|

市场调查报告书

商品编码

1773465

兽医神经退化性疾病诊断市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Veterinary Neurodegenerative Disease Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

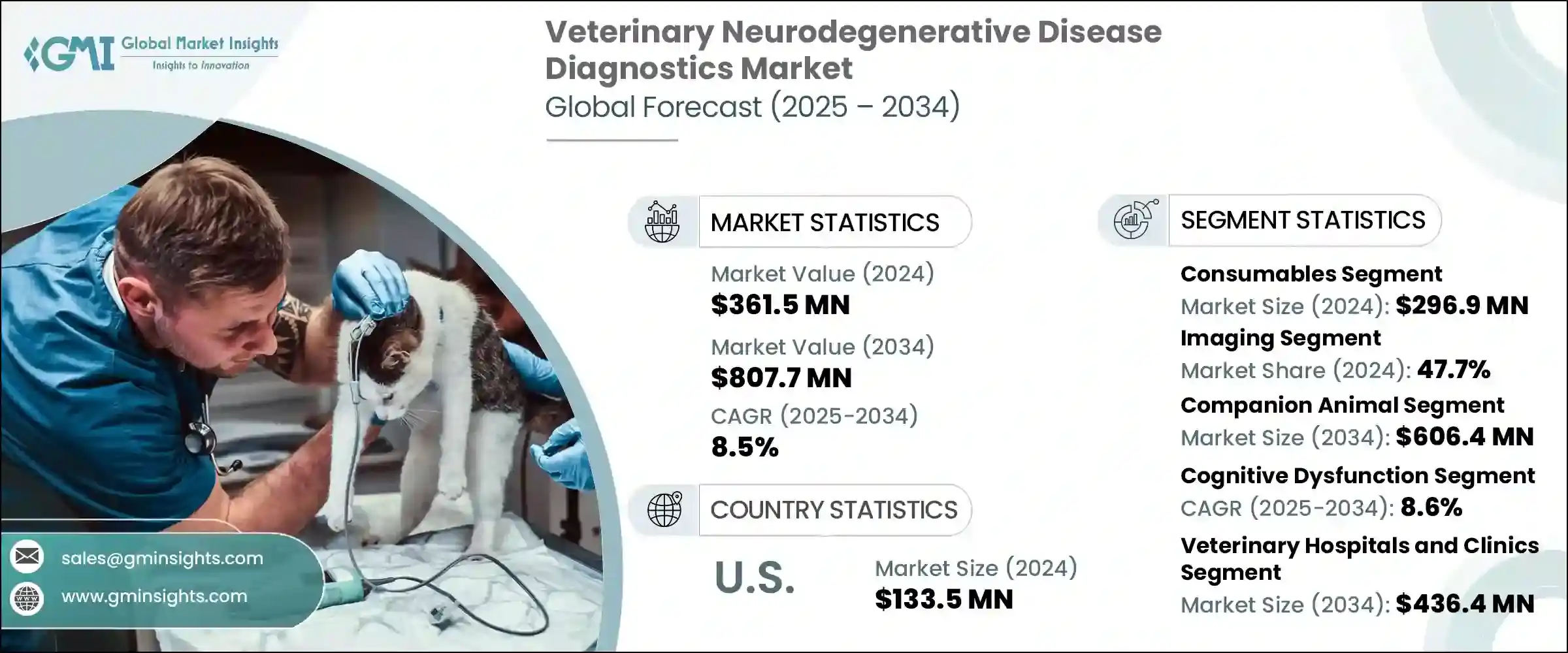

2024 年全球兽医神经退化性疾病诊断市场价值为 3.615 亿美元,预计到 2034 年将以 8.5% 的复合年增长率增长至 8.077 亿美元。这一成长在 2025 年至 2034 年期间的复合年增长率为 8.5%,其驱动力来自几个关键因素。动物神经系统疾病的增多,加上宠物拥有量和动物保健支出的激增,推动了对准确且易于获取的诊断工具的需求。随着全球伴侣动物和牲畜数量的迅速增加,对先进兽医诊断的需求变得比以往任何时候都更加迫切。兽医神经病学的技术进步也在重塑诊断方法方面发挥关键作用。成像、生物标记检测方面的创新以及高灵敏度诊断试剂盒的开发显着提高了疾病检测的精确度。

亚太、拉丁美洲和部分非洲地区的新兴经济体正在显着增加兽医诊所和流动医疗单位的建立。这些设施越来越多地配备了CT和MRI等尖端神经系统诊断工具,有助于提高诊断准确性和治疗效果。政府推出的动物健康和疾病预防支持政策也鼓励了公私投资。兽医保健领域的主要企业正在扩大其服务网络,并与参考实验室建立策略合作伙伴关係,以提高医疗服务匮乏地区的诊断服务覆盖率。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 3.615亿美元 |

| 预测值 | 8.077亿美元 |

| 复合年增长率 | 8.5% |

兽医神经退化性疾病诊断涵盖种类繁多的仪器和耗材,包括检测试剂、试剂、试剂盒和其他支援组件。这些产品用于开发和应用诊断解决方案,帮助识别和监测动物的神经系统疾病。市场按产品类型细分为耗材和仪器,其中耗材类别占据领先地位,2024 年的估值为 2.969 亿美元。耗材用于每个诊断程序,因此需要不断补充。这种重复使用确保了稳定的收入来源,并增强了对这些产品的需求。耗材的一次性使用特性、易于整合到兽医工作流程以及标准化的格式提供了便利性、一致性和可靠性——这些关键因素促使它们在诊所和实验室中广泛应用。

根据检测类型,市场可分为影像学、生物标记诊断检测和其他方法。 2024年,影像学占据了47.7%的市场份额,占据主导地位。它透过提供与脊椎退化或脑功能障碍等疾病相关的结构性问题的视觉洞察,在识别神经系统异常方面发挥着至关重要的作用。 CT和MRI技术在兽医环境中的日益普及,提高了这些诊断方法的可用性和有效性,并最终推动了影像学在整个市场中的主导地位。

依动物类型划分,市场分为伴侣动物和家畜。伴侣动物细分市场在2024年占据市场主导地位,预计2034年将达到6.064亿美元。这个细分市场受益于宠物拥有量的增加、人们对动物神经系统疾病认识的提高以及宠物主人投资专业诊断的趋势日益增强。随着与年龄相关的神经系统疾病在宠物身上的认知度不断提高,对精准早期检测的需求持续增长,从而推动了先进诊断解决方案的进一步应用。

以适应症分析,预计到2034年,认知功能障碍领域的复合年增长率将达到8.6%,这主要得益于动物年龄相关性神经功能衰退的发生率不断上升。这种疾病,尤其是在老年犬中,正日益引起宠物主人和兽医专业人士的注意。正在进行的研究和新型诊断测试的开发,使得认知问题的识别速度和准确性得以提高,有助于满足日益增长的需求。

就最终用途而言,市场细分为兽医院和诊所、诊断实验室和其他最终用户。兽医院和诊所在2024年成为领先细分市场,预计到2034年将达到4.364亿美元。这些机构通常资源丰富,拥有先进的诊断工具和熟练的专业人员,能够有效率地处理大量样本。它们能够提供准确及时的诊断,成为许多宠物主人的首选。对成像系统和神经诊断基础设施的投资进一步巩固了它们在该领域的主导地位。

从地理来看,北美在2024年以40.6%的市占率领先全球市场。光是美国一国的市场价值就达到了1.335亿美元,延续了前几年的上升趋势。该地区受益于强大的兽医基础设施、较高的宠物饲养率以及日益增强的宠物健康意识。先进的动物保健服务和日益普及的宠物保险政策也是推动该地区成长的重要因素。此外,城乡兽医设施网路的不断扩大也有助于扩大市场渗透率。

兽医神经退化性疾病诊断市场的竞争格局由全球巨头和区域专家组成。爱德士实验室 (IDEXX Laboratories)、默克动物保健 (Merck Animal Health)、维克 (Virbac) 和硕腾 (Zoetis) 等领先公司合计占约 45%-50% 的市场份额。他们的主导地位归功于广泛的产品组合、全球影响力以及对技术创新的持续投入。这些参与者正专注于收购、新产品开发和地理扩张等策略性倡议,以巩固其市场地位。同时,区域和本地供应商正在透过提供价格合理的诊断解决方案并采取併购和合作等成长策略来扩大市场份额,从而加剧竞争。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 每个阶段的增值

- 影响价值链的因素

- 产业衝击力

- 成长动力

- 动物神经系统疾病发生率上升

- 增进对动物神经生物学的理解

- 分子和影像诊断技术的进步

- 宠物拥有量和宠物医疗保健支出不断增长

- 扩大伴侣动物保险覆盖范围

- 产业陷阱与挑战

- 已验证的生物标誌物供应有限

- 兽医神经科医生和训练有素的专业人员短缺

- 机会

- 兽医基础设施快速发展

- 人工智慧和数位平台在诊断中的整合

- 成长动力

- 成长潜力分析

- 监管格局

- 技术格局

- 当前的技术趋势

- 新兴技术

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司市占率分析

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与协作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按产品,2021 - 2034 年

- 主要趋势

- 耗材

- 仪器

第六章:市场估计与预测:按测试类型,2021 - 2034 年

- 主要趋势

- 影像学

- MRI(磁振造影)

- CT(电脑断层扫描)

- 其他影像学检查

- 生物标记诊断测试

- 脑脊髓液 (CSF) 生物标记

- 血液生物标记

- 其他生物标记诊断测试

- 其他测试类型

第七章:市场估计与预测:按动物类型,2021 - 2034 年

- 主要趋势

- 伴侣动物

- 狗

- 猫

- 马匹

- 其他伴侣动物

- 牲畜

- 牛

- 绵羊和山羊

- 其他牲畜

第八章:市场估计与预测:按适应症,2021 - 2034 年

- 主要趋势

- 认知功能障碍

- 小脑萎缩

- 海绵状脑病

- 其他适应症

第九章:市场估计与预测:依最终用途,2021 - 2034 年

- 主要趋势

- 兽医医院和诊所

- 诊断实验室

- 其他最终用途

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Antech Diagnostics

- Avacta Animal Health Limited

- ACUVET BIOTECH

- Carestream Health

- IDEXX Laboratories

- Life Diagnostics

- Neurologica Corporation

- Merck Animal Health

- MI:RNA Diagnostics

- Mercodia AB

- Neogen Corporation

- Randox Laboratories

- Siemens Healthineers

- Virbac

- Zoetis

The Global Veterinary Neurodegenerative Disease Diagnostics Market was valued at USD 361.5 million in 2024 and is estimated to grow at a CAGR of 8.5% to reach USD 807.7 million by 2034. This growth, occurring at a CAGR of 8.5% from 2025 to 2034, is being driven by several key factors. The rise in neurological disorders among animals, coupled with a surge in pet ownership and spending on animal healthcare, is pushing demand for accurate and accessible diagnostic tools. With both companion and livestock animal populations increasing rapidly across the globe, the need for advanced veterinary diagnostics has become more pressing than ever. Technological advancements in veterinary neurology are also playing a crucial role in reshaping diagnostic approaches. Innovations in imaging, biomarker testing, and the development of highly sensitive diagnostic kits have significantly improved the precision of disease detection.

Emerging economies in Asia-Pacific, Latin America, and parts of Africa are witnessing a notable boost in the establishment of veterinary clinics and mobile care units. These facilities are increasingly equipped with cutting-edge neurological diagnostic tools such as CT and MRI, helping improve diagnostic accuracy and treatment outcomes. Supportive government policies focused on animal health and disease prevention are also encouraging public-private investments. Major corporations in the veterinary healthcare space are expanding their service networks and entering into strategic partnerships with reference laboratories, enhancing the availability of diagnostics in underserved regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $361.5 Million |

| Forecast Value | $807.7 Million |

| CAGR | 8.5% |

Veterinary neurodegenerative disease diagnostics comprise a wide array of instruments and consumables, including assays, reagents, kits, and other supporting components. These are used to develop and apply diagnostic solutions that help in the identification and monitoring of neurological conditions in animals. The market, segmented by product type into consumables and instruments, saw the consumables category leading with a valuation of USD 296.9 million in 2024. Consumables are used in every diagnostic procedure and thus need constant replenishment. This repetitive use ensures a steady revenue stream and strengthens the demand for these products. Their single-use nature, ease of integration into veterinary workflows, and standardized formats offer convenience, consistency, and reliability-key factors that contribute to their widespread adoption in clinics and labs.

On the basis of test type, the market is categorized into imaging, biomarker diagnostic tests, and other methods. Imaging held the dominant market share of 47.7% in 2024. It plays a vital role in identifying neurological abnormalities by providing visual insights into structural issues associated with diseases like spinal degeneration or brain dysfunction. The increasing integration of CT and MRI technologies in veterinary settings has improved the availability and effectiveness of these diagnostic methods, contributing to the dominance of imaging in the overall market.

By animal type, the market is segmented into companion animals and livestock animals. The companion animal segment led the market in 2024 and is projected to reach USD 606.4 million by 2034. This segment benefits from rising pet ownership, increasing awareness of animal neurological conditions, and the growing tendency among pet owners to invest in specialized diagnostics. As age-related neurological disorders become more recognized in pets, the need for precise and early detection continues to grow, prompting further use of advanced diagnostic solutions.

When analyzed by indication, cognitive dysfunction segment is expected to register a CAGR of 8.6% through 2034, driven by the rising occurrence of age-related neurological decline in animals. This condition, particularly in older dogs, is gaining greater awareness among pet owners and veterinary professionals alike. Ongoing research and the development of new diagnostic tests are enabling the identification of cognitive issues with improved speed and accuracy, helping to meet growing demand.

In terms of end use, the market is segmented into veterinary hospitals and clinics, diagnostic laboratories, and other end users. Veterinary hospitals and clinics emerged as the leading segment in 2024 and are anticipated to reach USD 436.4 million by 2034. These institutions are typically well-resourced, with advanced diagnostic tools and skilled professionals capable of processing a high volume of samples efficiently. Their ability to deliver accurate and timely diagnoses makes them the go-to choice for many pet owners. Investments in imaging systems and neurodiagnostic infrastructure further solidify their dominance in this space.

Geographically, North America led the global market with a share of 40.6% in 2024. The United States alone reached a market value of USD 133.5 million in 2024, continuing its upward trend from previous years. The region benefits from strong veterinary infrastructure, high rates of pet ownership, and growing awareness regarding pet health. The presence of advanced animal healthcare services and increasing adoption of pet insurance policies are also important factors fueling regional growth. Additionally, the expanding network of veterinary facilities in both urban and rural areas contributes to broader market penetration.

The competitive landscape in the veterinary neurodegenerative disease diagnostics market features a mix of global giants and regional specialists. Leading companies such as IDEXX Laboratories, Merck Animal Health, Virbac, and Zoetis collectively hold approximately 45%-50% of the market. Their dominance is attributed to broad product portfolios, global reach, and consistent investment in technological innovation. These players are focusing on strategic initiatives like acquisitions, new product development, and geographic expansion to strengthen their positions. Meanwhile, regional and local providers are intensifying competition by offering affordable diagnostic solutions and adopting growth strategies such as mergers and collaborations to expand their market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Test type

- 2.2.4 Animal type

- 2.2.5 Indication

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of neurological disorders in animals

- 3.2.1.2 Improved understanding of animal neurobiology

- 3.2.1.3 Technological advancements in molecular and imaging diagnostics

- 3.2.1.4 Growing pet ownership and pet healthcare spending

- 3.2.1.5 Expansion of companion animal insurance coverage

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Limited availability of validated biomarkers

- 3.2.2.2 Shortage of veterinary neurologists and trained professionals

- 3.2.3 Opportunities

- 3.2.3.1 Rapid veterinary infrastructure development

- 3.2.3.2 Integration of AI and digital platforms in diagnostics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technology landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Imaging

- 6.2.1 MRI (magnetic resonance imaging)

- 6.2.2 CT (computed tomography)

- 6.2.3 Other imaging tests

- 6.3 Biomarker diagnostic tests

- 6.3.1 CSF (cerebrospinal fluid) biomarkers

- 6.3.2 Blood-based biomarkers

- 6.3.3 Other biomarker diagnostic tests

- 6.4 Other test types

Chapter 7 Market Estimates and Forecast, By Animal Type, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Sheep and goats

- 7.3.3 Other livestock animals

Chapter 8 Market Estimates and Forecast, By Indication, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Cognitive dysfunction

- 8.3 Cerebellar abiotrophy

- 8.4 Spongiform encephalopathies

- 8.5 Other indications

Chapter 9 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Veterinary hospitals and clinics

- 9.3 Diagnostic laboratories

- 9.4 Other end use

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Antech Diagnostics

- 11.2 Avacta Animal Health Limited

- 11.3 ACUVET BIOTECH

- 11.4 Carestream Health

- 11.5 IDEXX Laboratories

- 11.6 Life Diagnostics

- 11.7 Neurologica Corporation

- 11.8 Merck Animal Health

- 11.9 MI:RNA Diagnostics

- 11.10 Mercodia AB

- 11.11 Neogen Corporation

- 11.12 Randox Laboratories

- 11.13 Siemens Healthineers

- 11.14 Virbac

- 11.15 Zoetis

动物用神经退化性疾病诊断的按全球市场,各产品类型,诊断试验,动物的类别,各适应症,各最终用途,各地区,机会,预测,2018年~2032年

动物用神经退化性疾病诊断的按全球市场,各产品类型,诊断试验,动物的类别,各适应症,各最终用途,各地区,机会,预测,2018年~2032年 动物神经退化性疾病诊断市场规模、份额、趋势分析报告(按动物类型、诊断测试、产品、适应症、最终用途、地区、细分市场预测),2025 年至 2030 年美国兽医神经退化性疾病诊断市场:市场规模、份额、趋势分析(按诊断测试、动物类型、产品类型、适应症、最终用途)、细分市场预测(2025-2030 年)

动物神经退化性疾病诊断市场规模、份额、趋势分析报告(按动物类型、诊断测试、产品、适应症、最终用途、地区、细分市场预测),2025 年至 2030 年美国兽医神经退化性疾病诊断市场:市场规模、份额、趋势分析(按诊断测试、动物类型、产品类型、适应症、最终用途)、细分市场预测(2025-2030 年) 动物神经退化性疾病诊断市场:市场规模、占有率、趋势、产业分析报告:依产品、检测方法、动物类型、适应症、最终用途、地区划分,预测至2025-2034年

动物神经退化性疾病诊断市场:市场规模、占有率、趋势、产业分析报告:依产品、检测方法、动物类型、适应症、最终用途、地区划分,预测至2025-2034年