|

市场调查报告书

商品编码

1773394

再生沥青路面 (RAP) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Recycled Asphalt Pavement (RAP) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

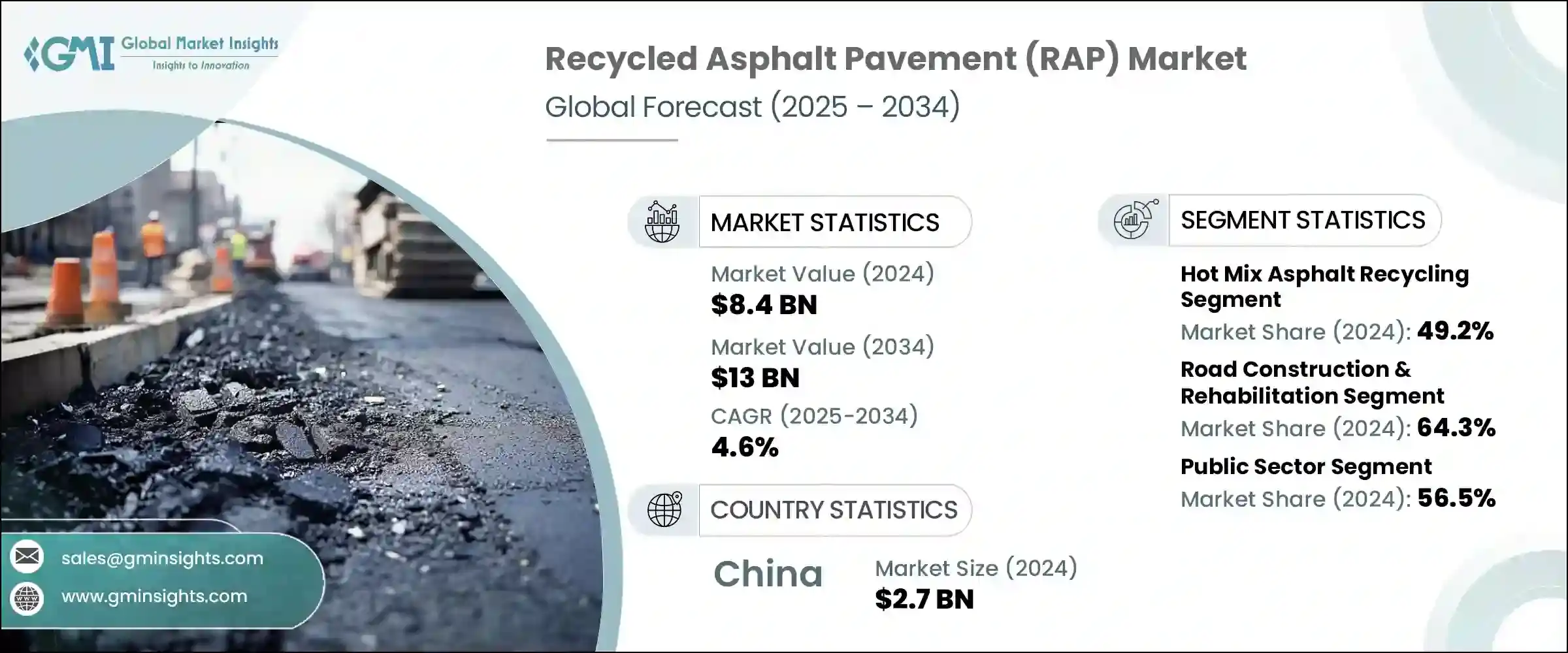

2024年,全球再生沥青路面市场规模达84亿美元,预计2034年将以4.6%的复合年增长率成长,达到130亿美元。随着对经济高效、永续建筑材料的需求不断增长,再生沥青路面产业在各个基础设施领域都获得了显着的关注。各国政府和承包商越来越多地采用沥青回收,以减少对原生料的依赖,降低专案成本,并最大限度地减少对环境的影响。这一趋势的驱动力在于,人们越来越重视透过重复使用现有道路材料来减少垃圾掩埋、提高能源效率和限制温室气体排放。监管机构持续强调透过永续道路建设实践来保护环境,这进一步巩固了再生沥青路面在全球基础设施领域的地位。

在追求更永续的道路修復解决方案方面,再生沥青 (RAP) 展现出显着的经济和生态优势。再生沥青可以融入铺路工程中,且性能丝毫不受影响,是传统沥青的耐用替代品。它与现有的间歇式和滚筒式混合技术相容,使其成为大规模道路建设的实用选择。近年来,人们越来越重视减少基础设施专案生命週期排放,这也促进了再生沥青 (RAP) 的普及。透过将再生材料纳入施工流程,承包商能够在保持结构完整性的同时降低碳足迹。此外,RAP 的操作弹性(例如可使用行动回收设备在现场加工)也提高了其效率并使其广泛应用。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 84亿美元 |

| 预测值 | 130亿美元 |

| 复合年增长率 | 4.6% |

在各种回收方法中,热拌沥青混合料 (HMA) 回收已成为主流,2024 年占据了整体市场份额的 49.2%。 HMA 回收因其能够提供接近原始性能的性能,同时显着降低材料成本和碳排放而脱颖而出。它对高 RAP 含量混合料的适应性使其成为高速公路重铺和道路升级的首选方法。此外,技术进步提高了 HMA 回收製程的一致性和质量,使其能够应用于结构要求严格的路面层。

在应用方面,道路建设和修復占据市场主导地位,占2024年总需求的64.3%。永续城市发展和经济高效的道路升级需求日益增长,导致该领域再生沥青(RAP)的使用量激增。如今,再生材料被广泛应用于主干道和地方道路,帮助市政当局和私人承包商在优化资源利用的同时实现环境目标。再生沥青(RAP)能够利用高比例的再生材料来维持路面性能,使其成为公共和私人基础设施项目的关键组成部分。随着越来越多的司法管辖区寻求与长期永续发展目标保持一致,将其融入道路工程变得更具战略意义。

按最终用户细分,公共部门在2024年占据再生材料市场的最大份额,达56.5%。政府支持的基础设施计划和永续发展要求已使再生材料成为公共工程的标准组成部分。国家和地区层面的主管部门越来越多地要求在招标规范中使用再生材料,尤其是在高速公路和市政重建项目中。公共机构也优先考虑那些符合环境认证和长期性能的材料,从而增强了再生材料在采购策略中的价值。

从区域来看,中国引领全球再生沥青 (RAP) 市场,2024 年估值达 27 亿美元。中国高度重视基础设施互联互通、都市更新和环境责任,推动了各省大规模采用再生沥青。支持再生建筑材料的政策框架,加上现代化再生工厂的蓬勃发展,持续支撑再生沥青在各类专案中的应用。中国在国家公路建设中采用结构化方法,将再生沥青融入其中,这显着提升了该地区的市场份额。

随着大型基础设施公司不断提升其永续发展能力,再生沥青路面产业的竞争格局正在改变。市场领导者正在将沥青回收纳入核心运营,并专注于垂直整合,以确保整个供应链的品质控制。从拥有骨材生产单位到营运沥青混合料厂和提供摊舖服务,这些公司已经建立了精简的流程,以有效地回收和再利用再生沥青。

许多企业正在透过建立专用设施、升级滚筒搅拌机以及利用行动设备进行高再生沥青应用来扩大其回收能力。技术整合也变得越来越重要,企业部署数位化工具以实现再生沥青的精准计量、温度调节和排放监测,以支援符合低碳建筑标准。此外,产业参与者正在与公共机构合作进行研究和试点项目,旨在提高再生沥青使用的规范并优化全深度回收技术。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 道路维修和基础设施修復的需求不断增长

- 与原生沥青相比,材料和生产成本更低

- 严格的环境法规促进再生材料

- 产业陷阱与挑战

- 专用回收设备和工厂改造的初始投资成本

- 再生沥青材料的品质和性能不一致

- 市场机会

- 扩大政府资助的可持续基础设施项目,鼓励 RAP 整合

- 道路建设中越来越多地采用就地冷填和全深度再生技术

- 开发性能增强添加剂以提高高 RAP 混合料的质量

- 私营部门对商业项目绿建筑材料的兴趣日益浓厚

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按回收流程,2021 - 2034 年

- 主要趋势

- 热拌沥青回收

- 批次厂

- 鼓厂

- 冷拌沥青再生利用

- 就地冷再生

- 中央工厂冷回收

- 就地回收

- 就地冷再生(CIR)

- 全深度填海(FDR)

- 就地热回收 (HIR)

- 中央工厂回收

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 道路建设与修復

- 高速公路和快速公路

- 城市道路和街道

- 乡村道路

- 停车场和人行道

- 机场跑道和滑行道

- 人行道、自行车道和休閒场地

- 其他基础设施(港口、工业场地)

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 公部门

- 交通运输部(DOT)

- 市政当局和地方政府

- 机场和港口当局

- 私部门

- 建筑和工程公司

- 房地产开发商

- 工业和商业最终用途

- 承包商和分包商

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第九章:公司简介

- Colas SA

- Eurovia (VINCI Group)

- Granite Construction Inc.

- Oldcastle Materials (CRH)

- LafargeHolcim Ltd.

- CEMEX SAB de CV

- Vulcan Materials Company

- Road Science

- The Lane Construction Corporation

- GreenRap

- Downer Group (Reconophalt)

- Gencor Industries

- Phoenix Industries

- Atmos Technologies

The Global Recycled Asphalt Pavement Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 4.6% to reach USD 13 billion by 2034. As demand for cost-effective and sustainable construction materials increases, the RAP industry is gaining significant traction across various infrastructure segments. Governments and contractors are increasingly embracing asphalt recycling to reduce dependence on virgin raw materials, lower project costs, and minimize environmental impact. The trend is driven by a growing focus on reducing landfill waste, improving energy efficiency, and limiting greenhouse gas emissions through the reuse of existing road materials. Regulatory bodies continue to emphasize environmental preservation through sustainable road construction practices, which has further solidified RAP's position in the global infrastructure sector.

In the pursuit of more sustainable road rehabilitation solutions, RAP presents considerable economic and ecological advantages. Recycled asphalt can be integrated into paving projects without compromising performance, offering a durable alternative to conventional asphalt. Its compatibility with existing batch and drum mix technologies makes it a practical choice for large-scale road construction. In recent years, the increased focus on reducing lifecycle emissions from infrastructure projects has also contributed to RAP's rising popularity. By incorporating reclaimed materials into construction workflows, contractors are able to lower their carbon footprints while maintaining high structural integrity. Moreover, the operational flexibility of RAP, such as its ability to be processed on-site using mobile recycling equipment, adds to its efficiency and widespread adoption.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $13 Billion |

| CAGR | 4.6% |

Among recycling methods, hot mix asphalt (HMA) recycling has emerged as the leading process, accounting for 49.2% of the overall market share in 2024. HMA recycling stands out due to its ability to deliver near-virgin performance while significantly cutting down on both material costs and carbon emissions. Its adaptability to high-RAP-content mixes has made it the preferred method for highway resurfacing and road upgrades. Additionally, advances in technology have improved the consistency and quality of HMA recycling processes, making it feasible for use in structurally demanding road layers.

In terms of application, road construction and rehabilitation dominated the market, representing 64.3% of total demand in 2024. The increasing need for sustainable urban development and cost-effective roadway upgrades has led to a surge in RAP usage within this segment. Recycled materials are now widely incorporated into arterial and local roads, helping municipalities and private contractors meet environmental goals while optimizing resource use. The ability to maintain pavement performance using high percentages of recycled content has made RAP a key component in public and private infrastructure projects. Its integration into roadworks has become more strategic as more jurisdictions seek to align with long-term sustainability targets.

When segmented by end user, the public sector held the largest share of the RAP market in 2024, accounting for 56.5%. Government-backed infrastructure initiatives and sustainability mandates have made RAP a standard component in public works. Authorities at national and regional levels increasingly require the use of recycled materials in tender specifications, particularly for highways and municipal redevelopment projects. Public agencies are also prioritizing materials that contribute to environmental certifications and long-term performance, thereby reinforcing the value of RAP in procurement strategies.

Regionally, China led the global RAP market, with a valuation of USD 2.7 billion in 2024. The country's strong emphasis on infrastructure connectivity, urban renewal, and environmental responsibility has driven large-scale adoption of recycled asphalt across its provinces. Policy frameworks supporting recycled construction materials, coupled with the growth of modern recycling plants, continue to support RAP deployment in various projects. China's structured approach to integrating RAP in national highway development has contributed significantly to the region's dominant market share.

The competitive landscape of the recycled asphalt pavement industry is evolving as major infrastructure companies enhance their sustainability credentials. Market leaders are incorporating asphalt recycling into core operations, focusing on vertical integration to ensure quality control across the supply chain. From owning aggregate production units to operating asphalt mix plants and paving services, these companies have established streamlined processes to recover and reuse reclaimed asphalt efficiently.

Many are expanding their recycling capacity by setting up dedicated facilities, upgrading drum mixers, and utilizing mobile units for high-RAP applications. Technological integration is also becoming more prominent, with firms deploying digital tools for precise RAP dosing, temperature regulation, and emissions monitoring to support compliance with low-carbon construction standards. In addition, industry participants are collaborating with public agencies on research and pilot projects aimed at enhancing specifications for recycled asphalt use and optimizing full-depth recycling techniques.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Recycling Process

- 2.2.3 Application

- 2.2.4 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing demand for road repair and infrastructure rehabilitation

- 3.2.1.2 Lower material and production costs compared to virgin asphalt

- 3.2.1.3 Stringent environmental regulations promoting recycled materials

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Initial investment costs for specialized recycling equipment and plant modifications

- 3.2.2.2 Inconsistent quality and performance of reclaimed asphalt material

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of government-funded sustainable infrastructure programs encouraging RAP integration

- 3.2.3.2 Rising adoption of cold-in-place and full-depth reclamation techniques in road construction

- 3.2.3.3 Development of performance-enhancing additives to improve high RAP mix quality

- 3.2.3.4 Increasing private sector interest in green construction materials for commercial projects

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation Landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation Landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates and Forecast, By Recycling Process, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Hot mix asphalt recycling

- 5.2.1 Batch plant

- 5.2.2 Drum plant

- 5.3 Cold mix asphalt recycling

- 5.3.1 In-place cold recycling

- 5.3.2 Central plant cold recycling

- 5.4 In-place recycling

- 5.4.1 Cold in-place recycling (CIR)

- 5.4.2 Full depth reclamation (FDR)

- 5.4.3 Hot in-place recycling (HIR)

- 5.5 Central plant recycling

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction & rehabilitation

- 6.2.1 Highways and expressways

- 6.2.2 Urban roads and streets

- 6.2.3 Rural roads

- 6.3 Parking lots and pavements

- 6.4 Airport runways and taxiways

- 6.5 Pathways, bike lanes, and recreational surfaces

- 6.6 Other infrastructure (ports, industrial sites)

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Public sector

- 7.2.1 Departments of transportation (DOTs)

- 7.2.2 Municipalities and local governments

- 7.2.3 Airports and ports authorities

- 7.3 Private sector

- 7.3.1 Construction and engineering firms

- 7.3.2 Real estate developers

- 7.3.3 Industrial and commercial end use

- 7.4 Contractors and subcontractors

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 Colas S.A.

- 9.2 Eurovia (VINCI Group)

- 9.3 Granite Construction Inc.

- 9.4 Oldcastle Materials (CRH)

- 9.5 LafargeHolcim Ltd.

- 9.6 CEMEX S.A.B. de C.V.

- 9.7 Vulcan Materials Company

- 9.8 Road Science

- 9.9 The Lane Construction Corporation

- 9.10 GreenRap

- 9.11 Downer Group (Reconophalt)

- 9.12 Gencor Industries

- 9.13 Phoenix Industries

- 9.14 Atmos Technologies

沥青改质剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

沥青改质剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 沥青市场报告:按产品、沥青类型、应用、最终用途产业和地区划分,2026-2034年

沥青市场报告:按产品、沥青类型、应用、最终用途产业和地区划分,2026-2034年 2026年全球沥青、润滑油和润滑脂市场报告

2026年全球沥青、润滑油和润滑脂市场报告 温拌沥青添加剂市场按类型、技术、应用和最终用户划分 - 全球预测 2026-2032

温拌沥青添加剂市场按类型、技术、应用和最终用户划分 - 全球预测 2026-2032 沥青脱模剂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

沥青脱模剂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) 沥青经销商 - 全球市场份额和排名、总收入和需求预测(2025-2031 年)北美沥青路面地工织物市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2025-2033 年)2025年全球再生沥青市场报告

沥青经销商 - 全球市场份额和排名、总收入和需求预测(2025-2031 年)北美沥青路面地工织物市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2025-2033 年)2025年全球再生沥青市场报告 冷拌沥青市场机会、成长动力、产业趋势分析及2025-2034年预测

冷拌沥青市场机会、成长动力、产业趋势分析及2025-2034年预测 2025-2029年全球沥青市场

2025-2029年全球沥青市场