|

市场调查报告书

商品编码

1782126

十二指肠溃疡治疗市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Duodenal Ulcer Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

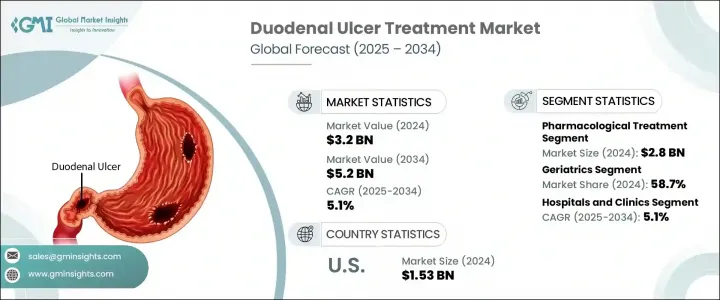

2024年,全球十二指肠溃疡治疗市场规模达32亿美元,预计2034年将以5.1%的复合年增长率成长,达到52亿美元。这一增长主要源于全球十二指肠溃疡病例的不断增加,而这些病例通常与营养不良、饮酒和吸烟习惯有关。人口老化也加剧了对治疗方案的需求,因为老年人更容易出现胃肠道併发症。 H2受体阻断剂和质子帮浦抑制剂(PPI)等药物因其可靠的抑酸能力和良好的安全性而得到越来越广泛的应用。

在许多治疗方案中,这些药物如今与针对幽门螺旋桿菌感染(十二指肠溃疡的主要病因)的抗生素合併使用。此外,硫糖铝和米索前列醇等药物因其对胃黏膜的保护作用而日益受到关注。人工智慧诊断、行动医疗工具和远距医疗的融合正在重塑溃疡治疗的提供方式,重点在于可及性和以患者为中心的治疗。随着越来越多的医疗保健系统采用数位健康模式和预防策略,各地区对可靠的十二指肠溃疡治疗的需求持续成长。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 32亿美元 |

| 预测值 | 52亿美元 |

| 复合年增长率 | 5.1% |

2024年,药物治疗领域收入达28亿美元。这一主导地位源于PPI和H2受体阻断剂等药物类别在快速缓解症状和持续控制酸度方面的有效性。这些药物因其易用性、口服给药和整体便利性而广受青睐,有助于居家照护和患者长期坚持用药。它们无需侵入性操作即可有效控制症状,使其成为医疗保健提供者和患者的首选,推动了该治疗类别的成长。

老年病学领域在2024年的市占率为58.7%。随着年龄增长,胃肠道保护功能下降,老年人更容易患溃疡,因此他们成为治疗方案的主要消费群体。此外,长期使用非类固醇类抗发炎药物 (NSAID) 治疗其他与年龄相关的疾病,会显着增加该族群罹患十二指肠溃疡的风险。由于长期接触溃疡诱因,需要针对老年患者制定长期预防性照护计画。

2025年,美国十二指肠溃疡治疗市场规模达15.3亿美元。由于幽门螺旋桿菌感染率不断上升、非类固醇抗发炎药物(NSAID)的频繁使用以及饮食风险因素的影响,美国市场持续成长。美国重视早期发现和完善的治疗方案,有助于及时诊断和介入。强大的医疗基础设施、广泛的宣传活动以及尖端诊断服务的可近性,确保了较高的治疗采用率。持续的治疗研究和创新投入也增强了美国在全球十二指肠溃疡治疗格局中的地位。

市场的主要参与者包括武田製药、雅培实验室、勃林格殷格翰、西普拉、卫材、葛兰素史克、辉瑞、默克、鲁宾、诺华、费罗兹森实验室、太阳製药、赛诺菲和阿斯特捷利康。为了巩固市场地位,十二指肠溃疡治疗领域的公司正在采取各种策略措施。专注于针对症状管理和根本病因(例如幽门螺旋桿菌)的先进药物研发。

许多公司正在透过合作伙伴关係、本地生产和区域行销策略来增强其全球影响力。数位化医疗整合,例如智慧监测和远距医疗治疗,正在被探索,以提高患者的参与度和依从性。此外,各公司正在多元化产品组合,纳入联合疗法,旨在提高疗效和依从性。策略定价、病患援助计画和医生教育活动也支持更广泛的市场渗透。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 幽门螺旋桿菌感染盛行率上升

- 远距医疗和数位诊断的扩展

- 人们对胃肠道健康的认识不断提高

- 抑酸疗法的技术进步

- 产业陷阱与挑战

- 内视镜和pH监测程序成本高昂

- 不良反应

- 市场机会

- 扩大发展中地区的医疗保健

- 加强公私合作,促进可负担药品供应

- 成长动力

- 成长潜力分析

- 管道分析

- 未来市场趋势

- 技术和创新格局

- 监管格局

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按治疗类型,2021 - 2034 年

- 主要趋势

- 药物治疗

- 药品类别

- 质子帮浦抑制剂

- H2拮抗剂

- 抗生素

- 其他药物类别

- 药物类型

- 品牌治疗

- 泛型

- 给药途径

- 口服

- 肠外

- 药品类别

- 手术

第六章:市场估计与预测:依年龄组,2021 年至 2034 年

- 主要趋势

- 成年人

- 老年病学

第七章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 医院和诊所

- 居家照护环境

- 门诊手术中心

- 其他最终用途

第八章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第九章:公司简介

- Abbott Laboratories

- AstraZeneca

- Boehringer Ingelheim

- Cipla

- Eisai

- Ferozsons Laboratories

- GlaxoSmithKline

- Lupin

- Merck

- Novartis

- Pfizer

- Sanofi

- Sun Pharma

- Takeda Pharmaceutical

The Global Duodenal Ulcer Treatment Market was valued at USD 3.2 billion in 2024 and is estimated to grow at a CAGR of 5.1% to reach USD 5.2 billion by 2034. This growth is largely fueled by rising cases of duodenal ulcers worldwide, often linked to poor nutrition, alcohol intake, and smoking habits. An aging population also contributes to increased demand for treatment solutions, as older individuals are more susceptible to gastrointestinal complications. Medications such as H2 receptor blockers and proton pump inhibitors (PPIs) are seeing heightened usage due to their reliable acid-suppressing abilities and favorable safety profiles.

In many treatment plans, these are now used in conjunction with antibiotics that target Helicobacter pylori infections- a leading cause of duodenal ulcers. Additionally, agents like sucralfate and misoprostol are gaining traction for their protective effects on the gastric lining. The integration of AI diagnostics, mobile health tools, and telemedicine is reshaping how ulcer care is delivered, with a focus on accessibility and patient-centered treatment. As more healthcare systems adopt digital health models and preventive strategies, the demand for reliable duodenal ulcer treatments continues to grow across all regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.2 Billion |

| Forecast Value | $5.2 Billion |

| CAGR | 5.1% |

The pharmacological therapies segment generated USD 2.8 billion in 2024. This dominance stems from the effectiveness of drug classes like PPIs and H2 blockers in providing quick symptom relief and consistent acid control. These medications are widely preferred for their ease of use, oral delivery, and overall convenience, which support home-based care and long-term patient adherence. Their ability to manage symptoms effectively without invasive procedures makes them the first choice for both healthcare providers and patients, pushing growth in this treatment category.

The geriatrics segment held a 58.7% share in 2024. Age-related declines in gastrointestinal protection increase vulnerability to ulcer formation among older adults, making them the primary consumer group for treatment options. Additionally, chronic use of non-steroidal anti-inflammatory drugs (NSAIDs) to manage other age-related conditions significantly raises the risk of duodenal ulcers in this demographic. This persistent exposure to ulcerogenic triggers calls for long-term and preventive care approaches tailored to senior patients.

United States Duodenal Ulcer Treatment Market was valued at USD 1.53 billion in 2025. The American market continues to grow due to the increasing prevalence of Helicobacter pylori infections, frequent NSAID use, and dietary risk factors. The country's emphasis on early detection and robust treatment protocols supports timely diagnosis and intervention. Strong infrastructure in healthcare delivery, along with extensive awareness campaigns and access to cutting-edge diagnostic services, ensures high treatment adoption. Ongoing investments in therapeutic research and innovation also bolster the country's role in shaping the global duodenal ulcer treatment landscape.

Key industry players in this market include Takeda Pharmaceutical, Abbott Laboratories, Boehringer Ingelheim, Cipla, Eisai, GlaxoSmithKline, Pfizer, Merck, Lupin, Novartis, Ferozsons Laboratories, Sun Pharma, Sanofi, and AstraZeneca. To strengthen their market position, companies operating in the duodenal ulcer treatment space are embracing various strategic initiatives. Investment in advanced drug development targeting both symptom management and root causes, such as Helicobacter pylori, is a key focus.

Many firms are enhancing their global reach through partnerships, local manufacturing, and regional marketing strategies. Digital health integration, such as smart monitoring and telehealth-enabled treatment, is being explored to boost patient engagement and adherence. Additionally, firms are diversifying portfolios to include combination therapies, aiming to improve efficacy and compliance. Strategic pricing, patient assistance programs, and physician education campaigns also support broader market penetration.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumption and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Treatment type

- 2.2.3 Age group

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of helicobacter pylori infections

- 3.2.1.2 Expansion of telemedicine and digital diagnostics

- 3.2.1.3 Growing awareness of gastrointestinal health

- 3.2.1.4 Technological advancements in acid-suppressing therapies

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of endoscopic and pH monitoring procedures

- 3.2.2.2 Adverse effects

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding healthcare in developing regions

- 3.2.3.2 Growing public-private partnerships for affordable drug access

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Pipeline analysis

- 3.5 Future market trends

- 3.6 Technology and innovation landscape

- 3.7 Regulatory landscape

- 3.7.1 North America

- 3.7.2 Europe

- 3.7.3 Asia Pacific

- 3.7.4 Latin America

- 3.7.5 Middle East and Africa

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Pharmacological treatment

- 5.2.1 Drug class

- 5.2.1.1 Proton pump inhibitors

- 5.2.1.2 H2 antagonists

- 5.2.1.3 Antibiotics

- 5.2.1.4 Other drug classes

- 5.2.2 Medication type

- 5.2.2.1 Branded Treatment

- 5.2.2.2 Generics

- 5.2.3 Route of administration

- 5.2.3.1 Oral

- 5.2.3.2 Parenteral

- 5.2.1 Drug class

- 5.3 Surgery

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adults

- 6.3 Geriatrics

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Homecare settings

- 7.4 Ambulatory surgical centers

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 AstraZeneca

- 9.3 Boehringer Ingelheim

- 9.4 Cipla

- 9.5 Eisai

- 9.6 Ferozsons Laboratories

- 9.7 GlaxoSmithKline

- 9.8 Lupin

- 9.9 Merck

- 9.10 Novartis

- 9.11 Pfizer

- 9.12 Sanofi

- 9.13 Sun Pharma

- 9.14 Takeda Pharmaceutical