|

市场调查报告书

商品编码

1797682

智慧宠物餵食器市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Smart Pet Feeder Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

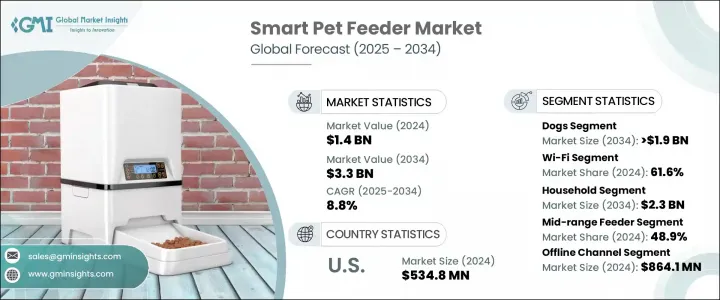

2024年,全球智慧宠物餵食器市场规模达14亿美元,预计2034年将以8.8%的复合年增长率成长,达到33亿美元。这一增长主要归因于全球宠物拥有量的激增、可支配收入的提高,以及人们越来越倾向于将宠物视为家庭成员。年轻的宠物主人越来越多地将智慧科技融入宠物照护的日常中,以确保宠物的便利性、健康和合理的营养。能够按预定时间间隔精准分配食物的自动餵食器越来越受欢迎,尤其是那些能够连接手机应用程式、内建相机和语音功能的餵食器。

智慧家庭的蓬勃发展进一步激发了人们对连网宠物餵食解决方案的兴趣,尤其是在消费者需要更多远端控制和监控功能的情况下。电商平台正在大幅扩大这些产品的覆盖范围,协助其渗透成熟市场和发展中市场。这些设备配备了防堵塞分配器、防篡改盖子和安全隔间,以保护食物并防止其他动物接触,从而解决了污染和过度进食的问题。智慧餵食器高度重视自动化、安全性和使用者友善性,正迅速成为科技驱动宠物家庭的必备之选。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 14亿美元 |

| 预测值 | 33亿美元 |

| 复合年增长率 | 8.8% |

预计到2034年,猫咪餵食器市场的复合年增长率将达到9.2%,这得益于养猫人数的显着增长以及人们对猫咪健康和营养的日益关注。猫主人正在积极寻求能够有效分配和保存干湿粮的自动化解决方案。专为猫咪设计的餵食器通常包含基于人工智慧的定时餵食、密封的储藏室和冷藏功能,对于那些希望保持猫咪食物新鲜和规律餵食习惯的人来说,它们是一个实用的选择。这些创新对于宠物主人可能长时间外出且需要可靠、定时餵食的家庭来说至关重要。

2024年,支援Wi-Fi的智慧餵食器占据了市场主导地位,市场份额达61.6%,因为它们透过行动应用程式提供先进的远端功能。这些餵食器允许宠物主人管理餵食时间、透过即时视讯监控宠物,并在任何有网路连线的地方调整餵食量。智慧型手机使用率的上升、家庭互联互通的增强以及数位技术的日益普及,促使人们更倾向于选择基于Wi-Fi的系统,而非蓝牙或手动选项。这些解决方案能够与更广泛的智慧家庭生态系统无缝集成,对科技爱好者极具吸引力。

美国智慧宠物餵食器市场规模在2024年达到5.348亿美元,高于2023年的4.993亿美元。预计2025年至2034年期间,该市场的复合年增长率将达到8.6%,这得益于宠物饲养的普及、强大的数位基础设施以及互联宠物护理产品的快速普及。美国消费者尤其青睐创新的自动化解决方案,不仅能提供便利,还能提供更优质的动物照护。该地区拥有成熟的分销网络、较高的可支配收入以及先进的兽医医疗保健体系,所有这些都支持市场的持续成长。

全球智慧宠物餵食器市场的主要公司包括 Whisker、Dogness、PetSafe Brands、Tuya、Sure Petcare、Wopet、PETLIBRO、Geeni、小米、HONEYGUARDIAN、Pawbo、Aqara、Catit、Arf Pets、Okos Smart Pet Feeder 和 BeardPet。这些公司持续推动产品创新,以满足日益增长的消费者需求。智慧宠物餵食器市场的领先公司正在大力投资产品创新,专注于增强功能,例如健康监测、即时视讯存取、AI 驱动的餵食演算法和语音整合。为了巩固市场地位,各大品牌优先考虑无缝的行动应用介面以及与现有智慧家庭生态系统的兼容性。与电子商务平台和零售连锁店的策略合作伙伴关係拓宽了产品的覆盖范围,同时公司也在强调以用户为中心的设计和耐用的製造品质。许多公司正在使其产品组合多样化,包括针对特定宠物需求(例如湿粮储存或多宠物家庭)量身定制的餵食器。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 产业衝击力

- 成长动力

- 宠物拥有量不断增加

- 不断进步的技术

- 提高对宠物健康和营养的认识

- 产业陷阱与挑战

- 对技术可靠性的担忧

- 初始成本高

- 市场机会

- 拓展电子商务平台

- 与宠物食品品牌的合作

- 成长动力

- 成长潜力分析

- 监管格局

- 宠物数量统计

- 定价分析

- 技术进步

- 当前的技术趋势

- 新兴技术

- 消费者行为分析

- 差距分析

- 未来市场趋势

- 波特的分析

- PESTEL分析

第四章:竞争格局

- 介绍

- 公司矩阵分析

- 公司市占率分析

- 北美洲

- 欧洲

- 亚太地区

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

第五章:市场估计与预测:按宠物类型,2021 - 2034 年

- 主要趋势

- 狗

- 猫

- 其他宠物类型

第六章:市场估计与预测:按连结类型,2021 - 2034 年

- 主要趋势

- 蓝牙

- 无线上网

- 其他连线类型

第七章:市场估计与预测:按应用,2021 - 2034 年

- 主要趋势

- 家庭

- 商业的

第八章:市场估计与预测:按价格区间,2021 年至 2034 年

- 主要趋势

- 低成本餵料器

- 中程送料器

- 高端送料器

第九章:市场估计与预测:按配销通路,2021 - 2034 年

- 主要趋势

- 线上通路

- 线下通路

- 实体宠物店

- 实体大众商店

第十章:市场估计与预测:按地区,2021 - 2034 年

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 亚太地区

- 日本

- 中国

- 印度

- 澳洲

- 韩国

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 中东和非洲

- 南非

- 沙乌地阿拉伯

- 阿联酋

第 11 章:公司简介

- Aqara

- Arf Pets

- BeardPet

- Catit (Rolf C Hagen)

- Dogness

- Geeni

- HONEYGUARDIAN

- Okos Smart Pet Feeder

- Pawbo

- Petlibro

- PetSafe Brands

- Sure Petcare (Merck)

- Tuya

- Whisker

- Wopet

- Xiaomi

The Global Smart Pet Feeder Market was valued at USD 1.4 billion in 2024 and is estimated to grow at a CAGR of 8.8% to reach USD 3.3 billion by 2034. This growth is largely attributed to the surge in global pet ownership, paired with a rise in disposable income and a growing trend of treating pets as family members. Younger pet owners are increasingly integrating smart technologies into pet care routines to ensure convenience, wellness, and proper nutrition. Automated feeders that dispense food in accurate portions on scheduled intervals are gaining popularity, especially those with mobile app connectivity, built-in cameras, and voice functions.

The boom in smart home adoption has further driven interest in connected pet feeding solutions, especially as consumers demand more control and monitoring features from remote locations. E-commerce platforms are significantly enhancing the reach of these products, aiding their penetration into both mature and developing markets. These devices come equipped with anti-jam dispensers, tamper-resistant lids, and secure compartments to protect food and prevent access by other animals, addressing concerns of contamination and overeating. With a strong emphasis on automation, safety, and user-friendly features, smart feeders are fast becoming an essential addition to tech-driven pet households.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.4 Billion |

| Forecast Value | $3.3 Billion |

| CAGR | 8.8% |

The cat feeder segment is anticipated to register a CAGR of 9.2% through 2034, driven by a notable increase in cat ownership and a stronger focus on feline health and nutrition. Cat owners are actively seeking automated solutions that can efficiently portion and preserve both dry and wet food. Devices tailored for cats often incorporate AI-based schedules, sealed storage compartments, and refrigeration features, making them a practical option for those looking to maintain freshness and consistency in feeding routines. These innovations are becoming vital for households where pet owners may be away for extended periods and require reliable, scheduled feeding.

The Wi-Fi-enabled smart feeders dominated the market in 2024 with a share of 61.6%, as they offer advanced remote features through mobile applications. These feeders allow pet parents to manage feeding times, monitor pets via live video, and adjust meal portions from anywhere with internet access. The increase in smartphone usage, enhanced home connectivity, and rising adoption of digital technologies are driving preference for Wi-Fi-based systems over Bluetooth or manual options. These solutions offer seamless integration with broader smart home ecosystems, making them highly appealing to tech-savvy users.

United States Smart Pet Feeder Market generated USD 534.8 million in 2024, up from USD 499.3 million in 2023. This market is forecasted to grow at a CAGR of 8.6% from 2025 through 2034, fueled by widespread pet ownership, strong digital infrastructure, and the rapid uptake of connected pet care products. Consumers in the U.S. are particularly drawn to innovative, automated solutions that offer convenience and enhanced animal care. The region benefits from a mature distribution network, high disposable income, and an advanced veterinary healthcare system, all of which support sustained market growth.

Key companies operating in this Global Smart Pet Feeder Market include Whisker, Dogness, PetSafe Brands, Tuya, Sure Petcare, Wopet, PETLIBRO, Geeni, Xiaomi, HONEYGUARDIAN, Pawbo, Aqara, Catit, Arf Pets, Okos Smart Pet Feeder, and BeardPet. These players continue to push product innovations that cater to growing consumer demands. Leading companies in the smart pet feeder market are investing heavily in product innovation, focusing on enhanced features such as health monitoring, real-time video access, AI-driven feeding algorithms, and voice integration. To strengthen their foothold, brands are prioritizing seamless mobile app interfaces and compatibility with existing smart home ecosystems. Strategic partnerships with e-commerce platforms and retail chains have broadened product reach, while companies are also emphasizing user-centric design and durable build quality. Many players are diversifying their portfolios to include feeders tailored to specific pet needs, like wet food storage or multiple pet households.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Pet type trends

- 2.2.3 Connectivity type trends

- 2.2.4 Application trends

- 2.2.5 Price range trends

- 2.2.6 Distribution channel trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising pet ownership

- 3.2.1.2 Growing technological advancements

- 3.2.1.3 Increasing awareness for pet health & nutrition

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Concerns for technical reliability

- 3.2.2.2 High initial costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expanding e-commerce platform

- 3.2.3.2 Partnerships with pet food brands

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Pet population statistics

- 3.6 Pricing analysis

- 3.7 Technology advancement

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Consumer behavior analysis

- 3.9 Gap analysis

- 3.10 Future market trends

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 North America

- 4.3.2 Europe

- 4.3.3 Asia Pacific

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

Chapter 5 Market Estimates and Forecast, By Pet Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Dogs

- 5.3 Cats

- 5.4 Other pet types

Chapter 6 Market Estimates and Forecast, By Connectivity Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Bluetooth

- 6.3 Wi-Fi

- 6.4 Other connectivity types

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Household

- 7.3 Commercial

Chapter 8 Market Estimates and Forecast, By Price Range, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Low-cost feeder

- 8.3 Mid-range feeder

- 8.4 High-end feeder

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Online channel

- 9.3 Offline channel

- 9.3.1 Physical pet store

- 9.3.2 Physical mass merchant store

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 Japan

- 10.4.2 China

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aqara

- 11.2 Arf Pets

- 11.3 BeardPet

- 11.4 Catit (Rolf C Hagen)

- 11.5 Dogness

- 11.6 Geeni

- 11.7 HONEYGUARDIAN

- 11.8 Okos Smart Pet Feeder

- 11.9 Pawbo

- 11.10 Petlibro

- 11.11 PetSafe Brands

- 11.12 Sure Petcare (Merck)

- 11.13 Tuya

- 11.14 Whisker

- 11.15 Wopet

- 11.16 Xiaomi

智慧宠物技术和互联护理解决方案市场预测至2032年:按产品、宠物类型、互联程度、性别、分销管道、应用、最终用户和地区分類的全球分析智慧宠物餵食器和营养监测市场预测至2032年:全球产品、宠物类型、监测功能、连接方式、技术、最终用户和区域分析全球智慧宠物餵食系统市场:预测至2032年-依产品类型、宠物类型、定价模式、连结方式、通路和区域进行分析物联网宠物行为追踪器市场预测至2032年:按设备类型、连接方式、性别、宠物类型、应用、最终用户和地区分類的全球分析

智慧宠物技术和互联护理解决方案市场预测至2032年:按产品、宠物类型、互联程度、性别、分销管道、应用、最终用户和地区分類的全球分析智慧宠物餵食器和营养监测市场预测至2032年:全球产品、宠物类型、监测功能、连接方式、技术、最终用户和区域分析全球智慧宠物餵食系统市场:预测至2032年-依产品类型、宠物类型、定价模式、连结方式、通路和区域进行分析物联网宠物行为追踪器市场预测至2032年:按设备类型、连接方式、性别、宠物类型、应用、最终用户和地区分類的全球分析 自动智慧宠物餵食器市场:按宠物类型、连接性别、餵食容量、销售管道和最终用户划分 - 全球预测 2025-20322032 年智慧宠物科技市场预测:按产品、宠物类型、连接技术、价格分布范围、分销管道、应用和地区进行的全球分析

自动智慧宠物餵食器市场:按宠物类型、连接性别、餵食容量、销售管道和最终用户划分 - 全球预测 2025-20322032 年智慧宠物科技市场预测:按产品、宠物类型、连接技术、价格分布范围、分销管道、应用和地区进行的全球分析 自动和智慧供料系统的全球市场2032年自主餵食无人机市场预测:按产品类型、组件、餵食方式、有效载荷容量、技术、应用和地区进行的全球分析全球自动和智慧宠物餵食器市场:未来预测(至 2032 年)—按产品、宠物类型、容量、价格分布范围、分销管道、应用和地区进行分析

自动和智慧供料系统的全球市场2032年自主餵食无人机市场预测:按产品类型、组件、餵食方式、有效载荷容量、技术、应用和地区进行的全球分析全球自动和智慧宠物餵食器市场:未来预测(至 2032 年)—按产品、宠物类型、容量、价格分布范围、分销管道、应用和地区进行分析 全球智慧宠物餵食器市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测

全球智慧宠物餵食器市场研究报告-产业分析、规模、份额、成长、趋势及2025年至2033年预测