|

市场调查报告书

商品编码

1773347

商用车电子服务工具 (EST) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Commercial Vehicle Electronic Service Tools (EST) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

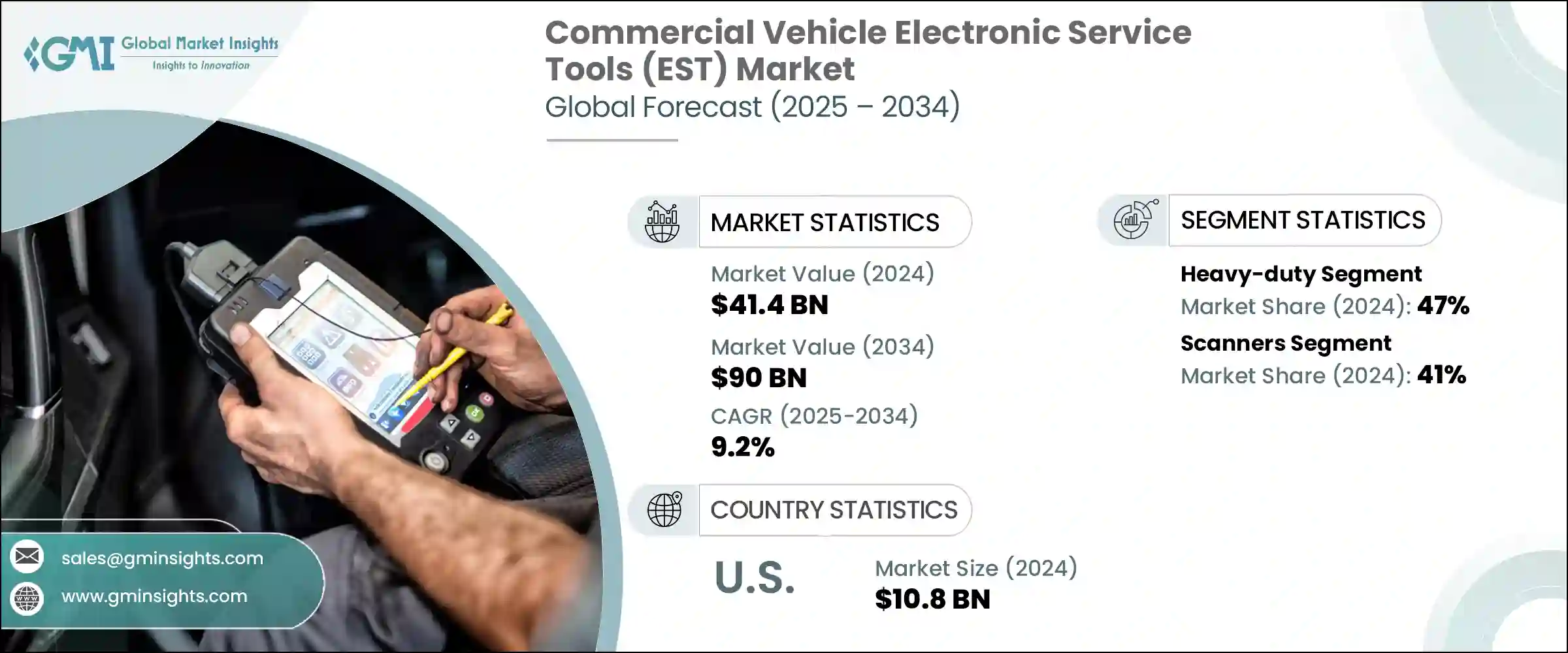

2024 年全球商用车电子服务工具市场价值为 414 亿美元,预计到 2034 年将以 9.2% 的复合年增长率成长,达到 900 亿美元。引擎控制单元 (ECU)、远端资讯处理系统和驾驶辅助技术等先进电子设备迅速融入商用车,显着增加了对高科技诊断工具的需求。随着传统机械维修逐渐不足,车队营运商和服务中心正在采用先进的电子工具进行即时诊断、软体更新和精确的故障检测。这些工具有助于减少车辆停机时间、优化车队性能并提高维护效率。随着电子商务、物流和供应链产业蓬勃发展,全球商用车数量不断增长,对定期诊断和维护的需求也日益增加。

车队管理人员越来越依赖基于电子服务工具的预测性维护解决方案,以最大限度地减少停机时间并优化资源配置。这一趋势尤其重要,因为商用车辆因长时间运行而磨损加剧,尤其是在物流、建筑和长途货运等行业。这些车辆的持续运作给零件带来了额外的压力,从而加速了频繁维护和及时诊断的需求。随着车队需求的不断增长,服务提供者和工具製造商正在寻找重大机会,引入创新解决方案,以优化维护计划并延长车辆使用寿命。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 414亿美元 |

| 预测值 | 900亿美元 |

| 复合年增长率 | 9.2% |

2024年,重型车辆市场占了47%的份额。这一增长得益于全球物流中重型车辆使用量的不断增长,即时资料和远端诊断对于确保营运效率、法规合规性和快速解决问题至关重要。随着物流业越来越依赖先进技术来改善车队管理,对专用电子服务工具的需求持续激增。这些工具有助于监控车辆的关键参数,例如油耗、引擎性能和驾驶员行为,从而改善车队运营,最大限度地减少停机时间,并保持监管标准,尤其是在跨境运输领域。

扫描器细分市场在2024年占据41%的市场份额,预计到2034年将以11.1%的复合年增长率成长。诊断扫描仪的不断发展使其在诊断复杂车辆系统方面更加灵活和高效。无线通讯功能、触控萤幕介面和即时资料流等新技术的进步,使这些工具成为维修厂和服务中心不可或缺的工具。现在,它们提供更多功能,包括ECU编程、系统测试和双向控制,从而提高了技术人员的工作效率和服务准确性,进一步推动了其普及。

美国商用车电子服务工具 (EST) 市场占有 83% 的主导地位,2024 年市场规模达 108 亿美元。美国庞大且多样化的商用车辆队伍持续推动着该产业的需求,尤其是在长途货运、配送和建筑等产业。美国完善的汽车售后市场基础设施,包括广泛的独立维修厂网路、 OEM授权服务中心和车队维护设施,为电子服务工具的成长奠定了坚实的基础。

商用车电子服务工具市场的主要参与者包括 Bendix、Bosch、Continental AG、Cummins、Daimler Trucks、Knorr-Bremse、Navistar、PACCAR、Snap-on 和 Volvo。各公司为巩固其市场地位而采取的关键策略包括持续开发可与最新汽车技术无缝整合的先进诊断工具。各公司也专注于扩大其产品范围,以满足从重型卡车到小型市政车辆等各种车型的需求。此外,他们正在与原始设备製造商 (OEM) 和车队营运商建立合作伙伴关係,以确保工具与新车型的兼容性,同时优先投资研发以增强工具功能,例如将人工智慧和机器学习融入预测性诊断。此外,许多公司正专注于扩大其全球影响力,尤其是在新兴市场,以利用不断增长的车队和物流行业。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率分析

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 商用车产量上升

- 远端资讯处理和车队管理的日益普及

- 预测性和预防性维护的需求不断增长

- 人工智慧与资料分析的整合

- 产业陷阱与挑战

- 初期投资成本高

- 网路安全风险

- 市场机会

- 符合排放法规

- 车队数位化倡议

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 按产品

- 生产统计

- 生产中心

- 消费中心

- 汇出和汇入

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:依车型,2021 - 2034 年

- 主要趋势

- 轻型

- 中型

- 重负

第六章:市场估计与预测:按工具,2021 - 2034 年

- 主要趋势

- 扫描仪

- 分析器

- 系统专用工具

- 远端资讯处理

第七章:市场估计与预测:依商业模式,2021 - 2034 年

- 主要趋势

- 购买

- 基于订阅

- 按使用付费

第八章:市场估计与预测:依连结性,2021 - 2034 年

- 主要趋势

- 蓝牙

- 无线上网

- USB

- 蜂巢

- 云

第九章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 故障检测与诊断

- 预测性和预防性维护

- 效能监控和校准

- 维修和保养服务

- 车辆追踪和远端资讯处理服务

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 在线的

- 离线

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧人

- 俄罗斯

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 南非

- 沙乌地阿拉伯

- 阿联酋

第十二章:公司简介

- Autel Intelligent Technology

- Bendix

- Bosch

- Cojali USA

- Continental AG

- Cummins

- Daimler Trucks

- Delphi Technologies

- Denso

- Knorr-Bremse

- Meritor

- Navistar

- Noregon Systems

- PACCAR

- Snap-on

- Tech Mahindra

- TEXA

- Valeo

- Volvo Group

- ZF Friedrichshafen

The Global Commercial Vehicle Electronic Service Tools Market was valued at USD 41.4 billion in 2024 and is estimated to grow at a CAGR of 9.2% to reach USD 90 billion by 2034. The rapid integration of advanced electronics into commercial vehicles, including engine control units (ECUs), telematics systems, and driver-assistance technologies, has significantly increased the demand for high-tech diagnostic tools. With traditional mechanical servicing becoming inadequate, fleet operators and service centers are adopting advanced electronic tools to provide real-time diagnostics, software updates, and precise fault detection. These tools help reduce vehicle downtime, optimize fleet performance, and enhance maintenance efficiency. As the global commercial vehicle fleet grows, driven by the boom in e-commerce, logistics, and supply chain sectors, the need for regular diagnostics and maintenance is intensifying.

Fleet managers are increasingly relying on predictive maintenance solutions, powered by electronic service tools, to minimize downtime and improve resource allocation. This trend is especially critical as commercial vehicles experience increased wear and tear from extended operational hours, particularly in industries like logistics, construction, and long-haul trucking. The continuous operation of these vehicles puts added pressure on components, accelerating the need for frequent maintenance and timely diagnostics. With the growing demands on fleets, service providers and tool manufacturers are finding significant opportunities to introduce innovative solutions that can optimize maintenance schedules and enhance vehicle longevity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $41.4 Billion |

| Forecast Value | $90 Billion |

| CAGR | 9.2% |

In 2024, the heavy-duty vehicle segment held a 47% share. This growth is driven by the increasing use of heavy-duty vehicles in global logistics, where real-time data and remote diagnostics are vital for ensuring operational efficiency, regulatory compliance, and quick problem resolution. As the logistics industry becomes more reliant on advanced technologies to improve fleet management, the demand for specialized electronic service tools continues to surge. These tools help monitor key vehicle parameters, such as fuel consumption, engine performance, and driver behavior, thus enhancing fleet operations, minimizing downtime, and maintaining regulatory standards, especially in cross-border transportation.

The scanners segment held a 41% share in 2024 and is expected to grow at a CAGR of 11.1% through 2034. The continuous evolution of diagnostic scanners has made them more versatile and efficient in diagnosing complex vehicle systems. New advancements, such as wireless communication capabilities, touchscreen interfaces, and live data streaming, have made these tools indispensable in workshops and service centers. They now offer more functionalities, including ECU programming, system tests, and bi-directional controls, which enhance technician productivity and service accuracy, further driving their adoption.

United States Commercial Vehicle Electronic Service Tools (EST) Market held a dominant 83% share and generated USD 10.8 billion in 2024. The vast and varied commercial vehicle fleet in the U.S. serves as a constant driver for demand in this sector, particularly in industries like long-haul trucking, delivery, and construction. The country's well-established automotive aftermarket infrastructure, including a wide network of independent workshops, OEM-authorized service centers, and fleet maintenance facilities, provides a solid foundation for the growth of electronic service tools.

Key players in the Commercial Vehicle Electronic Service Tools Market include Bendix, Bosch, Continental AG, Cummins, Daimler Trucks, Knorr-Bremse, Navistar, PACCAR, Snap-on, and Volvo. Key strategies that companies are adopting to strengthen their position in the market include the continuous development of advanced diagnostic tools that integrate seamlessly with the latest vehicle technologies. Companies are also focusing on expanding their product offerings to cater to a wide range of vehicle types, from heavy-duty trucks to smaller municipal vehicles. Additionally, partnerships with OEMs and fleet operators are being pursued to ensure tool compatibility with new vehicle models, while investment in research and development is a priority to enhance tool capabilities, such as incorporating artificial intelligence and machine learning for predictive diagnostics. Furthermore, many companies are focusing on expanding their global presence, particularly in emerging markets, to capitalize on the growing fleet and logistics sectors.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Tool

- 2.2.4 Business Model

- 2.2.5 Connectivity

- 2.2.6 Application

- 2.2.7 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising commercial vehicle production

- 3.2.1.2 Growing adoption of telematics & fleet management

- 3.2.1.3 Rising demand for predictive and preventive maintenance

- 3.2.1.4 Integration of AI & data analytics

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High initial investment cost

- 3.2.2.2 Cybersecurity risk

- 3.2.3 Market opportunities

- 3.2.3.1 Emission regulation compliance

- 3.2.3.2 Fleet digitalization initiatives

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Light duty

- 5.3 Medium-duty

- 5.4 Heavy-duty

Chapter 6 Market Estimates & Forecast, By Tool, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Scanners

- 6.3 Analyzers

- 6.4 System-specific tools

- 6.5 Telematics

Chapter 7 Market Estimates & Forecast, By Business Model, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Purchase

- 7.3 Subscription-based

- 7.4 Pay-per-use

Chapter 8 Market Estimates & Forecast, By Connectivity, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Bluetooth

- 8.3 Wi-Fi

- 8.4 USB

- 8.5 Cellular

- 8.6 Cloud

Chapter 9 Market Estimates & Forecast, By Application, 2021- 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 Fault detection & diagnostics

- 9.3 Predictive & preventive maintenance

- 9.4 Performance monitoring & calibration

- 9.5 Repair & maintenance services

- 9.6 Vehicle tracking & telematics service

Chapter 10 Market Estimates & Forecast, By Distribution Channel, 2021- 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 Online

- 10.3 Offline

Chapter 11 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Nordics

- 11.3.7 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.4.6 Southeast Asia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Autel Intelligent Technology

- 12.2 Bendix

- 12.3 Bosch

- 12.4 Cojali USA

- 12.5 Continental AG

- 12.6 Cummins

- 12.7 Daimler Trucks

- 12.8 Delphi Technologies

- 12.9 Denso

- 12.10 Knorr-Bremse

- 12.11 Meritor

- 12.12 Navistar

- 12.13 Noregon Systems

- 12.14 PACCAR

- 12.15 Snap-on

- 12.16 Tech Mahindra

- 12.17 TEXA

- 12.18 Valeo

- 12.19 Volvo Group

- 12.20 ZF Friedrichshafen

2026年全球汽车钣金零件市场报告

2026年全球汽车钣金零件市场报告 商用车凸轮轴市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、製造技术、燃料类型、地区和竞争格局划分,2021-2031年)汽车锻造市场 - 全球产业规模、份额、趋势、机会及预测(按材料类型、零件、车辆类型、地区和竞争格局划分,2021-2031年)

商用车凸轮轴市场 - 全球产业规模、份额、趋势、机会及预测(按车辆类型、製造技术、燃料类型、地区和竞争格局划分,2021-2031年)汽车锻造市场 - 全球产业规模、份额、趋势、机会及预测(按材料类型、零件、车辆类型、地区和竞争格局划分,2021-2031年) 全球汽车贵金属催化剂市场(按催化剂类型、贵金属类型、燃料类型、排放标准阶段、车辆类型和分销渠道划分)预测(2026-2032年)汽车底盘钣金市场(按零件、车辆类型、材质、製造流程、销售管道和最终用户划分)—2026-2032年全球预测汽车素车钢材市场依材质、产品类型、製造流程、车辆类型及应用划分-2026年至2032年全球预测汽车车身结构性黏着剂树脂类型、应用、车辆类型、动力系统和结构划分),全球预测,2026-2032年轻量化车身黏合剂市场(按聚合物类型、组件系统、车辆类型、基材和应用划分)-全球预测,2026-2032年乘用车零件锻造市场-全球产业规模、份额、趋势、机会及预测,依材料类型、零件类型、车辆类型、地区及竞争格局划分,2021-2031年预测商用车零件锻造市场 - 全球产业规模、份额、趋势、机会和预测,按材料类型、零件类型、车辆类型、地区和竞争格局划分(2021-2031 年预测)

全球汽车贵金属催化剂市场(按催化剂类型、贵金属类型、燃料类型、排放标准阶段、车辆类型和分销渠道划分)预测(2026-2032年)汽车底盘钣金市场(按零件、车辆类型、材质、製造流程、销售管道和最终用户划分)—2026-2032年全球预测汽车素车钢材市场依材质、产品类型、製造流程、车辆类型及应用划分-2026年至2032年全球预测汽车车身结构性黏着剂树脂类型、应用、车辆类型、动力系统和结构划分),全球预测,2026-2032年轻量化车身黏合剂市场(按聚合物类型、组件系统、车辆类型、基材和应用划分)-全球预测,2026-2032年乘用车零件锻造市场-全球产业规模、份额、趋势、机会及预测,依材料类型、零件类型、车辆类型、地区及竞争格局划分,2021-2031年预测商用车零件锻造市场 - 全球产业规模、份额、趋势、机会和预测,按材料类型、零件类型、车辆类型、地区和竞争格局划分(2021-2031 年预测)