|

市场调查报告书

商品编码

1773412

冷拌沥青市场机会、成长动力、产业趋势分析及2025-2034年预测Cold Mix Asphalt Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

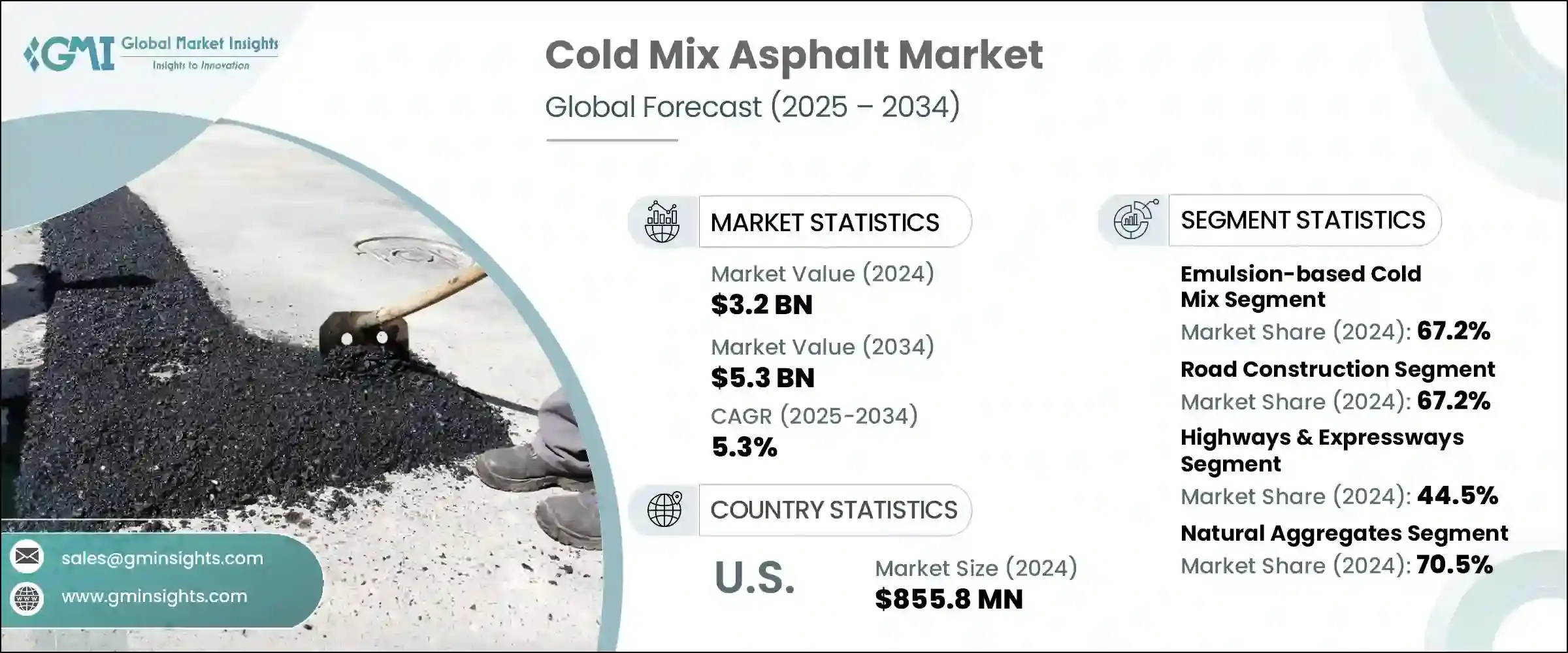

2024 年全球冷拌沥青混合料市场价值为 32 亿美元,预计到 2034 年将以 5.3% 的复合年增长率成长至 53 亿美元。这项成长动力来自全球持续的基础设施投资、对低排放建筑材料日益增长的需求以及对道路维护和修復项目日益增长的关注。冷拌沥青混合料由于使用方便、设备要求低、几乎可以在任何天气条件下施工,作为传统热拌沥青混合料的替代品,其受欢迎程度正稳步提升。发展中和已开发地区的政府都在推动道路连通和养护计划,尤其是在热拌沥青混合料厂有限或根本不存在的地区。因此,冷拌沥青混合料替代品正成为农村道路建设和现场维修项目中不可或缺的一部分。

这种沥青类型也有助于降低温室气体排放,在有利于永续基础设施建设的监管环境下,它成为一个相当吸引力的选择。它广泛应用于临时维修、公共设施断路恢復以及低流量道路的维护,使其成为成本敏感且物流挑战较大的场合中不可或缺的材料。此外,国家政策支援和配方技术进步提高了其可靠性、保质期以及对现代铺路标准的遵循。冷拌沥青不仅降低了人工和能源成本,还延长了储存时间,使其成为分散施工和紧急维修的首选解决方案。这种便利性,加上其高效的性能,确保了冷拌沥青继续受到公共工程部门和私人承包商的青睐。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 32亿美元 |

| 预测值 | 53亿美元 |

| 复合年增长率 | 5.3% |

在产品细分方面,2024年,乳液基冷拌混合料占据市场主导地位,占总收入份额的67.2%。这种优势源自于其生产过程中更低的能耗和更安全的施工操作,这与全球安全和永续发展目标高度契合。乳液基混合料因其与各种骨材的兼容性以及适用于路面修补和一般维护而广泛应用。配方日益普及也得益于其在潮湿环境下也能施工的特性,这进一步增强了其在各种气候和环境下的实用性。

2024年,道路建设领域是最大的应用领域,市占率达67.2%。尤其是在半城市化和农村地区,道路建设项目越来越重视高效、经济的解决方案,这持续推动了冷拌沥青的需求。这种材料具有运输便利、无需现场加热等物流优势,是建造通道、小路和低流量交通走廊的理想选择。它能够快速部署,资源消耗极少,也使其成为基础设施扩建工程中初期表面处理和铺路的首选材料。

从终端产业角度来看,2024年,高速公路和快速公路占了44.5%的市场。随着国家和区域公路投资的不断增加,对速凝和耐候材料的需求日益增长,这些材料能够承受频繁的车辆荷载,同时最大限度地减少交通中断。冷拌沥青混合料能够很好地满足这项需求,尤其是在需要持续维修、路肩加固和路面稳定的地方。其快速部署能力可确保最大限度地减少停机时间,这对于繁忙路线和高流量高速公路至关重要。

2024年,美国引领全球冷拌沥青混合料市场,市场估价达8.558亿美元。联邦政府专注于基础设施现代化的资金投入,以及向环保材料的广泛转变,在支撑市场成长方面发挥了关键作用。各州和市政机构在道路维护工作中越来越多地采用冷拌沥青混合料,这主要得益于其多功能性,以及在极端天气波动地区的紧急维修、季节性修补和长期路面处理方面的适用性。

塑造竞争格局的关键参与者包括 All States Materials Group、Martin Marietta Materials、Lakeside Industries、UNIQUE Paving Materials 和嘉吉。这些公司利用区域专业知识和先进的研发能力,提供满足不同地区需求的高效能产品。他们高度重视可靠性、耐用性和生态效率,并不断改进产品,以满足永续道路建设不断变化的需求。受消费者日益青睐、符合现代基础设施优先事项的即用型、全天候路面解决方案的推动,那些强调聚合物改性冷补解决方案和以客户为中心的支援系统的品牌也在扩大其业务范围。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 基础建设不断推进

- 成本效益和能源效率

- 环境永续性重点

- 易于应用和储存

- 产业陷阱与挑战

- 品质一致性问题

- 发展中地区的认知有限

- 来自热拌沥青的竞争

- 标准化挑战

- 市场机会

- 新兴市场基础建设成长

- 技术进步

- 永续建筑趋势

- 偏远地区应用

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利格局

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按类型,2021 - 2034 年

- 主要趋势

- 乳化冷混料

- 阳离子乳液冷混料

- 阴离子乳液冷混剂

- 非离子乳液冷混料

- 稀释沥青

- 快速固化(RC)削减

- 中等固化(mc)削减

- 慢速固化(SC)削减

- 泡沫沥青

- 冷再生混合料

- 现场冷回收

- 中央工厂冷回收

- 其他类型

- 聚合物改质冷拌混合料

- 纤维增强冷混料

- 添加剂增强冷混合料

第六章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 道路建设

- 新道路建设

- 道路拓宽

- 临时道路

- 道路维护和维修

- 修补坑洞

- 裂缝密封

- 表面处理

- 紧急维修

- 路面修復

- 全面深度復垦

- 就地冷再生

- 基层稳定

- 其他应用

- 肩部结构

- 公用事业削减恢復

- 自行车道和人行道

第七章:市场估计与预测:按最终用途产业,2021 - 2034 年

- 主要趋势

- 高速公路和快速公路

- 州际公路

- 州际公路

- 高速公路

- 市政道路

- 城市道路

- 郊区道路

- 乡村道路

- 机场

- 跑道

- 滑行道

- 围裙

- 停车区

- 商业停车场

- 住宅停车场

- 工业停车场

- 其他的

- 港口和海港

- 工业区

- 休閒区

第八章:市场估计与预测:依总体类型,2021 - 2034 年

- 主要趋势

- 天然骨材

- 碎石

- 碎石

- 沙

- 再生骨材

- 再生沥青路面(RAP)

- 再生混凝土骨材(RCA)

- 其他再生材料

- 合成骨材

第九章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- ExxonMobil Corporation

- BASF

- Total Energies SE

- All States Materials Group.

- Martin Marietta Materials

- Asphalt Materials

- UNIQUE Paving Materials

- Arkema Group

- Kao Corporation

- Ingevity Corporation

- Colas SA

- Aggregate Industries

- Cargill

- HEI-Way Premium Asphalt

- Simon Team

- Heidelberg Materials AG

- Reeves Construction Company

- Tarmac (CRH Company)

- Lakeside Industries

The Global Cold Mix Asphalt Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 5.3 billion by 2034. This growth is being driven by ongoing infrastructure investments, a rising demand for low-emission construction materials, and increasing attention toward road maintenance and rehabilitation projects worldwide. Cold mix asphalt is steadily gaining traction as an alternative to traditional hot mix due to its ease of use, minimal equipment requirements, and ability to be applied in virtually any weather condition. Governments across developing and developed regions are pushing for road connectivity and preservation programs, especially in areas where access to hot mix plants is limited or non-existent. As a result, the cold mix alternative is becoming integral to rural road development and spot repair projects.

This asphalt type also contributes to lower greenhouse gas emissions, making it an attractive option in a regulatory landscape that favors sustainable infrastructure practices. Its use in temporary repairs, utility cut reinstatements, and maintenance of low-traffic roads has made it indispensable in cost-sensitive and logistically challenged scenarios. Furthermore, national policy support and technological advancements in formulation have enhanced its reliability, shelf life, and adherence to modern paving standards. Cold mix asphalt not only reduces labor and energy costs but also enables longer storage, making it a go-to solution for decentralized construction and emergency repairs. This convenience, coupled with its performance efficiency, ensures that cold mix continues to gain preference among public works departments and private contractors alike.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.3 Billion |

| CAGR | 5.3% |

In terms of product segmentation, emulsion-based cold mix dominated the market in 2024, accounting for 67.2% of the total revenue share. This dominance stems from its lower energy consumption during production and safer handling during application, which aligns well with global safety and sustainability goals. Emulsion-based mixes are widely used due to their compatibility with various aggregates and suitability for patchwork and general road surface maintenance. The rising adoption of this formulation is also supported by its ability to be applied in damp conditions, further enhancing its practicality in a range of climates and environments.

The road construction segment represented the largest application area in 2024, holding a market share of 67.2%. The increasing emphasis on efficient, cost-effective solutions for road development projects, particularly in semi-urban and rural regions, continues to boost demand for cold mix asphalt. This material offers logistical advantages, such as easier transport and no need for onsite heating, making it ideal for building access roads, byways, and low-volume traffic corridors. Its capacity to be deployed quickly with minimal resources has also made it a preferred material for initial surface treatments and paving in infrastructure expansion projects.

From an end-use industry perspective, highways and expressways contributed to 44.5% of the market share in 2024. As investments in national and regional roadways intensify, there is a growing need for quick-setting and weather-resistant materials that can withstand frequent vehicle loads while minimizing traffic disruptions. Cold mix asphalt fulfills this requirement well, particularly in areas where continuous repairs, shoulder reinforcement, and surface stabilization are needed. Its rapid deployability ensures minimal downtime, which is critical for busy routes and high-traffic expressways.

The United States led the global cold mix asphalt market in 2024, with a valuation of USD 855.8 million. Federal funding focused on infrastructure modernization, along with a broader shift toward environmentally conscious materials, has played a pivotal role in supporting market growth. The adoption of cold mix in road preservation efforts across state and municipal agencies is increasing, particularly due to its versatility and suitability for emergency repairs, seasonal patching, and long-term surface treatments in areas with extreme weather fluctuations.

Key players shaping the competitive landscape include All States Materials Group, Martin Marietta Materials, Lakeside Industries, UNIQUE Paving Materials, and Cargill. These companies leverage regional expertise and advanced R&D capabilities to offer high-performance products tailored to diverse geographic needs. With a strong focus on reliability, durability, and eco-efficiency, they continue to refine their offerings to support the evolving demands of sustainable road construction. Brands that emphasize polymer-modified cold patch solutions and customer-centric support systems are also expanding their footprint, driven by increasing consumer preference for ready-to-use, all-season pavement solutions that align with modern infrastructure priorities.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Application

- 2.2.4 End use industry

- 2.2.5 Manufacturing process

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing infrastructure development

- 3.2.1.2 Cost-effectiveness & energy efficiency

- 3.2.1.3 Environmental sustainability focus

- 3.2.1.4 Ease of application & storage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Quality consistency issues

- 3.2.2.2 Limited awareness in developing regions

- 3.2.2.3 Competition from hot mix asphalt

- 3.2.2.4 Standardization challenges

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging markets infrastructure growth

- 3.2.3.2 Technological advancements

- 3.2.3.3 Sustainable construction trends

- 3.2.3.4 Remote area applications

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Emulsion-based cold mix

- 5.2.1 Cationic emulsion cold mix

- 5.2.2 Anionic emulsion cold mix

- 5.2.3 Non-ionic emulsion cold mix

- 5.3 Cutback asphalt

- 5.3.1 Rapid curing (RC) cutback

- 5.3.2 Medium curing (mc) cutback

- 5.3.3 Slow curing (SC) cutback

- 5.4 Foamed asphalt

- 5.5 Cold recycled mix

- 5.5.1 Place cold recycling

- 5.5.2 Central plant cold recycling

- 5.6 Other types

- 5.6.1 Polymer modified cold mix

- 5.6.2 Fiber reinforced cold mix

- 5.6.3 Additive enhanced cold mix

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Road construction

- 6.2.1 New road construction

- 6.2.2 Road widening

- 6.2.3 Temporary roads

- 6.3 Road maintenance & repair

- 6.3.1 Pothole patching

- 6.3.2 Crack sealing

- 6.3.3 Surface treatment

- 6.3.4 Emergency repairs

- 6.4 Pavement rehabilitation

- 6.4.1 Full depth reclamation

- 6.4.2 Cold in-place recycling

- 6.4.3 Base course stabilization

- 6.5 Other applications

- 6.5.1 Shoulder construction

- 6.5.2 Utility cuts restoration

- 6.5.3 Bike paths & walkways

Chapter 7 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Highways & expressways

- 7.2.1 Interstate highways

- 7.2.2 State highways

- 7.2.3 Expressways

- 7.3 Municipal roads

- 7.3.1 Urban roads

- 7.3.2 Suburban roads

- 7.3.3 Rural roads

- 7.4 Airports

- 7.4.1 Runways

- 7.4.2 Taxiways

- 7.4.3 Aprons

- 7.5 Parking areas

- 7.5.1 Commercial parking lots

- 7.5.2 Residential parking

- 7.5.3 Industrial parking

- 7.6 Others

- 7.6.1 Ports & harbors

- 7.6.2 Industrial areas

- 7.6.3 Recreational areas

Chapter 8 Market Estimates and Forecast, By Aggregate Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Natural aggregates

- 8.2.1 Crushed stone

- 8.2.2 Gravel

- 8.2.3 Sand

- 8.3 Recycled aggregates

- 8.3.1 Reclaimed asphalt pavement (RAP)

- 8.3.2 Recycled concrete aggregate (RCA)

- 8.3.3 Other recycled materials

- 8.4 Synthetic aggregates

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 ExxonMobil Corporation

- 10.2 BASF

- 10.3 Total Energies SE

- 10.4 All States Materials Group.

- 10.5 Martin Marietta Materials

- 10.6 Asphalt Materials

- 10.7 UNIQUE Paving Materials

- 10.8 Arkema Group

- 10.9 Kao Corporation

- 10.10 Ingevity Corporation

- 10.11 Colas SA

- 10.12 Aggregate Industries

- 10.13 Cargill

- 10.14 HEI-Way Premium Asphalt

- 10.15 Simon Team

- 10.16 Heidelberg Materials AG

- 10.17 Reeves Construction Company

- 10.18 Tarmac (CRH Company)

- 10.19 Lakeside Industries

沥青改质剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

沥青改质剂:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 沥青市场报告:按产品、沥青类型、应用、最终用途产业和地区划分,2026-2034年

沥青市场报告:按产品、沥青类型、应用、最终用途产业和地区划分,2026-2034年 2026年全球沥青、润滑油和润滑脂市场报告

2026年全球沥青、润滑油和润滑脂市场报告 温拌沥青添加剂市场按类型、技术、应用和最终用户划分 - 全球预测 2026-2032

温拌沥青添加剂市场按类型、技术、应用和最终用户划分 - 全球预测 2026-2032 沥青脱模剂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年)

沥青脱模剂市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场预测(2025-2033 年) 沥青经销商 - 全球市场份额和排名、总收入和需求预测(2025-2031 年)北美沥青路面地工织物市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2025-2033 年)2025年全球再生沥青市场报告

沥青经销商 - 全球市场份额和排名、总收入和需求预测(2025-2031 年)北美沥青路面地工织物市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2025-2033 年)2025年全球再生沥青市场报告 再生沥青路面 (RAP) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

再生沥青路面 (RAP) 市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测 2025-2029年全球沥青市场

2025-2029年全球沥青市场