|

市场调查报告书

商品编码

1797749

电池黏合剂材料市场机会、成长动力、产业趋势分析及2025-2034年预测Battery Binder Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

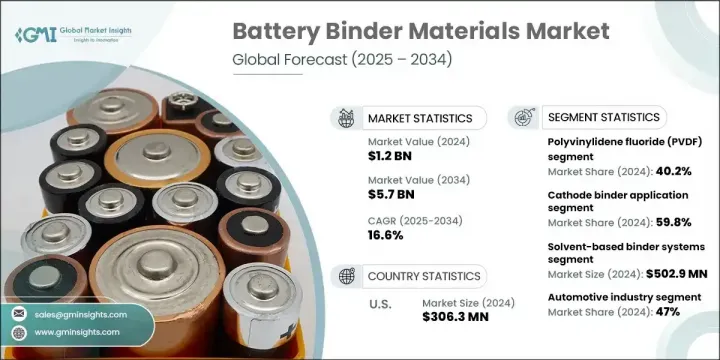

2024年,全球电池黏合剂材料市场规模达12亿美元,预计到2034年将以16.6%的复合年增长率成长,达到57亿美元。这一成长趋势主要受电动车、行动电子设备和再生能源储存系统等多个高成长领域对锂离子电池日益增长的需求的影响。电池黏合剂——用于将活性颗粒固定到电极集流体上的专用聚合物——在设计更高效率、更大容量和更长使用寿命的电池方面变得越来越重要。它们作为结构性“黏合剂”,确保了电池的黏合性和耐用性,直接影响电池的机械完整性和循环性能。

随着穿戴式装置和智慧型手机等现代消费性设备中高能量密度、小型电池设计的不断扩展,黏合剂材料配方的创新也加速了。随着大型电池储能係统融入再生能源基础设施,对长效且热稳定的黏合剂的需求急剧增长。製造商正致力于生产下一代丙烯酸基黏合剂,以增强电极的黏结力、机械强度和柔韧性。对轻量化组件和环境相容性的日益重视持续引领产品开发,而永续材料的日益普及也进一步提升了先进製造业的需求。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 12亿美元 |

| 预测值 | 57亿美元 |

| 复合年增长率 | 16.6% |

2024年,正极黏合剂市场占有59.8%的份额,预计到2034年复合年增长率为16.5%。这些黏合剂对于在严格的充放电循环中保持正极的耐久性和性能至关重要。最常用的材料之一是PVDF(聚偏氟乙烯),它以其强大的耐化学性和耐热性、可靠的黏合性以及与多种正极材料的兼容性而闻名。正极黏合剂在确保活性材料与集流体表面有效连接方面发挥关键作用,有助于提高电池的稳定性和输出效率。

2024年,溶剂型黏合剂体系市场规模达5.029亿美元,预计到2034年将以16.8%的复合年增长率成长。过去,使用NMP的PVDF基溶剂型黏合剂因其优异的附着力、耐化学性和性能而在电池製造领域备受青睐。然而,由于欧洲和北美等主要地区日益严格的环境和安全法规,这些材料如今面临更严格的限制。虽然溶剂型系统仍占主导地位,但向水性和更环保的黏合剂技术的转变正在重塑市场格局,促使製造商在不影响性能的情况下寻求更清洁、更合规的替代品。

2024年,美国电池黏合剂材料市场规模达3.063亿美元,预计2034年复合年增长率将达到13.7%。由于电动车的强劲发展、对储能的大量投资以及根深蒂固的製造业生态系统,美国将继续蓬勃发展,成为电池黏合剂创新的中心枢纽。联邦政府对国内电池供应链的大力支持,加上对先进黏合剂生产的财政激励,巩固了美国在这个快速发展的市场中的立足点。策略性资本注入也正在提升SBR和PVDF等下一代黏合剂材料的生产能力,进一步推动本土发展。

全球电池黏合剂材料市场的主要领导者包括瑞翁株式会社、索尔维公司、科慕公司、中化蓝天、东岳集团、阿科玛公司、吴羽株式会社、上海三爱富新材料、JSR株式会社和山东华夏神舟新材料。这些公司正在大力投资研发,以开发符合全球永续发展目标的环保高性能黏合配方。与电池製造商和原始设备製造商的合作,使得新材料能够更快地融入下一代电池系统。各公司也在扩大产能并成立合资企业,以增强其区域影响力。为了因应不断变化的监管环境,市场领导者正在从传统的溶剂型体系转向水性体系,同时注重製造过程中的可扩展性和能源效率。

目录

第一章:方法论与范围

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商格局

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 电动车市场扩张

- 储能係统部署

- 消费性电子产品需求成长

- 电池性能提升要求

- 产业陷阱与挑战

- 材料成本高且价格波动

- 环境和安全法规

- 技术性能限制

- 供应链集中风险

- 市场机会

- 下一代电池技术

- 永续和生物基黏合剂的开发

- 硅阳极技术采用

- 新兴市场渗透

- 成长动力

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 依产品类型

- 未来市场趋势

- 技术和创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)

(註:仅提供重点国家的贸易统计数据

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考虑

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测:依产品类型,2021-2034

- 主要趋势

- 聚偏氟乙烯(PVDF)

- 羧甲基纤维素(CMC)

- 丁苯橡胶(SBR)

- 聚丙烯酸(PAA)

- 其他特殊黏合剂

第六章:市场估计与预测:按应用,2021-2034

- 主要趋势

- 阴极黏合剂应用

- NCM阴极系统

- NCA阴极系统

- LFP阴极系统

- 高压正极材料

- 阳极黏合剂应用

- 石墨阳极系统

- 硅基阳极系统

- 钛酸锂(LTO)体系

- 下一代阳极材料

第七章:市场估计与预测:按技术,2021-2034 年

- 主要趋势

- 溶剂型黏合剂体系

- 传统 PVDF 系统

- 水性黏合剂体系

- CMC/SBR 组合

- 混合黏合剂体系

- 多组分配方

- 下一代技术

- 固态电池黏合剂

- 导电黏合剂网络

- 自修復材料

第八章:市场估计与预测:按最终用途产业,2021-2034 年

- 主要趋势

- 汽车产业

- 电动乘用车

- 电动商用车

- 油电混合车

- 消费性电子产品

- 智慧型手机和平板电脑

- 笔记型电脑和便携式设备

- 穿戴式电子产品

- 游戏和娱乐设备

- 储能係统

- 电网规模储能

- 住宅储能

- 商业和工业存储

- 再生能源整合

- 工业应用

- 物料搬运设备

- 备用电源系统

- 电信基础设施

- 医疗保健设备

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Arkema SA

- Chemours Company

- Dongyue Group

- JSR Corporation

- Kureha Corporation

- Shandong Huaxia Shenzhou New Material

- Shanghai 3F New Materials

- Sinochem Lantian

- Solvay SA

- Zeon Corporation

The Global Battery Binder Materials Market was valued at USD 1.2 billion in 2024 and is estimated to grow at a CAGR of 16.6% to reach USD 5.7 billion by 2034. This upward trend is largely influenced by the escalating demand for lithium-ion batteries across a variety of high-growth sectors such as electric vehicles, mobile electronics, and renewable energy storage systems. Battery binders-specialized polymers used to secure active particles to electrode current collectors-are becoming increasingly vital in designing batteries with greater efficiency, higher capacity, and extended lifespans. Their role as structural "adhesives" ensures cohesive binding and durability, directly impacting the battery's mechanical integrity and cycle performance.

The expansion of energy-dense, compact battery designs for modern consumer devices like wearables and smartphones is accelerating innovation in binder material formulations. With the integration of large-scale battery storage systems into renewable energy infrastructure, the need for long-lasting and thermally stable binders has grown sharply. Manufacturers are focusing on producing next-generation acrylic-based binders to boost electrode cohesion, enhance mechanical strength, and improve flexibility. Rising emphasis on lightweight components and environmental compatibility continues to steer product development, while growing adoption of sustainable materials further elevates demand in advanced manufacturing sectors.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.2 Billion |

| Forecast Value | $5.7 Billion |

| CAGR | 16.6% |

The cathode binders segment held 59.8% share in 2024, with projected growth at a CAGR of 16.5% through 2034. These binders are essential in maintaining cathode durability and performance under rigorous charge-discharge cycles. Among the most used materials is PVDF (polyvinylidene fluoride), known for its robust chemical and thermal resistance, reliable adhesion, and compatibility with a wide range of cathode materials. Cathode binders play a critical role in ensuring that the active materials remain effectively connected to the collector surface, thereby contributing to battery stability and output efficiency.

In 2024, the solvent-based binder systems segment was valued at USD 502.9 million and is projected to grow at a CAGR of 16.8% through 2034. Historically, PVDF-based solvent binders using NMP were favored in battery manufacturing due to their ability to offer superior adhesion, chemical resilience, and performance. However, these materials are now facing tighter restrictions due to increasing environmental and safety regulations in key regions like Europe and North America. While solvent-based systems still dominate, the shift toward water-based and more eco-friendly binder technologies is reshaping the landscape, pushing manufacturers toward cleaner and more compliant alternatives without compromising performance.

United States Battery Binder Materials Market generated USD 306.3 million in 2024, with expected growth at a CAGR of 13.7% through 2034. The nation continues to thrive as a central hub for battery binder innovation, propelled by its robust electric vehicle rollout, significant investments in energy storage, and deep-rooted manufacturing ecosystem. Extensive federal support for domestic battery supply chains, combined with financial incentives for advanced adhesive production, has strengthened the U.S. foothold in this fast-evolving market. Strategic capital infusion is also advancing production capabilities for next-gen binder materials like SBR and PVDF, further driving local development.

Key companies leading the Global Battery Binder Materials Market include Zeon Corporation, Solvay S.A., Chemours Company, Sinochem Lantian, Dongyue Group, Arkema S.A., Kureha Corporation, Shanghai 3F New Materials, JSR Corporation, and Shandong Huaxia Shenzhou New Material. They are investing significantly in R&D to develop environmentally friendly and high-performance binder formulations that meet global sustainability goals. Collaborations with battery cell manufacturers and OEMs are enabling faster integration of new materials into next-generation battery systems. Companies are also expanding production capacity and entering joint ventures to strengthen their regional reach. To comply with shifting regulatory landscapes, market leaders are transitioning from traditional solvent-based systems to water-based alternatives while focusing on scalability and energy efficiency during manufacturing.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Application

- 2.2.4 Technology

- 2.2.5 End use industry

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Electric vehicle market expansion

- 3.2.1.2 Energy storage system deployment

- 3.2.1.3 Consumer electronics demand growth

- 3.2.1.4 Battery performance enhancement requirements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High material costs and price volatility

- 3.2.2.2 Environmental and safety regulations

- 3.2.2.3 Technical performance limitations

- 3.2.2.4 Supply chain concentration risks

- 3.2.3 Market opportunities

- 3.2.3.1 Next-generation battery technologies

- 3.2.3.2 Sustainable and bio-based binder development

- 3.2.3.3 Silicon anode technology adoption

- 3.2.3.4 Emerging market penetration

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product type

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.13 Carbon footprint consideration

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Polyvinylidene Fluoride (PVDF)

- 5.3 Carboxymethyl Cellulose (CMC)

- 5.4 Styrene-Butadiene Rubber (SBR)

- 5.5 Polyacrylic Acid (PAA)

- 5.6 Other Specialty Binders

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cathode binder applications

- 6.2.1 NCM cathode systems

- 6.2.2 NCA cathode systems

- 6.2.3 LFP cathode systems

- 6.2.4 High-voltage Cathode Materials

- 6.3 Anode binder applications

- 6.3.1 Graphite anode systems

- 6.3.2 Silicon-based anode systems

- 6.3.3 Lithium titanate oxide (LTO) systems

- 6.3.4 Next-generation anode materials

Chapter 7 Market Estimates and Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Solvent-based binder systems

- 7.2.1 Traditional PVDF systems

- 7.3 Water-based binder systems

- 7.3.1 CMC/SBR combinations

- 7.4 Hybrid binder systems

- 7.4.1 Multi-component formulations

- 7.5 Next-generation technologies

- 7.5.1 Solid-state battery binders

- 7.5.2 Conductive binder networks

- 7.5.3 Self-healing materials

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive industry

- 8.2.1 Electric passenger vehicles

- 8.2.2 Electric commercial vehicles

- 8.2.3 Hybrid electric vehicles

- 8.3 Consumer electronics

- 8.3.1 Smartphones and tablets

- 8.3.2 Laptops and portable devices

- 8.3.3 Wearable electronics

- 8.3.4 Gaming and entertainment devices

- 8.4 Energy storage systems

- 8.4.1 Grid-scale energy storage

- 8.4.2 Residential energy storage

- 8.4.3 Commercial and industrial storage

- 8.4.4 Renewable energy integration

- 8.5 Industrial applications

- 8.5.1 Material handling equipment

- 8.5.2 Backup power systems

- 8.5.3 Telecommunications infrastructure

- 8.5.4 Medical and healthcare devices

Chapter 9 Market Estimates and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East and Africa

Chapter 10 Company Profiles

- 10.1 Arkema S.A.

- 10.2 Chemours Company

- 10.3 Dongyue Group

- 10.4 JSR Corporation

- 10.5 Kureha Corporation

- 10.6 Shandong Huaxia Shenzhou New Material

- 10.7 Shanghai 3F New Materials

- 10.8 Sinochem Lantian

- 10.9 Solvay S.A.

- 10.10 Zeon Corporation

PAA阳极黏结剂-2026-2032年全球市占率及排名、总收入及需求预测

PAA阳极黏结剂-2026-2032年全球市占率及排名、总收入及需求预测 电池黏合剂市场:按类型、功能、製程类型、溶剂製程、应用和最终用户划分-2026-2032年全球市场预测锂电池正极黏合剂市场:按黏合剂类型、电池化学成分、应用、製造方法和终端用户产业划分-全球预测,2026-2032年

电池黏合剂市场:按类型、功能、製程类型、溶剂製程、应用和最终用户划分-2026-2032年全球市场预测锂电池正极黏合剂市场:按黏合剂类型、电池化学成分、应用、製造方法和终端用户产业划分-全球预测,2026-2032年 锂离子电池黏合剂市场分析与预测(至2035年):类型、产品、应用、材料类型、技术、组件、最终用户、形式、製程、功能锂离子电池黏合剂市场:按黏合剂类型、电池规格和应用分類的全球预测,2026-2032年

锂离子电池黏合剂市场分析与预测(至2035年):类型、产品、应用、材料类型、技术、组件、最终用户、形式、製程、功能锂离子电池黏合剂市场:按黏合剂类型、电池规格和应用分類的全球预测,2026-2032年 用于锂电池黏合剂的氢化丁腈橡胶 (HNBR) - 全球市场份额和排名、总收入和需求预测(2025-2031 年)用于锂离子电池的SBR黏合剂 - 全球市场份额和排名、总收入和需求预测(2025-2031年)

用于锂电池黏合剂的氢化丁腈橡胶 (HNBR) - 全球市场份额和排名、总收入和需求预测(2025-2031 年)用于锂离子电池的SBR黏合剂 - 全球市场份额和排名、总收入和需求预测(2025-2031年) 全球电池黏合剂市场全球锂离子电池黏合剂市场全球阳极黏合剂市场

全球电池黏合剂市场全球锂离子电池黏合剂市场全球阳极黏合剂市场