|

市场调查报告书

商品编码

1782154

企业文件同步与分享市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Enterprise File Sync and Share Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

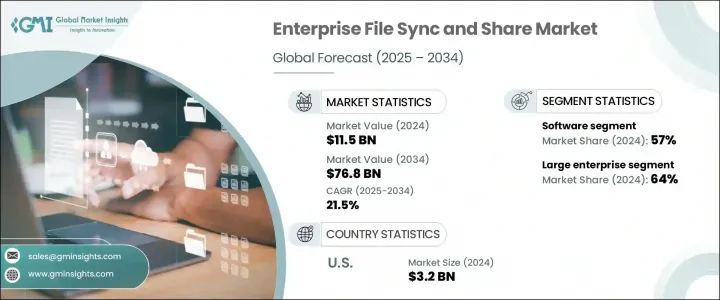

2024年,全球企业文件同步与共享市场规模达115亿美元,预计到2034年将以21.5%的复合年增长率成长,达到768亿美元。包括远距办公和混合办公模式在内的灵活办公环境的兴起,推动了对安全高效的资料共享解决方案的广泛需求。越来越多的企业选择EFSS平台,以确保跨装置檔案同步顺畅,实现无缝协作,无论身在何处。随着劳动力日益分散,数位化工具日益重要,EFSS已成为维持生产力、减少停机时间并支援许多企业目前推行的「行动优先」模式的关键解决方案。

随着人们对网路安全、资料外洩和监管要求的担忧日益加深,企业纷纷采用 EFSS 工具,这些工具提供内建保护功能,例如加密、存取控制、资料遗失防护,并支援符合 GDPR、HIPAA 和 ISO 等全球标准。这些系统允许透过安全管道共享内部和外部文件,使企业能够更轻鬆地履行法律义务并维护客户信任。日益增长的风险状况和日益严格的资料治理要求,已将 EFSS 技术定位为降低风险和确保业务连续性的重要组成部分。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 115亿美元 |

| 预测值 | 768亿美元 |

| 复合年增长率 | 21.5% |

2024年,软体领域占据了EFSS市场57%的份额,预计在2025-2034年期间的复合年增长率将达到20%。如今,企业需要配备先进保护措施(例如端到端加密、数位版权控制和多因素身份验证)的安全数位檔案共享工具。网路事件的不断增加,已使企业的重点转向在访问便利性和企业级安全性之间取得平衡的解决方案。这一趋势凸显了EFSS软体日益增长的重要性,该软体能够满足各行各业对可用性和严格资料保护的要求。

大型企业占了64%的市场份额,预计到2034年将以21%的复合年增长率成长。这些公司通常会部署混合云或多云基础设施,以增强协作、资料隐私和营运效率。与这些环境整合的EFSS解决方案可让敏感资料保留在本机系统中,同时利用云端的可扩充性为分散式团队提供服务。这种混合方法提供了大型组织所需的灵活性和控制力,尤其是在管理法规遵循和降低跨区域营运延迟方面。

北美企业文件同步与共享市场占75%的市场份额,2024年市场规模达32亿美元。北美在数位基础设施和云端运算应用方面的领先地位推动了文件共享平台的广泛应用。许多不同产业的企业都依赖EFSS工具来简化工作流程、实现远端团队协作,并透过高效能互联网服务和先进的云端生态系统来保护资料。

强大的基础设施以及 IBM、Dropbox、微软、Google、Citrix Systems、Egnyte 和 Box 等主要云端服务供应商,持续巩固了该国在这个快速成长的市场中的竞争优势。领先的 EFSS 供应商正在透过创新、整合和企业级服务等多种方式增强其影响力。各公司优先考虑人工智慧增强的搜寻和自动化功能、与生产力套件的无缝互通性以及行动友善介面,以提高用户采用率。他们还在增强安全协议、扩展多云相容性,并为受监管行业提供合规框架。与云端基础设施供应商建立策略合作伙伴关係、将产品与协作工具捆绑销售以及积极的定价模式,进一步帮助主要参与者在竞争环境中脱颖而出。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 成本结构

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 远距工作解决方案需求不断成长

- 云端服务的采用率不断上升

- 行动服务和 BYOD 政策的使用日益增多

- 对资料安全和合规性的担忧日益增加

- 产业陷阱与挑战

- 资料主权和合规性的复杂性

- 与遗留系统的整合问题

- 市场机会

- 对行业特定合规解决方案的需求不断增长

- 透过采用云端运算技术在新兴经济体中扩张

- 人工智慧与自动化的融合,提高生产力

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 成本細項分析

- 专利分析

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

- 用例

- 最佳情况

第四章:竞争格局

- 介绍

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 战略展望矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划和资金

第五章:市场估计与预测:按组件,2021 - 2034 年

- 主要趋势

- 软体

- 服务

第六章:市场估计与预测:依企业规模,2021 - 2034 年

- 主要趋势

- 中小企业

- 大型企业

第七章:市场估计与预测:依部署模式,2021 - 2034 年

- 主要趋势

- 本地

- 云

- 杂交种

第八章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 檔案储存和备份

- 内容管理备份

- 行动存取和生产力

- 文件协作

- 分析和报告

- 其他的

第九章:市场估计与预测:依产业垂直,2021 - 2034 年

- 主要趋势

- 金融服务业

- 软体

- 服务

- 卫生保健

- 软体

- 服务

- 媒体和娱乐

- 软体

- 服务

- 资讯科技和电信

- 软体

- 服务

- 零售与电子商务

- 软体

- 服务

- 政府和公共部门

- 软体

- 服务

- 运输与物流

- 软体

- 服务

- 其他的

- 软体

- 服务

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 北欧人

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳新银行

- 东南亚

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- MEA

- 阿联酋

- 沙乌地阿拉伯

- 南非

第 11 章:公司简介

- Accellion / Kiteworks

- Acronis

- BlackBerry

- Box

- Citrix Systems

- CTERA Networks

- Dropbox

- Egnyte

- IBM

- Microsoft

- Next cloud

- OpenText

- own Cloud

- Pydio

- Sugar Sync

- Syncplicity

- Thru

- Tresorit

- VMware

The Global Enterprise File Sync and Share Market was valued at USD 11.5 billion in 2024 and is estimated to grow at a CAGR of 21.5% to reach USD 76.8 billion by 2034. The rise of flexible work environments, including remote and hybrid models, has fueled widespread demand for secure, efficient data-sharing solutions. Businesses are increasingly turning to EFSS platforms that ensure smooth file synchronization across devices, enabling seamless collaboration regardless of location. With workforces becoming more decentralized and digital tools more essential, EFSS has emerged as a critical solution for maintaining productivity, reducing downtime, and supporting the mobile-first approach many organizations now embrace.

As concerns surrounding cybersecurity, data breaches, and regulatory mandates grow, businesses are adopting EFSS tools that offer built-in protections such as encryption, access controls, data loss prevention, and support for compliance with global standards like GDPR, HIPAA, and ISO. These systems allow internal and external file sharing through secure channels, making it easier for enterprises to meet legal obligations and protect client trust. The increasing risk landscape and stringent data governance requirements have positioned EFSS technologies as essential components for risk mitigation and business continuity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.5 Billion |

| Forecast Value | $76.8 Billion |

| CAGR | 21.5% |

In 2024, the software segment held a 57% share of the EFSS market and is projected to grow at a CAGR of 20% during 2025-2034. Organizations now demand secure digital file-sharing tools equipped with advanced protections like end-to-end encryption, digital rights controls, and multifactor authentication. The rising number of cyber incidents has shifted enterprise focus toward solutions that balance ease of access with enterprise-grade security. The trend highlights the growing importance of EFSS software that addresses both usability and strict data protection expectations across industries.

The large enterprises segment held a 64% share and is anticipated to grow at a CAGR of 21% through 2034. These companies often implement hybrid or multi-cloud infrastructures to enhance collaboration, data privacy, and operational efficiency. EFSS solutions that integrate with these environments allow sensitive data to remain in on-premises systems while leveraging the scalability of the cloud for distributed teams. This hybrid approach offers flexibility and control that large organizations require, especially in managing regulatory compliance and reducing latency across regional operations.

North America Enterprise File Sync and Share Market held a 75% share and generated USD 3.2 billion in 2024. The country's leadership in digital infrastructure and cloud adoption has fueled widespread implementation of file-sharing platforms. Many businesses across sectors rely on EFSS tools to streamline workflow, enable remote team collaboration, and safeguard data with high-performing internet services and sophisticated cloud ecosystems.

Robust infrastructure, along with major cloud providers like IBM, Dropbox, Microsoft Corporation, Google, Citrix Systems, Egnyte, and Box, continues to reinforce the country's competitive edge in this fast-growing market. Leading EFSS providers are strengthening their presence through a mix of innovation, integrations, and enterprise-grade service offerings. Companies are prioritizing AI-enhanced search and automation features, seamless interoperability with productivity suites, and mobile-friendly interfaces to improve user adoption. They are also enhancing security protocols, expanding multi-cloud compatibility, and offering compliance-ready frameworks for regulated sectors. Strategic partnerships with cloud infrastructure providers, product bundling with collaboration tools, and aggressive pricing models have further helped key players differentiate themselves in a competitive environment.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Component

- 2.2.3 Enterprise size

- 2.2.4 Deployment mode

- 2.2.5 Application

- 2.2.6 Industry vertical

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for remote work solutions

- 3.2.1.2 Rising adoption of cloud-based service

- 3.2.1.3 Growing use of mobile services and BYOD policies

- 3.2.1.4 Increasing concerns over data security and compliance

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data sovereignty and compliance complexities

- 3.2.2.2 Integration issues with legacy system

- 3.2.3 Market opportunities

- 3.2.3.1 Growing demand for industry-specific compliance solutions

- 3.2.3.2 Expansion in emerging economies with cloud adoption

- 3.2.3.3 Integration of AI and automation for enhanced productivity

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Cost breakdown analysis

- 3.9 Patent analysis

- 3.10 Sustainability and environmental aspects

- 3.10.1 Sustainable practices

- 3.10.2 Waste reduction strategies

- 3.10.3 Energy efficiency in production

- 3.10.4 Eco-friendly initiatives

- 3.10.5 Carbon footprint considerations

- 3.11 Use cases

- 3.12 Best-case scenario

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Software

- 5.3 Services

Chapter 6 Market Estimates & Forecast, By Enterprise Size, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 SMEs

- 6.3 Large enterprise

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 On-premises

- 7.3 Cloud

- 7.4 Hybrid

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 File storage & backup

- 8.3 Content management backup

- 8.4 Mobile access & productivity

- 8.5 Document collaboration

- 8.6 Analytics & reporting

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Industry Vertical, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 BFSI

- 9.2.1 Software

- 9.2.2 Services

- 9.3 Healthcare

- 9.3.1 Software

- 9.3.2 Services

- 9.4 Media & entertainment

- 9.4.1 Software

- 9.4.2 Services

- 9.5 IT & Telecom

- 9.5.1 Software

- 9.5.2 Services

- 9.6 Retail & E-commerce

- 9.6.1 Software

- 9.6.2 Services

- 9.7 Government & Public sector

- 9.7.1 Software

- 9.7.2 Services

- 9.8 Transportation & logistics

- 9.8.1 Software

- 9.8.2 Services

- 9.9 Others

- 9.9.1 Software

- 9.9.2 Services

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Accellion / Kiteworks

- 11.2 Acronis

- 11.3 BlackBerry

- 11.4 Box

- 11.5 Citrix Systems

- 11.6 CTERA Networks

- 11.7 Dropbox

- 11.8 Egnyte

- 11.9 Google

- 11.10 IBM

- 11.11 Microsoft

- 11.12 Next cloud

- 11.13 OpenText

- 11.14 own Cloud

- 11.15 Pydio

- 11.16 Sugar Sync

- 11.17 Syncplicity

- 11.18 Thru

- 11.19 Tresorit

- 11.20 VMware

2026年全球企业文件同步与共用(EFSS)市场报告

2026年全球企业文件同步与共用(EFSS)市场报告 企业文件同步与共用(EFSS) 市场分析及至 2035 年预测:依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分

企业文件同步与共用(EFSS) 市场分析及至 2035 年预测:依类型、产品类型、服务、技术、组件、应用、部署类型、最终用户及功能划分 企业文件同步与共用软体市场(依服务类型、使用者类型、应用程式类型、部署模式和垂直领域)-2025-2032 年全球预测

企业文件同步与共用软体市场(依服务类型、使用者类型、应用程式类型、部署模式和垂直领域)-2025-2032 年全球预测 企业文件同步和共享市场-全球产业规模、份额、趋势、机会和预测(按产品、按业务功能、按应用、按地区、按竞争)2020-2030F

企业文件同步和共享市场-全球产业规模、份额、趋势、机会和预测(按产品、按业务功能、按应用、按地区、按竞争)2020-2030F 企业文件同步和共享市场报告(按组件、部署类型、组织规模、应用、行业垂直和地区)2025 年至 2033 年

企业文件同步和共享市场报告(按组件、部署类型、组织规模、应用、行业垂直和地区)2025 年至 2033 年 2025-2029 年全球企业文件同步与共用市场

2025-2029 年全球企业文件同步与共用市场 企业文件同步与共用:市场占有率分析、产业趋势与统计、成长预测(2025-2030)

企业文件同步与共用:市场占有率分析、产业趋势与统计、成长预测(2025-2030) 企业文件同步与共用(EFSS) 市场规模、份额、趋势分析报告:按产品、按部署、按企业规模、按应用程式、按最终用途、按地区、按细分市场、预测,2024-2030 年

企业文件同步与共用(EFSS) 市场规模、份额、趋势分析报告:按产品、按部署、按企业规模、按应用程式、按最终用途、按地区、按细分市场、预测,2024-2030 年