|

市场调查报告书

商品编码

1773473

益生菌膳食补充剂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Probiotics Based Dietary Supplement Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

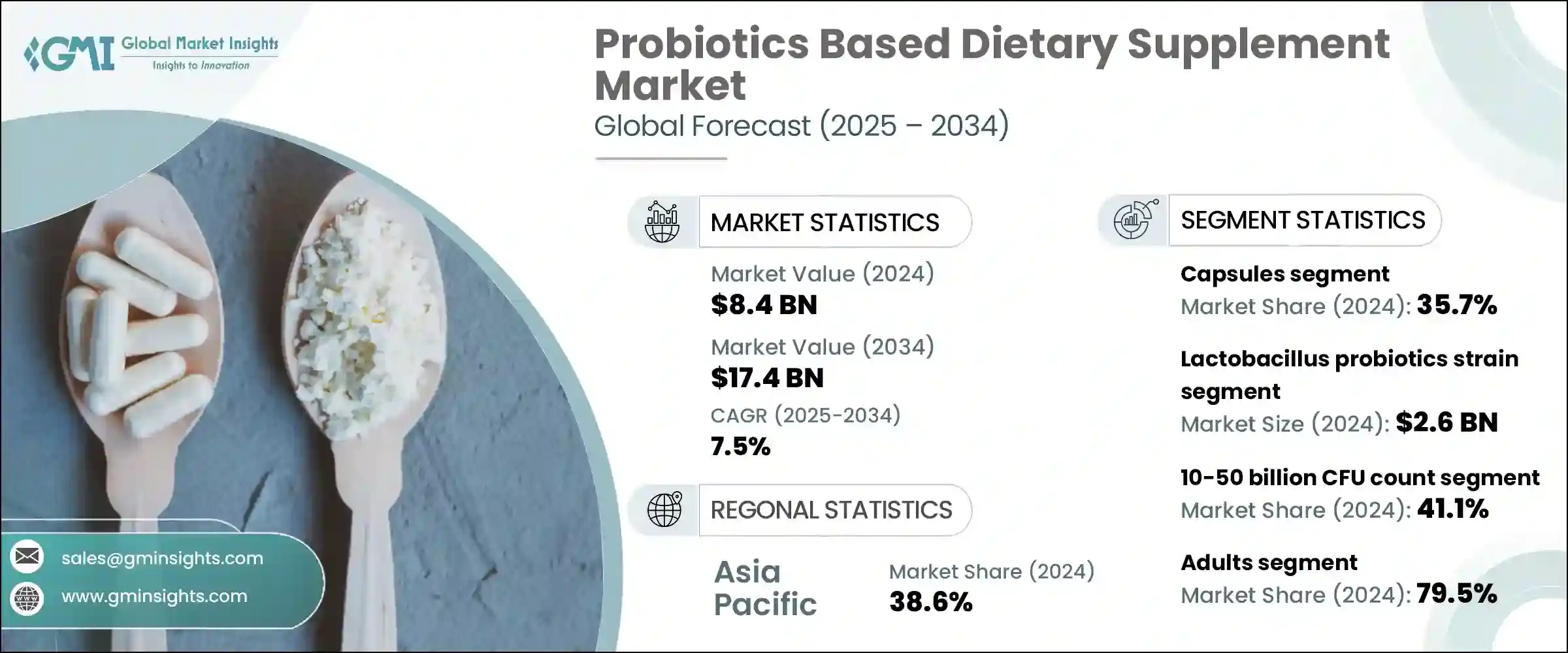

2024年,全球益生菌膳食补充剂市场规模达84亿美元,预计复合年增长率为7.5%,到2034年将达到174亿美元。这些补充剂采用乳酸桿菌、双歧桿菌和酿酒酵母等活性菌株精製而成,有助于维持消化平衡、增强免疫力并改善肠脑健康。人们对消化健康、预防性保健和无过敏原产品的关注度不断提高,刺激了市场需求。现今的消费者更青睐高菌落形成单位(CFU)、多菌株配方,以及软糖和小袋装等便利的包装形式。益生菌在婴儿、老年人和注重健康的成年人(尤其是在北美和亚太地区)中的应用日益广泛,为临床验证、给药系统和清洁标籤产品的创新创造了空间。

向无乳製品、注重透明度的产品和可持续采购的转变反映了健康意识和环保意识在营养领域的广泛趋势,将益生菌定位为预防性保健的核心支柱。消费者越来越严格地审查成分錶,要求符合道德价值和饮食限制的清洁标籤配方。这种行为转变加速了对植物性和无过敏原益生菌补充剂的需求,促使品牌在非乳製品载体、天然香料和可生物降解包装方面进行创新。随着人们对肠道在免疫力、情绪和整体活力方面作用的认识不断提高,益生菌不再被视为小众补充剂,而是日常必需品。这种演变正在改变製造商的产品开发方式,使其具备可追溯性、环境责任以及根据现代生活方式量身定制的个人化健康效果。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 84亿美元 |

| 预测值 | 174亿美元 |

| 复合年增长率 | 7.5% |

胶囊类产品占市场主导地位,占35.7%,2024年总额达30亿美元。其成功源自于精准剂量、长保质期和便利使用。素食、明胶和缓释剂型满足了消费者的多样化需求,确保益生菌能够承受胃酸侵蚀到达肠道。随着个人化肠道健康方案日益受到关注,针对消化、免疫和心理健康量身定制的高菌落形成单位(CFU)胶囊产品尤其受到追捧。

乳酸桿菌菌株市场占30.4%,2024年价值26亿美元。这些经过临床验证的菌株,如嗜酸乳桿菌、鼠李糖乳桿菌和植物乳桿菌,以改善肠道菌丛、增强免疫力和缓解乳糖不耐症而闻名。它们对胃酸的耐受性强,无论单菌或多菌种混合都具有良好的适应性,这使得它们在无乳製品和纯素益生菌产品中广受欢迎,尤其是在北美和亚洲市场。

2024年,亚太地区益生菌膳食补充剂市场占38.6%的市占率。该地区的成长动力源于日益增强的消化和免疫健康意识、更高的乳糖不耐症发病率、城镇化进程以及对功能性食品日益增长的需求。为了满足消费者的需求,本地和国际品牌正在扩大零售业务和研发规模,提供无乳糖、植物性益生菌产品。政府主导的健康运动、日益壮大的中产阶级以及发酵食品在该地区的热度,都推动了益生菌的大规模普及。

全球主要创新者和经销商包括养乐多株式会社 (Yakult Honsha Co., Ltd.)、BioGaia AB、雀巢公司 (Nestle SA)、达能公司 (Danone SA) 和科汉森控股公司 (Chr. Hansen Holding A/S)。领先的公司正在透过菌株多样化和透明标籤来增强竞争优势,以吸引註重健康和过敏原敏感的消费者。他们也投资临床试验,以验证对肠脑、免疫和消化系统健康的功效。产品形式的创新——包括纯素胶囊、缓释产品、软糖和粉末——正在扩大不同人群的可及性。各公司正在扩展电子商务管道和直接面向消费者的模式,同时与医疗保健专业人士和食品品牌建立合作伙伴关係,以提升信誉。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品形式,2021 - 2034 年

- 主要趋势

- 胶囊

- 素食胶囊

- 明胶胶囊

- 缓释胶囊

- 其他的

- 平板电脑

- 咀嚼片

- 肠溶片

- 其他的

- 粉末

- 单份小袋

- 散装容器

- 其他的

- 液体

- 镜头

- 掉落

- 其他的

- 软糖

- 明胶基

- 果胶基

- 其他的

- 其他的

第六章:市场估计与预测:按益生菌菌株,2021 - 2034 年

- 主要趋势

- 乳酸桿菌

- 嗜酸乳桿菌

- 鼠李糖乳桿菌

- 植物乳酸桿菌

- 干酪乳桿菌

- 罗伊氏乳桿菌

- 其他的

- 双歧桿菌

- 双歧桿菌

- 长双歧桿菌

- 乳酸双歧桿菌

- 短双歧桿菌

- 其他的

- 链球菌

- 嗜热链球菌

- 其他的

- 芽孢桿菌

- 凝结芽孢桿菌

- 枯草桿菌

- 其他的

- 酵母菌

- 布拉氏酵母菌

- 其他的

- 多菌株配方

- 其他的

第七章:市场估计与预测:按 CFU 计数,2021 - 2034 年

- 主要趋势

- 低于10亿CFU

- 10亿至100亿CFU

- 100-500亿CFU

- 超过500亿CFU

第八章:市场估计与预测:按消费者人口统计,2021 - 2034 年

- 主要趋势

- 成年人

- 18-34岁

- 35-54岁

- 55岁以上

- 孩子们

- 婴儿(0-2岁)

- 儿童(3-12岁)

- 青少年(13-17岁)

第九章:市场估计与预测:按健康应用,2021 - 2034 年

- 主要趋势

- 消化健康

- 肠躁症(IBS)

- 发炎性肠道疾病(IBD)

- 抗生素相关腹泻

- 其他的

- 免疫健康

- 女性健康

- 体重管理

- 大脑健康

- 口腔健康

- 其他的

第 10 章:市场估计与预测:按配销通路,2021 年至 2034 年

- 主要趋势

- 零售药局

- 健康与保健商店

- 超市和大卖场

- 网路零售

- 电子商务平台

- 品牌网站

- 网路药局

- 直销

- 其他的

第 11 章:市场估计与预测:按地区,2021 年至 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

第十二章:公司简介

- Chr. Hansen Holding A/S

- Danone SA (Activia, Actimel)

- Yakult Honsha Co., Ltd.

- Nestle SA (Garden of Life)

- Probi AB

- BioGaia AB

- Probiotics International Ltd (Protexin)

- Lallemand Inc.

- DuPont (IFF)

- Lifeway Foods, Inc.

- Morinaga Milk Industry Co., Ltd.

- Bifodan A/S

- Culturelle (i-Health, Inc.)

- Jarrow Formulas, Inc.

- NOW Foods

The Global Probiotics Based Dietary Supplement Market was valued at USD 8.4 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 17.4 billion by 2034. These supplements, crafted with live strains like Lactobacillus, Bifidobacterium, and Saccharomyces, support digestive balance, bolster immunity, and enhance gut-brain health. Rising awareness around digestive wellness, preventive health, and allergen-free options is spurring demand. Today's consumers are opting for high-CFU, multi-strain formulations, as well as convenient formats like gummies and sachets. Broadening use among infants, seniors, and health-conscious adults-especially across North America and Asia-Pacific-is creating space for innovations in clinical validation, delivery systems, and clean-label offerings.

The shift toward dairy-free, transparency-focused products and sustainable sourcing reflects a wider trend in health-conscious and eco-minded nutrition, positioning probiotics as a central pillar of preventive wellness. Consumers are increasingly scrutinizing ingredient lists, demanding clean-label formulations that align with ethical values and dietary restrictions. This behavioral shift is accelerating the demand for plant-based and allergen-free probiotic supplements, pushing brands to innovate with non-dairy carriers, natural flavorings, and biodegradable packaging. As awareness grows around the gut's role in immunity, mood, and overall vitality, probiotics are no longer viewed as niche supplements but rather as daily essentials. This evolution is transforming how manufacturers approach product development, with traceability, environmental responsibility, and personalized health outcomes tailored to modern lifestyles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.4 Billion |

| Forecast Value | $17.4 Billion |

| CAGR | 7.5% |

The capsule segment dominated the market with a 35.7% share, totaling USD 3 billion in 2024. Their success is due to precise dosage, long shelf-life, and ease of use. Vegetarian, gelatin, and delayed-release versions cater to diverse consumer needs, ensuring probiotics survive stomach acid to reach the gut. High-CFU capsule options tailored for digestion, immunity, and mental health are particularly sought after amid growing interest in personalized gut health regimens.

Lactobacillus strains segment made up 30.4% share, worth USD 2.6 billion in 2024. These clinically backed strains-such as L.acidophilus, L.rhamnosus, and L.plantarum-are known for improving gut flora, strengthening immunity, and aiding lactose intolerance. Their resilience against stomach acid and adaptability in both single- and multi-strain blends make them popular in dairy-free and vegan probiotic products, especially prevalent in North American and Asian markets.

Asia-Pacific Probiotics Based Dietary Supplement Market held a 38.6% share in 2024. Growth in this region is driven by increasing digestive and immune health awareness, higher lactose intolerance rates, urbanization, and rising demand for functional foods. Local and international brands are expanding their retail presence and R&D to meet consumer needs, offering lactose-free, plant-based probiotic options. Government-led wellness campaigns, a growing middle class, and the regional popularity of fermented foods are contributing to mass adoption.

Key global innovators and distributors include Yakult Honsha Co., Ltd., BioGaia AB, Nestle S.A., Danone S.A., and Chr. Hansen Holding A/S. Leading firms are sharpening their competitive edge through strain diversification and transparent labeling, appealing to health-conscious and allergen-sensitive consumers. They're also investing in clinical trials to validate gut-brain, immune, and digestive health claims. Format innovation-with vegan capsules, delayed-release options, gummies, and powders-is broadening access across demographics. Companies are expanding e-commerce channels and direct-to-consumer models while forming partnerships with healthcare professionals and food brands to boost credibility.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Format, 2021 - 2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Capsules

- 5.2.1 Vegetarian capsules

- 5.2.2 Gelatin capsules

- 5.2.3 Delayed-release capsules

- 5.2.4 Others

- 5.3 Tablets

- 5.3.1 Chewable tablets

- 5.3.2 Enteric-coated tablets

- 5.3.3 Others

- 5.4 Powders

- 5.4.1 Single-serve sachets

- 5.4.2 Bulk containers

- 5.4.3 Others

- 5.5 Liquids

- 5.5.1 Shots

- 5.5.2 Drops

- 5.5.3 Others

- 5.6 Gummies

- 5.6.1 Gelatin-based

- 5.6.2 Pectin-based

- 5.6.3 Others

- 5.7 Others

Chapter 6 Market Estimates and Forecast, By Probiotic Strain, 2021 - 2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Lactobacillus

- 6.2.1 L. acidophilus

- 6.2.2 L. rhamnosus

- 6.2.3 L. plantarum

- 6.2.4 L. casei

- 6.2.5 L. reuteri

- 6.2.6 Others

- 6.3 Bifidobacterium

- 6.3.1 B. bifidum

- 6.3.2 B. longum

- 6.3.3 B. lactis

- 6.3.4 B. breve

- 6.3.5 Others

- 6.4 Streptococcus

- 6.4.1 S. thermophilus

- 6.4.2 Others

- 6.5 Bacillus

- 6.5.1 B. coagulans

- 6.5.2 B. subtilis

- 6.5.3 Others

- 6.6 Saccharomyces

- 6.6.1 S. boulardii

- 6.6.2 Others

- 6.7 Multi-strain formulations

- 6.8 Others

Chapter 7 Market Estimates and Forecast, By CFU Count, 2021 - 2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Below 1 billion CFU

- 7.3 1-10 billion CFU

- 7.4 10-50 billion CFU

- 7.5 Above 50 billion CFU

Chapter 8 Market Estimates and Forecast, By Consumer Demographics, 2021 - 2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 Adults

- 8.2.1 18-34 Years

- 8.2.2 35-54 Years

- 8.2.3 55+ Years

- 8.3 Children

- 8.3.1 Infants (0-2 Years)

- 8.3.2 Children (3-12 Years)

- 8.3.3 Adolescents (13-17 Years)

Chapter 9 Market Estimates and Forecast, By Health Application, 2021 - 2034 (USD Million) (Kilo Tons)

- 9.1 Key trends

- 9.2 Digestive health

- 9.2.1 Irritable bowel syndrome (IBS)

- 9.2.2 Inflammatory bowel disease (IBD)

- 9.2.3 Antibiotic-associated diarrhea

- 9.2.4 Others

- 9.3 Immune health

- 9.4 Women's health

- 9.5 Weight management

- 9.6 Brain health

- 9.7 Oral health

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Million) (Kilo Tons)

- 10.1 Key trends

- 10.2 Retail pharmacies

- 10.3 Health & wellness stores

- 10.4 Supermarkets & hypermarkets

- 10.5 Online retail

- 10.5.1 E-commerce platforms

- 10.5.2 Brand websites

- 10.5.3 Online pharmacies

- 10.6 Direct selling

- 10.7 Others

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Million) (Kilo Tons)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 Saudi Arabia

- 11.6.2 South Africa

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Chr. Hansen Holding A/S

- 12.2 Danone S.A. (Activia, Actimel)

- 12.3 Yakult Honsha Co., Ltd.

- 12.4 Nestle S.A. (Garden of Life)

- 12.5 Probi AB

- 12.6 BioGaia AB

- 12.7 Probiotics International Ltd (Protexin)

- 12.8 Lallemand Inc.

- 12.9 DuPont (IFF)

- 12.10 Lifeway Foods, Inc.

- 12.11 Morinaga Milk Industry Co., Ltd.

- 12.12 Bifodan A/S

- 12.13 Culturelle (i-Health, Inc.)

- 12.14 Jarrow Formulas, Inc.

- 12.15 NOW Foods