|

市场调查报告书

商品编码

1773398

消化性溃疡治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Peptic Ulcers Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

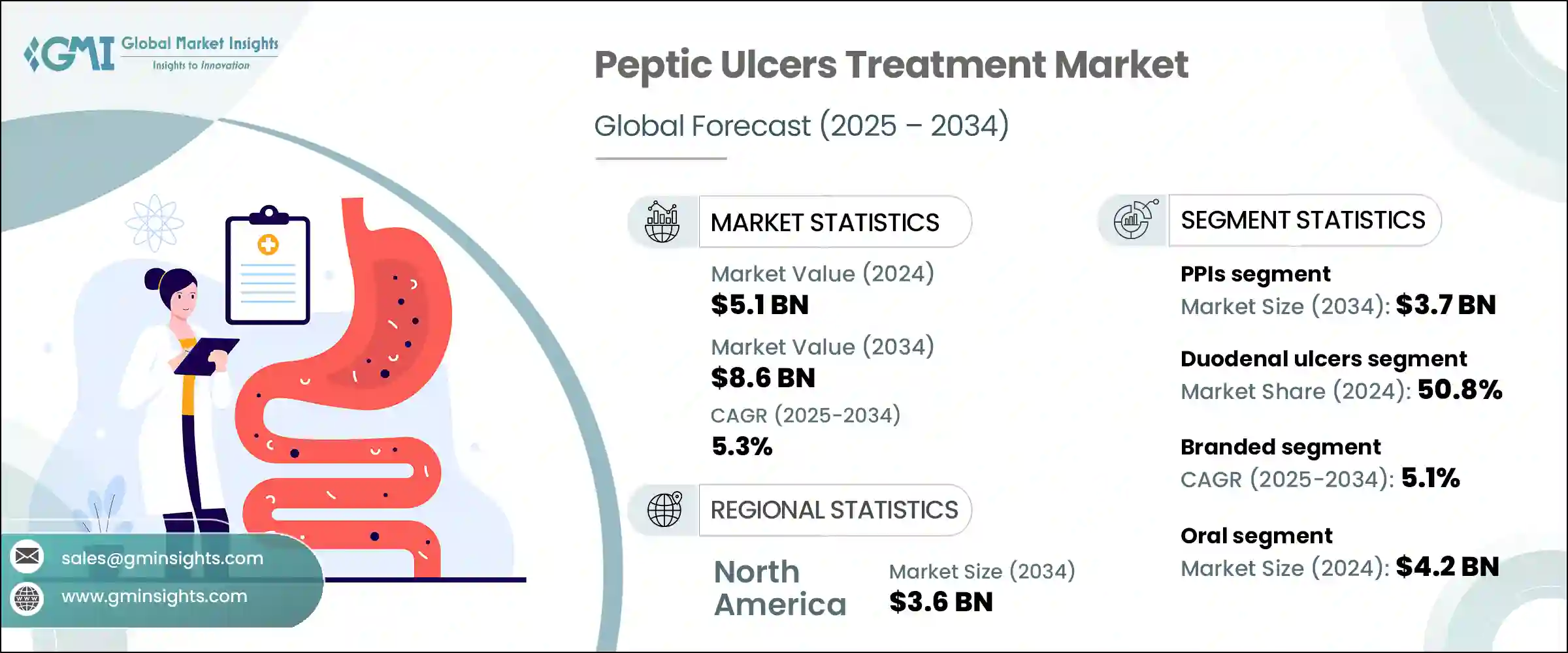

2024年,全球消化性溃疡治疗市场规模达51亿美元,预计2034年将以5.3%的复合年增长率成长至86亿美元。市场成长主要源自于成人胃肠道疾病发病率的上升以及创新药物解决方案的持续发展。幽门螺旋桿菌感染的广泛流行是推动这一需求成长的关键因素,该感染仍然是全球消化性溃疡的主要原因。全球卫生机构指出,幽门螺旋桿菌感染影响全球一半以上的人口,尤其是在中低收入地区。这种令人担忧的感染率预计将加速对更有效的治疗方案的需求,以控制和根除疾病。

推动市场扩张的另一个因素是非类固醇类抗发炎药物滥用的日益严重,这类药物往往会损害胃黏膜并导致溃疡形成。此外,诊断技术的进步以及创新治疗方案(包括二联疗法和三联疗法)的日益普及,正在提高患者的康復率并最大限度地降低溃疡復发率。这些因素,加上已开发国家和新兴国家对消化性溃疡的认知度不断提高以及医疗保健可近性的不断提升,预计将在未来几年维持对消化性溃疡治疗方案的稳定需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 51亿美元 |

| 预测值 | 86亿美元 |

| 复合年增长率 | 5.3% |

质子帮浦抑制剂 (PPI) 市场在 2024 年的销售额为 23 亿美元,预计到 2034 年将达到 37 亿美元,复合年增长率为 5.1%。 PPI 因其在降低胃酸水平、加速癒合和缓解疼痛方面的有效性,已成为溃疡治疗的基石。其可靠的疗效和极低的副作用使其成为治疗方案的广泛首选。 PPI 对根除幽门螺旋桿菌的多药疗法的贡献进一步巩固了其市场主导地位。临床上一直报告较高的治癒成功率,尤其是在 4 至 8 週的治疗窗口期内使用 PPI 的情况下。

十二指肠溃疡在2024年占据50.8%的市场份额,预计在整个预测期内将经历显着增长。这类溃疡通常发生在小肠上部,主要由细菌感染和长期使用非类固醇抗发炎药(NSAID)引发。这类溃疡在广泛人群中普遍存在,且常伴随独特的症状,便于更快诊断和更及时的干预,从而提高治疗率。

北美消化性溃疡治疗市场在2024年达到21亿美元,预计2034年将达到36亿美元,复合年增长率为5.5%。该地区的主导地位可归因于非类固醇抗发炎药物相关併发症和幽门螺旋桿菌感染的高负担。完善的医疗保健体系、更便捷的先进药物取得途径以及日益提升的胃肠道护理和预防保健意识,都有助于该地区保持强劲的市场地位。此外,领先製药公司的积极布局也将继续支撑该地区的成长。

全球消化性溃疡治疗产业的主要参与者包括武田、葛兰素史克、卡迪拉医疗保健、奥罗宾度製药、兰伯西实验室、辉瑞、雷迪博士实验室、Strides Pharma、Phathom Pharmaceuticals、Granules India、阿斯利康、太阳製药、卫材和 Azurity Pharmaceuticals。为了巩固市场地位,消化性溃疡治疗领域的主要参与者正专注于各种策略性措施。许多公司正大力投资研发,以开发疗效更高、副作用更小的新疗法。配方改进,尤其是联合用药方案的改进,旨在提高治疗依从性并最大限度地减少復发。

企业也正在扩大生产能力,强化全球供应链,以确保更广泛的治疗可及性。此外,企业正在建立策略合作伙伴关係,并进行併购活动,以扩大产品组合和地理覆盖范围。有针对性的宣传活动和医生教育计画进一步提升了产品知名度和品牌信誉,尤其是在诊断和治疗率稳步攀升的新兴医疗保健市场。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 幽门螺旋桿菌感染盛行率上升

- 老年人口不断增加

- 扩大研发经费和活动

- 产业陷阱与挑战

- 长期使用PPI的副作用

- 市场机会

- 新疗法和药物输送创新

- 网路药局的扩张

- 成长动力

- 成长潜力分析

- 管道分析

- 监管格局

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係和合作

- 扩张计划

第五章:市场估计与预测:按药物类型,2021 年至 2034 年

- 主要趋势

- 质子帮浦抑制剂(PPI)

- H2受体拮抗剂

- 抗酸药

- 抗生素

- 细胞保护剂

- 其他药物类型

第六章:市场估计与预测:按溃疡类型,2021 年至 2034 年

- 主要趋势

- 胃溃疡

- 十二指肠溃疡

- 食道溃疡

第七章:市场估计与预测:依药物类型,2021 年至 2034 年

- 主要趋势

- 品牌

- 泛型

第八章:市场估计与预测:依管理路线,2021 年至 2034 年

- 主要趋势

- 口服肠外

第九章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 医院药房

- 零售药局

- 网路药局

第十章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- AstraZeneca

- Aurobindo Pharma

- Azurity Pharmaceuticals

- Cadila Healthcare

- Dr. Reddy's Laboratories

- Eisai

- GlaxoSmithKline

- Granules India

- Pfizer

- Phathom Pharmaceuticals

- Ranbaxy Laboratories

- Strides Pharma

- Sun Pharma

- Takeda

The Global Peptic Ulcers Treatment Market was valued at USD 5.1 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 8.6 billion by 2034. The market growth is largely driven by the rising incidence of gastrointestinal conditions among adults and the continued development of innovative pharmaceutical solutions. A key contributor to this demand is the widespread prevalence of Helicobacter pylori infections, which remain a dominant cause of peptic ulcers globally. As noted by global health bodies, this infection affects more than half the world's population, with particularly high rates in low- and middle-income regions. This alarming prevalence is expected to accelerate the demand for more effective treatment options to manage and eliminate the condition.

Another factor fueling market expansion is the increasing misuse of non-steroidal anti-inflammatory drugs, which often damage the stomach lining and lead to ulcer formation. Alongside this, advancements in diagnostics and the rising adoption of innovative treatment regimens-including dual and triple combination therapies-are improving patient recovery rates and minimizing ulcer recurrence. These factors, combined with rising awareness and enhanced healthcare accessibility in both developed and emerging countries, are expected to sustain steady demand for peptic ulcer treatment solutions in the coming years.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $5.1 Billion |

| Forecast Value | $8.6 Billion |

| CAGR | 5.3% |

The proton pump inhibitors (PPIs) segment generated USD 2.3 billion in 2024 and is forecasted to hit USD 3.7 billion by 2034, registering a CAGR of 5.1%. PPIs have become the cornerstone of ulcer therapy due to their effectiveness in reducing gastric acid levels, accelerating healing, and relieving pain. Their dependable efficacy and minimal side effects have made them widely preferred in treatment regimens. Their contribution to multi-drug therapy approaches for H. pylori eradication further cements their dominant market position. High healing success rates have been consistently reported in clinical settings, particularly when PPIs are administered over a treatment window of four to eight weeks.

The duodenal ulcers segment held a 50.8% share in 2024 and is set to experience significant growth throughout the forecast period. These ulcers typically form in the upper part of the small intestine and are primarily triggered by bacterial infection and long-term use of NSAIDs. They are prevalent across a broad population and frequently present with distinct symptoms that allow for quicker diagnosis and more immediate intervention, supporting higher treatment rates.

North America Peptic Ulcers Treatment Market generated USD 2.1 billion in 2024 and is expected to reach USD 3.6 billion by 2034, growing at a CAGR of 5.5%. This regional dominance can be attributed to the high burden of NSAID-related complications and H. pylori cases. A well-established healthcare framework, better access to advanced medications, and increasing awareness regarding gastrointestinal care and preventive health all contribute to the region's strong market position. Additionally, the active presence of leading pharmaceutical companies continues to support growth in this region.

Major players in the Global Peptic Ulcers Treatment Industry include Takeda, GlaxoSmithKline, Cadila Healthcare, Aurobindo Pharma, Ranbaxy Laboratories, Pfizer, Dr. Reddy's Laboratories, Strides Pharma, Phathom Pharmaceuticals, Granules India, AstraZeneca, Sun Pharma, Eisai, and Azurity Pharmaceuticals. To solidify their market positions, key players in the peptic ulcer treatment space are focusing on diverse strategic initiatives. Many are investing heavily in R&D to develop new therapies with higher efficacy and lower side effects. Formulation improvements, especially around combination drug regimens, are aimed at increasing treatment adherence and minimizing recurrence.

Companies are also expanding their manufacturing capabilities and strengthening their global supply chains to ensure wider access to treatment. Additionally, firms are entering strategic partnerships and engaging in mergers and acquisitions to broaden their portfolios and geographical presence. Targeted awareness campaigns and physician education programs further enhance product visibility and brand credibility, especially in emerging healthcare markets where diagnostic and treatment rates are steadily climbing.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Drug type

- 2.2.3 Ulcer type

- 2.2.4 Medication type

- 2.2.5 Route of administration

- 2.2.6 Distribution channel

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of Helicobacter pylori Infections

- 3.2.1.2 Growing geriatric population

- 3.2.1.3 Expanding R&D fundings and activities

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Side effects of long-term PPI use

- 3.2.3 Market opportunities

- 3.2.3.1 Novel therapies & drug delivery innovations

- 3.2.3.2 Expansion of online pharmacies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Regulatory landscape

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 Expansion plans

Chapter 5 Market Estimates and Forecast, By Drug Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Proton pump inhibitors (PPIs)

- 5.3 H2-receptor antagonists

- 5.4 Antacids

- 5.5 Antibiotics

- 5.6 Cytoprotective agents

- 5.7 Other drug types

Chapter 6 Market Estimates and Forecast, By Ulcer Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Gastric ulcers

- 6.3 Duodenal ulcers

- 6.4 Esophageal ulcers

Chapter 7 Market Estimates and Forecast, By Medication Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Branded

- 7.3 Generics

Chapter 8 Market Estimates and Forecast, By Route of Administration, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Oral Parenteral

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Hospital pharmacies

- 9.3 Retail pharmacies

- 9.4 Online pharmacies

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 AstraZeneca

- 11.2 Aurobindo Pharma

- 11.3 Azurity Pharmaceuticals

- 11.4 Cadila Healthcare

- 11.5 Dr. Reddy’s Laboratories

- 11.6 Eisai

- 11.7 GlaxoSmithKline

- 11.8 Granules India

- 11.9 Pfizer

- 11.10 Phathom Pharmaceuticals

- 11.11 Ranbaxy Laboratories

- 11.12 Strides Pharma

- 11.13 Sun Pharma

- 11.14 Takeda