提高了人们对正确储存方法的认识。温湿度控製酒窖、节能冷却系统和模组化设计的进步,正在吸引新的买家。可支配收入的增加和葡萄酒文化的蓬勃发展,推动了住宅和豪华酒窖的普及,使得妥善储存成为葡萄酒爱好者和酒店餐饮企业都必须考虑的关键因素。

| 市场规模 | |

|---|---|

| 开始年份 | 2025 |

| 预测期 | 2026-2035 |

| 上市时的市场规模 | 13.4亿美元 |

| 预测金额 | 22.1亿美元 |

| 复合年增长率 | 5.1% |

预计2025年,独立式酒窖市场规模将达到5.245亿美元,并将以5.5%的复合年增长率成长至2035年。独立式酒窖因其多功能性和易于安装而广受欢迎,只需足够的通风和电源。它们可安装在住宅、公寓或小规模企业中,并配备可调节的层架、温湿度控制和节能冷却系统。这种适应性,加上家庭娱乐、葡萄酒收藏和精品住宿设施等日益增长的趋势,使得独立式酒窖成为全球市场成长的主要动力。

到2025年,商用葡萄酒储存系统将占据最大的市场份额。这些解决方案对于需要对大规模藏酒进行精确温控的餐厅、饭店、酒吧、酒庄和专业葡萄酒零售商至关重要。商业机构正在投资建造高容量、结构有序、具备长期储存能力的先进储酒单元,以保持葡萄酒品质并提升顾客体验。随着企业在提供优质饮品服务的同时,力求保护其珍贵藏酒,对更大、技术更先进的酒窖的需求也日益增长。

美国酒窖市场预计到2025年将达到4.653亿美元,并在2035年之前以5.1%的复合年增长率成长。市场扩张的驱动力主要来自消费者对高端葡萄酒收藏和家庭娱乐文化的日益增长的兴趣。富裕的消费者和葡萄酒爱好者正在投资模组化和客製化的解决方案,以确保最佳的温度、湿度和光照条件。住宅翻新和建筑趋势推动了对整合式酒窖、地下室和厨房酒柜的需求。专业零售商和高端住宅解决方案供应商透过提供现成和客製化选项,提高了产品的可及性。高级餐饮和酒店业也进一步推动了对商用酒柜的需求,以保护其庞大的藏酒并维持服务品质。

目录

第一章:调查方法和范围

第二章执行摘要

第三章业界考察

- 生态系分析

- 供应商情况

- 利润率

- 每个阶段增加的价值

- 影响价值链的因素

- 影响产业的因素

- 促进因素

- 全球葡萄酒消费量不断增长,人们对优质葡萄酒的鑑赏力也在提高。

- 扩大葡萄酒储存解决方案在住宅和豪华住宅的应用。

- 透过提供精心挑选的葡萄酒,拓展旅馆和餐饮业。

- 陷阱与挑战

- 定製酒窖的安装和维护成本很高

- 都市区住宅储物空间有限

- 机会

- 对模组化和紧凑型葡萄酒储藏单元的需求日益增长

- 与智慧家庭和物联网技术的集成

- 促进因素

- 成长潜力分析

- 未来市场趋势

- 科技与创新趋势

- 当前技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 副产品

- 监理情势

- 标准和合规要求

- 区域法规结构

- 认证标准

- 波特五力分析

- PESTEL 分析

- 专利趋势(基于初步调查)

- 按技术类型分類的专利申请趋势

- 领先的专利拥有者和创新领导者

- 新兴专利领域(智慧技术、冷冻技术创新)

- 贸易数据分析(基于付费资料库)

- 进出口量和进口额趋势(基于付费资料库)

- 主要贸易走廊和关税的影响(基于付费资料库)

- 主要进口国分析

- 主要出口国分析

- 分销基础设施和销售管道渗透现状(基于初步调查)

- 按地区和类型(现代零售与传统零售)分類的分销网络覆盖率(基于初步调查)

- 最后一公里基础设施差异和新分销管道的变化(基于初步研究)

第四章 竞争情势

- 介绍

- 企业市占率分析

- 按地区

- 企业矩阵分析

- 主要市场公司的竞争分析

- 竞争定位矩阵

- 主要进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 业务拓展计划

第五章 市场估算与预测:依产品类型划分,2022-2035年

- 独立式酒窖

- 内置酒窖

- 步入式酒窖

- 酒墙

- 酒柜

- 其他的

第六章 市场估计与预测:依产能划分,2022-2035年

- 小规模(少于50瓶)

- 中等规模(50-100件)

- 大号(100-200 件)

- 超大(超过200件)

第七章 市场估计与预测:依冷冻技术划分,2022-2035年

- 压缩机式冷却

- 热电冷却

- 混合冷却系统

第八章 市场估算与预测:依价格区间划分,2022-2035年

- 经济

- 大众市场

- 优质的

第九章 市场估计与预测:依应用领域划分,2022-2035年

- 住宅

- 商业的

- 餐厅和酒吧

- 饭店和度假村

- 葡萄酒商店和品酒室

- 其他的

第十章 市场估价与预测:依通路划分,2022-2035年

- B2B

- B2C

- 专卖店

- 家居建材商店

- 线上零售

- 百货公司

- 其他的

第十一章 市场估价与预测:按地区划分,2022-2035年

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲(MEA)

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

第十二章:公司简介

- Sub-Zero Group, Inc.

- EuroCave

- Liebherr Group

- Vinotemp International

- U-Line Corporation

- Haier Group

- Samsung Electronics

- LG Electronics

- Whirlpool(KitchenAid)

- Miele

- Bosch Home Appliances

- Perlick Corporation

- Smeg

- Marvel Refrigeration

- TRUE Manufacturing

The Global Wine Cellar Market was valued at USD 1.34 billion in 2025 and is estimated to grow at a CAGR of 5.1% to reach USD 2.21 billion by 2035.

The increasing popularity of wine across the globe has created a rising demand for dedicated wine storage solutions that maintain optimal temperature, humidity, and overall storage conditions. Consumers and businesses are seeking specialized cellars to preserve luxury and aged wines for long-term use. Hotels, restaurants, and private residences are increasingly investing in wine storage spaces for both commercial and personal purposes. Greater availability of premium wines through e-commerce and direct-to-consumer channels has heightened awareness of proper storage practices. Advancements in climate-controlled cellars, energy-efficient cooling systems, and modular designs are encouraging new buyers. Rising disposable incomes and the growing culture of wine appreciation are driving both residential and luxury wine cellar adoption, making proper storage a key consideration for enthusiasts and hospitality operators alike.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.34 Billion |

| Forecast Value | $2.21 Billion |

| CAGR | 5.1% |

The freestanding wine cellar segment accounted for USD 524.5 million in 2025 and is expected to grow at a CAGR of 5.5% through 2035. Freestanding units are favored for their versatility and ease of installation, requiring only proper ventilation and electricity. They can be deployed in homes, apartments, or small businesses and offer features like adjustable shelving, temperature and humidity control, and energy-efficient cooling. Their adaptability, combined with growing trends in home entertaining, wine collecting, and boutique lodging, positions freestanding wine cellars as a substantial contributor to global market growth.

The commercial wine storage systems held the largest market share in 2025. These solutions are essential for restaurants, hotels, bars, wineries, and specialty wine retailers that require precise climate management for large collections. Commercial venues invest in advanced storage units with high capacity, organized racking systems, and long-term preservation capabilities to maintain wine quality and enhance customer experiences. The demand for larger, technologically sophisticated wine cellars is rising as businesses aim to offer premium beverage services while safeguarding valuable collections.

U.S. Wine Cellar Market reached USD 465.3 million in 2025 and is expected to grow at a CAGR of 5.1% through 2035. Market expansion is supported by growing interest in premium wine collections and home entertainment culture. Affluent households and wine enthusiasts are investing in modular and custom solutions to ensure optimal temperature, humidity, and lighting conditions. Residential remodeling and construction trends are driving demand for integrated wine rooms, basements, and kitchen wine storage. Specialty retailers and luxury home solution providers contribute to product accessibility with both prebuilt and customized offerings. High-end restaurants and hospitality businesses further boost the demand for commercial wine storage units to protect extensive collections and maintain service quality.

Leading companies in the Global Wine Cellar Market include Sub-Zero Group, Inc., EuroCave, LG Electronics, Liebherr Group, Bosch Home Appliances, Samsung Electronics, Perlick Corporation, Whirlpool (KitchenAid), Haier Group, Marvel Refrigeration, Miele, TRUE Manufacturing, Smeg, Vinotemp International, and U-Line Corporation. Key players in the Global Wine Cellar Market are focusing on strategic initiatives to enhance their market presence and strengthen their competitive position. Companies are investing in R&D to develop advanced climate-controlled and energy-efficient solutions that cater to both residential and commercial needs. Collaborations with luxury home builders, hospitality businesses, and e-commerce platforms expand product reach and brand visibility. Firms offer customizable modular designs to meet varying customer requirements. Geographic expansion into emerging wine markets ensures broader penetration. Additionally, businesses emphasize after-sales services, maintenance packages, and extended warranties to improve customer satisfaction and loyalty.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Capacity

- 2.2.4 Cooling Technology

- 2.2.5 Pricing

- 2.2.6 Application

- 2.2.7 Distribution channel

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising wine consumption and appreciation of premium wines globally

- 3.2.1.2 Growing adoption of residential and luxury home wine storage solutions

- 3.2.1.3 Expansion of hospitality and restaurant sectors with curated wine offerings

- 3.2.2 Pitfalls & Challenges

- 3.2.2.1 High installation and maintenance costs for custom wine cellars

- 3.2.2.2 Limited space availability in urban residences

- 3.2.3 Opportunities

- 3.2.3.1 Rising demand for modular and compact wine storage units

- 3.2.3.2 Integration with smart home and IoT technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Future market trends

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Price trends

- 3.6.1 By region

- 3.6.2 By product

- 3.7 Regulatory landscape

- 3.7.1 Standards and compliance requirements

- 3.7.2 Regional regulatory frameworks

- 3.7.3 Certification standards

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

- 3.10 Patent Landscape (Driven by Primary Research)

- 3.10.1 Patent Filing Trends by Technology Type

- 3.10.2 Key Patent Holders & Innovation Leaders

- 3.10.3 Emerging Patent Areas (Smart Technology, Cooling Innovations)

- 3.11 Trade Data Analysis (Driven by Paid Data Base)

- 3.11.1 Import/Export Volume & Value Trends (Driven by Paid Data Base)

- 3.11.2 Key Trade Corridors & Tariff Impact (Driven by Paid Data Base)

- 3.11.3 Major Importing Countries Analysis

- 3.11.4 Major Exporting Countries Analysis

- 3.12 Distribution Infrastructure & Channel Penetration Landscape (Driven by Primary Research)

- 3.12.1 Channel Coverage by Region & Format (Modern vs Traditional Trade) (Driven by Primary Research)

- 3.12.2 Last-Mile Infrastructure Gaps & Emerging Channel Shifts (Driven by Primary Research)

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By Region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By Region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Product Type, 2022 - 2035, (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Freestanding wine cellars

- 5.3 Built-in wine cellars

- 5.4 Walk-in wine cellars

- 5.5 Wine walls

- 5.6 Wine cabinets

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Capacity, 2022 - 2035, (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Small (under 50 bottles)

- 6.3 Medium (50-100 bottles)

- 6.4 Large (100-200 bottles)

- 6.5 Extra-large (over 200 bottles)

Chapter 7 Market Estimates & Forecast, By Cooling Technology, 2022 - 2035, (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Compressor-Based Cooling

- 7.3 Thermoelectric Cooling

- 7.4 Hybrid Cooling Systems

Chapter 8 Market Estimates & Forecast, By Pricing, 2022 - 2035, (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Economy

- 8.3 Mass

- 8.4 Premium

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035, (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

- 9.3.1 Restaurants and bars

- 9.3.2 Hotels and resorts

- 9.3.3 Wine shops and tasting rooms

- 9.3.4 Others

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2022 - 2035, (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 B2B

- 10.3 B2C

- 10.3.1 Specialty stores

- 10.3.2 Home improvement stores

- 10.3.3 Online retail

- 10.3.4 Department stores

- 10.3.5 Others

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035, (USD Million) (Thousand Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 Saudi Arabia

- 11.6.2 UAE

- 11.6.3 South Africa

Chapter 12 Company Profiles

- 12.1 Sub-Zero Group, Inc.

- 12.2 EuroCave

- 12.3 Liebherr Group

- 12.4 Vinotemp International

- 12.5 U-Line Corporation

- 12.6 Haier Group

- 12.7 Samsung Electronics

- 12.8 LG Electronics

- 12.9 Whirlpool (KitchenAid)

- 12.10 Miele

- 12.11 Bosch Home Appliances

- 12.12 Perlick Corporation

- 12.13 Smeg

- 12.14 Marvel Refrigeration

- 12.15 TRUE Manufacturing