|

市场调查报告书

商品编码

1797708

建筑规模 3D 列印聚合物长丝市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测Polymer Filaments for Construction-Scale 3D Printing Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

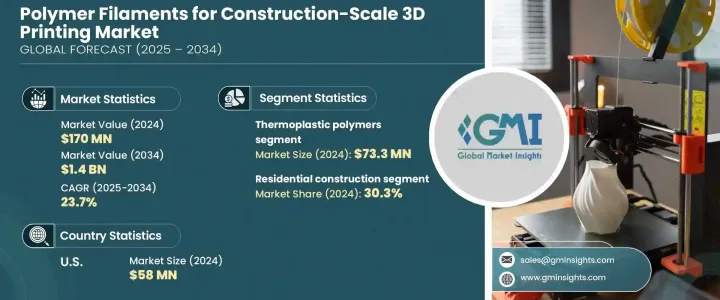

2024年,全球建筑级3D列印聚合物细丝市场价值达1.7亿美元,预计2034年将以23.7%的复合年增长率成长,达到14亿美元。这一快速增长的动力源于对创新和永续建筑方法日益增长的需求。 ABS、PLA和PET等工程热塑性塑胶正在针对从结构部件到整栋建筑的大幅面增材製造应用进行最佳化。 3D列印的多功能性使建筑师和工程师能够创建传统方法无法支援的轻量化复杂结构。这种能力正在促进先进聚合物细丝的快速普及。

政府支持的基础设施发展计画和永续性标准正在加速人们对这项技术的兴趣。 3D列印的自动化功能还能减少材料浪费和人工,使其成为更具成本效益的建筑解决方案。全球对智慧基础设施的重视,尤其是在快速城市化的亚太地区,使得印度、中国和日本等国家在建筑和开发项目中采用高性能3D列印材料方面处于领先地位。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 1.7亿美元 |

| 预测值 | 14亿美元 |

| 复合年增长率 | 23.7% |

2024年,住宅建筑领域占30.3%的市场。该应用因其在解决住房短缺和负担能力方面的作用而日益受到关注。使用聚合物长丝可以快速生产组件,从而缩短施工工期并降低人力成本。这些材料还支持翻新和模组化建筑,使其成为满足市场迫切需求的各种住房解决方案的理想选择。

大型熔融沈积成型 (FDM) 技术因其操作简单且设定成本相对较低,在 2024 年占据了显着份额。其可扩展性使其成为不同层次建筑的理想解决方案—从基础构件到全尺寸住宅或商业建筑。挤压成型设备的普及性也促进了其广泛应用和性能可靠性。

2024年,美国建筑规模3D列印用聚合物线材市场产值达5,800万美元。强劲的市场表现得益于强大的创新生态系统、不断增加的研发投入以及对永续建筑方法的需求。美国企业正在加速开发先进的线材材料,以满足大型建筑的技术需求,同时兼顾环保和成本效益。这项倡议将持续巩固美国在该领域的领先地位。

建筑规模 3D 列印聚合物长丝市场的主要参与者包括 Coex 3D、阿科玛、巴斯夫 SE、西卡 AG、Skanska AB、科思创、MudBots、Mighty Buildings、Tvasta Manufacturing Solutions 和 Manlon Polymers。建筑规模 3D 列印聚合物长丝市场的公司正专注于开发高性能、可回收和耐气候性的材料,以满足建筑业不断变化的需求。研发投资有助于提高长丝成分的强度、耐用性和耐热性。许多製造商正在与建筑科技公司和学术机构合作,以加速创新和商业准备。扩大全球分销和本地化生产能力也使公司能够为快速发展地区的基础设施项目提供服务。策略性合併和技术许可用于获取专有增材製造平台的使用权。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 价格趋势

- 按地区

- 依材料类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计数据

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:按材料类型,2021-2034 年

- 主要趋势

- 热塑性聚合物

- PLA(聚乳酸)和生物基热塑性塑料

- ABS(丙烯腈丁二烯苯乙烯)及工程塑料

- PETG(聚对苯二甲酸乙二醇酯)和特殊聚合物

- 高性能工程塑胶(PEEK、PEI、PEKK)

- 纤维增强复合材料

- 碳纤维增强聚合物(CFRP)

- 玻璃纤维增强聚合物(GFRP)

- 天然纤维增强复合材料

- 连续纤维增强系统

- 可持续和生物基材料

- 生物基聚合物配方

- 回收材料和消费后材料

- 可生物降解和可堆肥的聚合物

- 废弃物衍生材料和循环经济材料

- 特种和功能材料

- 耐火和阻燃聚合物

- 隔热节能材料

- 导电和智慧材料系统

- 多功能混合材料解决方案

- 新兴和先进材料

- 奈米复合材料和增强性能材料

- 形状记忆和响应性聚合物系统

- 自修復和自适应材料技术

- 仿生和自然启发的材料解决方案

第六章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 住宅建筑

- 商业建筑

- 基础设施和土木工程

- 建筑和装饰元素

- 专业和利基应用

第七章:市场估计与预测:按技术,2021-2034 年

- 主要趋势

- 大规模熔融沈积成型(FDM)

- 机器人施工系统

- 连续生产技术

- 新兴和先进技术

第八章:市场估计与预测:依最终用途,2021-2034

- 主要趋势

- 建筑公司和总承包商

- 建筑师和设计专业人士

- 房地产开发商和建筑物业主

- 研究和教育机构

- 政府和公共部门

第九章:市场估计与预测:依设备规模,2021-2034

- 主要趋势

- 大型工业系统

- 中型工业系统

- 紧凑、便携的系统

- 混合和多技术系统

第十章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第 11 章:公司简介

- Arkema

- BASF SE

- Coex 3D

- Covestro

- Manlon Polymers

- Mighty Buildings

- MudBots

- Sika AG

- Skanska AB

- Tvasta Manufacturing Solutions

The Global Polymer Filaments for Construction-Scale 3D Printing Market was valued at USD 170 million in 2024 and is estimated to grow at a CAGR of 23.7% to reach USD 1.4 billion by 2034. This rapid growth is driven by the increasing demand for innovative and sustainable building methods. Engineered thermoplastics such as ABS, PLA, and PET are being optimized for large-format additive manufacturing applications, from structural parts to entire buildings. The versatility of 3D printing enables architects and engineers to create lightweight, complex structures that traditional methods cannot support. This capability is fostering rapid adoption of advanced polymer filaments.

Government-backed infrastructure development initiatives and sustainability standards are accelerating interest in this technology. The automation capabilities of 3D printing also reduce material waste and manual labor, making it a more cost-efficient solution for construction. Global emphasis on smart infrastructure, especially across rapidly urbanizing regions in Asia-Pacific, is positioning countries like India, China, and Japan as leaders in the adoption of high-performance 3D printing materials for building and development projects.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $170 million |

| Forecast Value | $1.4 billion |

| CAGR | 23.7% |

The residential construction segment held a 30.3% share in 2024. This application is gaining traction for its role in addressing housing shortages and affordability. Using polymer filaments, components can be produced quickly, cutting down both construction timelines and labor costs. These materials also support renovation and modular builds, making them ideal for a wide range of housing solutions that respond to immediate market needs.

The large-scale fused deposition modeling (FDM) technology segment held a notable share in 2024 due to its operational simplicity and relatively low setup costs. Its scalable nature makes it an ideal solution for different levels of construction - from foundational components to full-scale residential or commercial buildings. The accessibility of extrusion-based equipment has contributed to its widespread adoption and performance reliability.

U.S. Polymer Filaments for Construction-Scale 3D Printing Market generated USD 58 million in 2024. This strong market presence is driven by a robust innovation ecosystem, increasing R&D efforts, and the demand for sustainable construction methods. Companies in the U.S. are accelerating development of advanced filament materials that meet the technical needs of large-scale construction while aligning with environmental and cost-efficiency objectives. This focus continues to strengthen the country's leadership in the sector.

Key players in Polymer Filaments for Construction-Scale 3D Printing Market include Coex 3D, Arkema, BASF SE, Sika AG, Skanska AB, Covestro, MudBots, Mighty Buildings, Tvasta Manufacturing Solutions, and Manlon Polymers. Companies in the polymer filaments for construction-scale 3D printing market are focusing on developing high-performance, recyclable, and climate-resilient materials to meet the evolving needs of the construction sector. Investments in R&D help improve the strength, durability, and thermal resistance of filament compositions. Many manufacturers are forming collaborations with construction tech firms and academic institutions to speed up innovation and commercial readiness. Expanding global distribution and localized production capabilities also allows companies to serve infrastructure projects in fast-developing regions. Strategic mergers and technology licensing are used to gain access to proprietary additive manufacturing platforms.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Material type trends

- 2.2.2 Application trends

- 2.2.3 Technology trends

- 2.2.4 End use trends

- 2.2.5 Equipment scale trends

- 2.2.6 Regional

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By material type

- 3.9 Future market trends

- 3.10 Technology and Innovation landscape

- 3.10.1 Current technological trends

- 3.10.2 Emerging technologies

- 3.11 Patent Landscape

- 3.12 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.12.1 Major importing countries

- 3.12.2 Major exporting countries

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.14 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material Type, 2021-2034 (USD Million) (Units)

- 5.1 Key trends

- 5.2 Thermoplastic polymers

- 5.2.1 PLA (polylactic acid) and bio-based thermoplastics

- 5.2.2 ABS (acrylonitrile butadiene styrene) and engineering plastics

- 5.2.3 PETG (polyethylene terephthalate glycol) and specialty polymers

- 5.2.4 High-performance engineering plastics (PEEK, PEI, PEKK)

- 5.3 Fiber-reinforced composites

- 5.3.1 Carbon fiber reinforced polymers (CFRP)

- 5.3.2 Glass fiber reinforced polymers (GFRP)

- 5.3.3 Natural fiber reinforced composites

- 5.3.4 Continuous fiber reinforcement systems

- 5.4 Sustainable and bio-based materials

- 5.4.1 Bio-based polymer formulations

- 5.4.2 Recycled content and post-consumer materials

- 5.4.3 Biodegradable and compostable polymers

- 5.4.4 Waste-derived and circular economy materials

- 5.5 Specialty and functional materials

- 5.5.1 Fire-resistant and flame-retardant polymers

- 5.5.2 Thermal insulation and energy-efficient materials

- 5.5.3 Conductive and smart material systems

- 5.5.4 Multi-functional and hybrid material solutions

- 5.6 Emerging and advanced materials

- 5.6.1 Nanocomposite and enhanced performance materials

- 5.6.2 Shape memory and responsive polymer systems

- 5.6.3 Self-healing and adaptive material technologies

- 5.6.4 Biomimetic and nature-inspired material solutions

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Million) (Units)

- 6.1 Key trends

- 6.2 Residential construction

- 6.3 Commercial construction

- 6.4 Infrastructure and civil engineering

- 6.5 Architectural and decorative elements

- 6.6 Specialty and niche applications

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Million) (Units)

- 7.1 Key trends

- 7.2 Large-scale fused deposition modelling (FDM)

- 7.3 Robotic construction systems

- 7.4 Continuous manufacturing technologies

- 7.5 Emerging and advanced technologies

Chapter 8 Market Estimates and Forecast, By End Use, 2021-2034 (USD Million) (Units)

- 8.1 Key trends

- 8.2 Construction companies and general contractors

- 8.3 Architects and design professionals

- 8.4 Real estate developers and building owners

- 8.5 Research and educational institutions

- 8.6 Government and public sector

Chapter 9 Market Estimates and Forecast, By Equipment Scale, 2021-2034 (USD Million) (Units)

- 9.1 Key trends

- 9.2 Large-scale industrial systems

- 9.3 Medium- scale industrial systems

- 9.4 Compact and portable systems

- 9.5 Hybrid and multi-technology systems

Chapter 10 Market Estimates and Forecast, By Region, 2021-2034 (USD Million) (Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Arkema

- 11.2 BASF SE

- 11.3 Coex 3D

- 11.4 Covestro

- 11.5 Manlon Polymers

- 11.6 Mighty Buildings

- 11.7 MudBots

- 11.8 Sika AG

- 11.9 Skanska AB

- 11.10 Tvasta Manufacturing Solutions

航太3D列印市场:依印表机类型、材料、技术、应用和最终用途产业划分-2026-2032年全球市场预测

航太3D列印市场:依印表机类型、材料、技术、应用和最终用途产业划分-2026-2032年全球市场预测 2026年全球航太3D列印市场报告

2026年全球航太3D列印市场报告 航太领域3D列印市场规模、份额、成长率及全球产业分析:按类型、应用和地区分類的洞察,2026-2034年预测航太3D列印市场规模、份额、趋势和成长分析报告(2026-2034年)

航太领域3D列印市场规模、份额、成长率及全球产业分析:按类型、应用和地区分類的洞察,2026-2034年预测航太3D列印市场规模、份额、趋势和成长分析报告(2026-2034年) 全球国防3D列印市场(2026-2036)

全球国防3D列印市场(2026-2036) 航太领域3D列印-全球产业规模、份额、趋势、机会及预测(按应用、材料、印表机技术、地区和竞争格局划分,2021-2031年)

航太领域3D列印-全球产业规模、份额、趋势、机会及预测(按应用、材料、印表机技术、地区和竞争格局划分,2021-2031年) 航太3D列印市场规模、份额和成长分析(按产品、技术、平台、最终产品、最终用户、应用和地区划分)-产业预测(2026-2033年)

航太3D列印市场规模、份额和成长分析(按产品、技术、平台、最终产品、最终用户、应用和地区划分)-产业预测(2026-2033年) 不銹钢填充聚合物长丝市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)金属填充聚合物长丝市场规模、份额和趋势分析报告 - 按金属、最终用途、地区和细分市场预测:2025-2033年航太和国防领域的 3D 列印:全球预测(2025-2030 年)

不銹钢填充聚合物长丝市场规模、份额和趋势分析报告:按类型、应用、地区和细分市场预测(2025-2033 年)金属填充聚合物长丝市场规模、份额和趋势分析报告 - 按金属、最终用途、地区和细分市场预测:2025-2033年航太和国防领域的 3D 列印:全球预测(2025-2030 年)