|

市场调查报告书

商品编码

1773273

兽医即时诊断市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Veterinary Point of Care Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

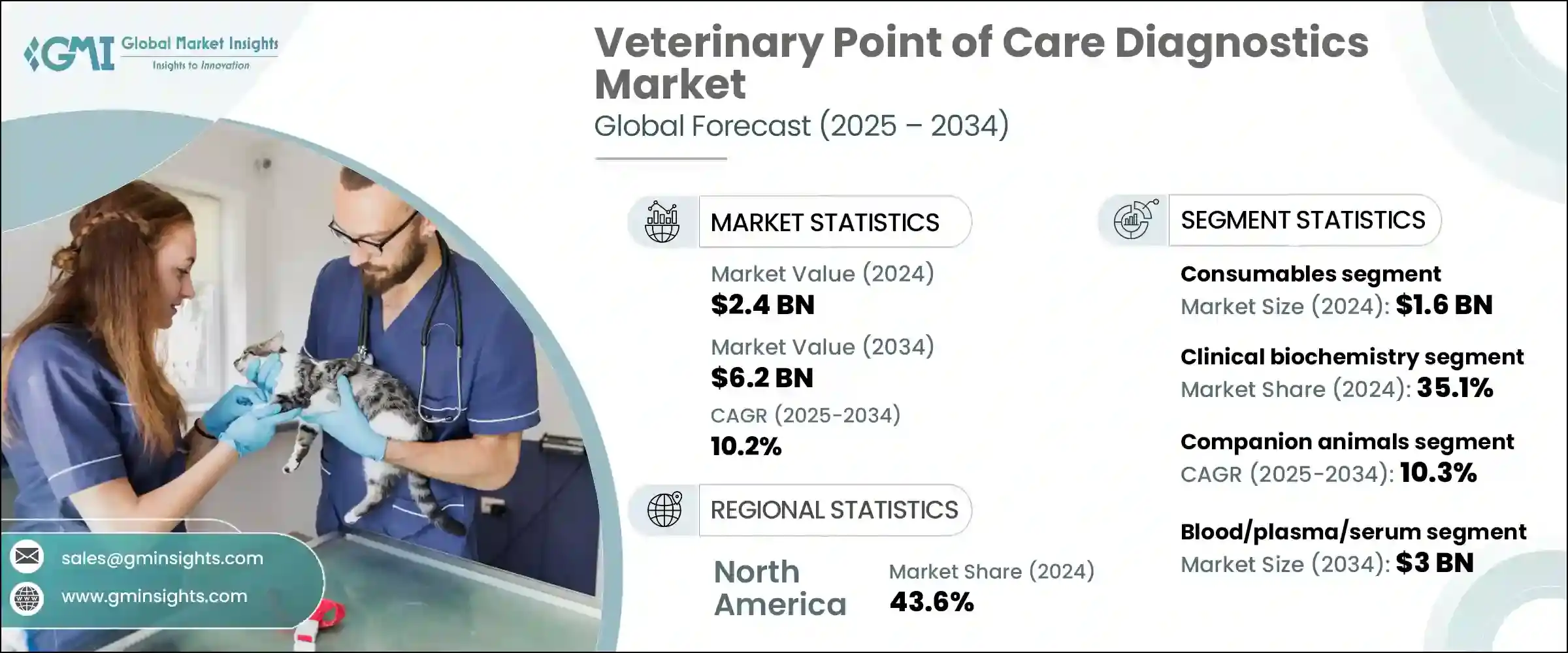

2024年,全球兽医师即时诊断市场规模达24亿美元,预计2034年将以10.2%的复合年增长率成长,达到62亿美元。这一增长反映了动物传染病发病率的上升,以及人们对跨物种人畜共通传染病日益增长的担忧。随着宠物饲养量和牲畜数量的增长,对快速现场检测的需求也日益增长。诊所和实验室正在部署先进的诊断工具,这些工具不仅能快速检测结果,而且便于携带,这在一定程度上得益于人工智慧和物联网平台,它们提高了准确性,并简化了动物健康管理。

随着兽医护理服务可及性的提升以及宠物保险覆盖率的不断上升,这些趋势增强了人们对即时诊断的信心,并加速了市场成长。随着越来越多的宠物主人重视预防性护理和早期疾病检测,他们越来越依赖即时诊断技术来更快地做出治疗决策。这种日益增长的需求促使兽医诊所和医院投资先进的便携式诊断工具,这些工具能够提供准确、即时的结果,避免外部实验室检测带来的延误。此外,这些工具的便利性和可靠性也增强了人们对优质护理的认知,使宠物主人更愿意定期进行兽医体检和健康监测,从而推动整个兽医诊断行业的持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 24亿美元 |

| 预测值 | 62亿美元 |

| 复合年增长率 | 10.2% |

2024年,兽医师即时诊断市场的耗材市场规模达16亿美元。这些耗材包括卡盒、试剂、检测试剂盒和检测试剂,是每个即时诊断程序的必需品,需要频繁补充。随着检测量的攀升,这种持续的需求支撑着可靠的经常性收入。随着诊所和医院的扩张,对便携式、易于使用的耗材的需求也随之增长,这些耗材能够立即获得结果并减少等待时间,宠物主人和专业人士对此非常欣赏。

临床生物化学领域在2024年占据35.1%的市场份额,这得益于其在评估代谢、器官功能、感染和发炎方面的核心作用。此领域的检测包括肝臟、肾臟、电解质、葡萄糖和败血症生物标记。其在兽医诊所和实验室的广泛应用凸显了其在及时诊断和治疗中的重要性,尤其是在紧急和慢性疾病中。

2024年,欧洲兽医即时诊断市场规模达6.058亿美元,未来可望维持强劲成长。在各国政府针对人畜共通传染病和牲畜疾病的措施的支持下,人们对快速动物诊断的认识不断提高,这正在加速其应用。由于微流体技术、免疫测定和便携式分子检测领域的创新,以及诊断公司和兽医组织之间的合作,欧洲市场正在快速发展。

兽医即时诊断市场的主要公司包括爱德士实验室 (IDEXX Laboratories)、通用电气医疗 (GE Healthcare)、硕腾 (Zoetis)、赛默飞世尔科技 (Thermo Fisher Scientific)、迈瑞 (Mindray)、生物梅里埃 (BioMerieux)、安泰克 (Antech)、富士雅莱索诺赛特 (SFUJ3A)、SFUJ看到欧莱索诺赛特 (EFUserJ3S)、SFUJ看到欧莱索诺赛特 (SFUJ.S. Diagnostics)、朗道实验室 (Randox Laboratories)、锐珂医疗 (Carestream Health)、百胜 (Esaote)、NeuroLogica、Biotangents、维克 (Virbac) 和伍德利设备 (Woodley Equipment)。诊断供应商正在透过产品创新、扩大合作伙伴关係和策略定价来巩固其市场地位。公司优先考虑研发,以提高检测灵敏度、便携性以及与人工智慧 (AI) 和云端平台的整合。他们与兽医诊所、动物健康网络和政府机构结盟,以扩大分销管道,并将解决方案嵌入标准护理方案中。将耗材与设备捆绑销售并提供订阅或试剂补充计划,可在确保经常性收入的同时,保持临床医生的忠诚度。区域扩张以及与当地经销商的合作,为不同市场提供客製化解决方案。此外,具有竞争力的价格、捆绑服务合约和保固计画有助于实现产品差异化。对技术卓越性和客户支援的双重重视使参与者能够在快速成长、结果驱动的行业中保持相关性并占据份额。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 对即时诊断的需求不断增加

- 增加动物保健支出

- 动物疾病发生率上升

- 诊断技术的进步

- 产业陷阱与挑战

- POC诊断设备及耗材成本高

- 熟练兽医专业人员短缺

- 市场机会

- 伴侣动物拥有量和宠物人性化程度的提高

- 兽医教育和培训中越来越多地使用即时护理

- 成长动力

- 成长潜力分析

- 监管格局

- 未来市场趋势

- 技术格局

- 当前的技术趋势

- 新兴技术

- 2024年各国兽医数量

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 年至 2034 年

- 主要趋势

- 耗材

- 仪器和设备

第六章:市场估计与预测:按测试类型,2021 年至 2034 年

- 主要趋势

- 临床生物化学

- 免疫诊断

- 分子诊断

- 血液学

- 尿液分析

- 其他测试类型

第七章:市场估计与预测:依动物类型,2021 年至 2034 年

- 主要趋势

- 伴侣动物

- 狗

- 猫

- 马匹

- 其他伴侣动物

- 牲畜

- 牛

- 猪

- 家禽

- 其他牲畜

第八章:市场估计与预测:依样本类型,2021 年至 2034 年

- 主要趋势

- 血液/血浆/血清

- 尿

- 粪便

- 其他样本类型

第九章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 传染病

- 非传染性疾病

- 遗传和先天性疾病

- 后天健康状况

- 其他应用

第 10 章:市场估计与预测:依最终用途,2021 年至 2034 年

- 主要趋势

- 兽医医院和诊所

- 诊断实验室

- 居家照护环境

- 其他最终用途

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Antech

- BioMerieux

- Biotangents

- Carestream Health

- Esaote

- Eurolyser Diagnostica

- FUJIFILM SonoSite

- GE Healthcare

- IDEXX Laboratories

- Mindray

- NeuroLogica

- Randox Laboratories

- Thermo Fisher Scientific

- Virbac

- Woodley Equipment

- Zoetis

The Global Veterinary Point of Care Diagnostics Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 6.2 billion by 2034. The surge reflects increasing rates of infectious diseases in animals and the growing concern over zoonotic illnesses crossing between species. As pet ownership and livestock populations expand, the need for rapid, on-site testing has intensified. Clinics and labs are responding by deploying advanced diagnostic tools that boast quick results and portability, thanks in part to AI and IoT-enabled platforms that enhance accuracy and streamline animal health management.

Together with better access to veterinary care and rising pet insurance adoption, these trends are fueling confidence in point-of-care testing and accelerating market growth. As more pet owners prioritize preventive care and early disease detection, they are increasingly relying on rapid diagnostics available at the point of care for faster treatment decisions. This growing demand is encouraging veterinary clinics and hospitals to invest in advanced, portable diagnostic tools that provide accurate, real-time results without the delays of external lab testing. Additionally, the convenience and reliability offered by these tools are reinforcing the perception of quality care, making pet owners more willing to engage in regular veterinary checkups and health monitoring, thereby propelling sustained growth across the entire veterinary diagnostics sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 10.2% |

The consumables segment from the veterinary point-of-care diagnostics market generated USD 1.6 billion in 2024. They include cartridges, reagents, test kits, and assays-essential for each point-of-care procedure and necessitating frequent replenishment. This continuous requirement supports reliable recurring revenue as testing volumes climb. As clinics and hospitals expand, demand for portable and easy-use consumables grows, enabling immediate results and reduced waiting times, which pet owners and professionals appreciate.

The clinical biochemistry segment held a 35.1% share in 2024, driven by its central role in evaluating metabolism, organ function, infection, and inflammation. Tests in this segment include panels for liver, kidney, electrolytes, glucose, and sepsis biomarkers. Widespread adoption in veterinary clinics and labs underscores their importance in timely diagnosis and treatment, especially critical in emergency and chronic conditions.

Europe Veterinary Point of Care Diagnostics Market reached USD 605.8 million in 2024 and is poised for strong future growth. Rising awareness around rapid animal diagnostics, backed by government initiatives targeting zoonotic and livestock diseases, is accelerating adoption. Enhanced by innovations in microfluidics, immunoassays, and portable molecular testing, along with collaborations between diagnostic firms and veterinary organizations, the European market is advancing rapidly.

Key companies in the Veterinary Point of Care Diagnostics Market include IDEXX Laboratories, GE Healthcare, Zoetis, Thermo Fisher Scientific, Mindray, BioMerieux, Antech, FUJIFILM SonoSite, Eurolyser Diagnostics, Randox Laboratories, Carestream Health, Esaote, NeuroLogica, Biotangents, Virbac, Woodley Equipment. Diagnostic providers are strengthening their market foothold through product innovation, expanding partnerships, and strategic pricing. Companies prioritize R&D to enhance test sensitivity, portability, and integration with AI and cloud platforms. They forge alliances with veterinary clinics, animal health networks, and government agencies to expand distribution and embed solutions in standard care protocols. Bundling consumables with equipment and offering subscription or reagent-replenishment programs secures recurring revenues while maintaining clinician loyalty. Regional expansions and collaborations with local distributors enable customized solutions for diverse markets. Additionally, competitive pricing, bundled service contracts, and warranty schemes help differentiate offerings. A dual emphasis on technological excellence and customer support allows players to maintain relevance and capture share in a rapidly growing, outcome-driven sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Test type

- 2.2.4 Animal type

- 2.2.5 Sample type

- 2.2.6 Application

- 2.2.7 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for point of care diagnostics

- 3.2.1.2 Increasing animal healthcare expenditures

- 3.2.1.3 Rising prevalence of animal diseases

- 3.2.1.4 Advancements in diagnostics technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of POC diagnostic devices and consumables

- 3.2.2.2 Shortage of skilled veterinary professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Rising companion animal ownership and pet humanization

- 3.2.3.2 Growing use of point of care in veterinary education and training

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Number of veterinarians, by country, 2024

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments and devices

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical biochemistry

- 6.3 Immunodiagnostics

- 6.4 Molecular diagnostics

- 6.5 Hematology

- 6.6 Urinalysis

- 6.7 Other test types

Chapter 7 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Other livestock animals

Chapter 8 Market Estimates and Forecast, By Sample Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Blood/plasma/serum

- 8.3 Urine

- 8.4 Fecal

- 8.5 Other sample types

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Infectious diseases

- 9.3 Non-infectious conditions

- 9.4 Hereditary and congenital conditions

- 9.5 Acquired health conditions

- 9.6 Other applications

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Diagnostic labs

- 10.4 Home care settings

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Antech

- 12.2 BioMerieux

- 12.3 Biotangents

- 12.4 Carestream Health

- 12.5 Esaote

- 12.6 Eurolyser Diagnostica

- 12.7 FUJIFILM SonoSite

- 12.8 GE Healthcare

- 12.9 IDEXX Laboratories

- 12.10 Mindray

- 12.11 NeuroLogica

- 12.12 Randox Laboratories

- 12.13 Thermo Fisher Scientific

- 12.14 Virbac

- 12.15 Woodley Equipment

- 12.16 Zoetis

2026年全球兽医照护现场(POC)血液学诊断市场报告2026年全球快速兽用检测市场报告2026年全球照护现场诊断市场报告

2026年全球兽医照护现场(POC)血液学诊断市场报告2026年全球快速兽用检测市场报告2026年全球照护现场诊断市场报告 兽用血液分析仪市场按产品类型、技术、吞吐量、应用和最终用户划分-全球预测(2026-2032 年)

兽用血液分析仪市场按产品类型、技术、吞吐量、应用和最终用户划分-全球预测(2026-2032 年) 兽医即时诊断市场规模、份额和成长分析(按产品类型、动物样本类型、检体、检测方法、最终用途和地区划分)—2026-2033年产业预测快速动物试验市场按产品类型、动物类型、技术、应用、最终用户和分销管道划分-2025-2032年全球预测

兽医即时诊断市场规模、份额和成长分析(按产品类型、动物样本类型、检体、检测方法、最终用途和地区划分)—2026-2033年产业预测快速动物试验市场按产品类型、动物类型、技术、应用、最终用户和分销管道划分-2025-2032年全球预测 全球快速动物检测市场全球兽医照护现场诊断市场

全球快速动物检测市场全球兽医照护现场诊断市场 兽医护理点诊断市场 - 全球产业规模、份额、趋势、机会和预测,按产品、动物类型、样本类型、适应症、检测类别、最终用户、地区和竞争情况细分,2020 年至 2030 年

兽医护理点诊断市场 - 全球产业规模、份额、趋势、机会和预测,按产品、动物类型、样本类型、适应症、检测类别、最终用户、地区和竞争情况细分,2020 年至 2030 年 美国动物照护现场诊断市场规模、份额、趋势分析报告,按产品类型、动物类型、样本类型、适应症、测试类别、最终用途、国家/地区、细分市场预测,2025 年至 2030 年

美国动物照护现场诊断市场规模、份额、趋势分析报告,按产品类型、动物类型、样本类型、适应症、测试类别、最终用途、国家/地区、细分市场预测,2025 年至 2030 年