|

市场调查报告书

商品编码

1797766

胶合木市场机会、成长动力、产业趋势分析及2025-2034年预测Glulam Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

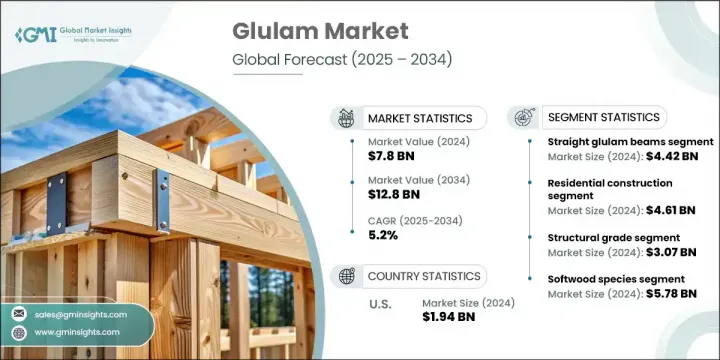

2024年,全球胶合木市场规模达78亿美元,预计到2034年将以5.2%的复合年增长率成长,达到128亿美元。市场发展势头强劲,主要得益于人们普遍转向永续建筑实践。随着公共和私营部门都专注于降低排放和整合可再生建筑材料,采用可持续来源木材製成的胶合木已成为钢材和混凝土等传统材料的可行替代品。其低能耗和低碳足迹的特性与全球气候目标高度契合。随着大规模木材技术在多层建筑中的兴起,胶合木因其优异的结构性能、大跨度以及易于异地预製等特点而日益受到青睐。使用胶合木可以加快工程进度,并减少施工现场的环境破坏。

此外,随着开发商寻求透过高性能、低影响的材料来满足环保标准,人们对绿色建筑认证日益增长的兴趣也增强了胶合木的吸引力。 LEED、BREEAM 和 WELL 等认证日益影响着公共和私人建筑项目的设计和材料选择。胶合木的可再生特性,加上其高强度轻质和低碳排放,使其成为帮助计画达到这些严格环保标准的理想材料。建筑师和建筑商青睐胶合木,不仅因为它的可持续性,还因为它兼具美感和设计灵活性,这与亲生物和现代建筑的潮流相契合。

| 市场范围 | |

|---|---|

| 起始年份 | 2024 |

| 预测年份 | 2025-2034 |

| 起始值 | 78亿美元 |

| 预测值 | 128亿美元 |

| 复合年增长率 | 5.2% |

直胶合梁市场在2024年创造了44.2亿美元的产值,预计2025年至2034年的复合年增长率将达到4.6%。与其他结构材料相比,直胶合梁凭藉其强度高、适应性强且价格实惠的优势,仍是许多建筑项目的首选材料。其设计简洁,且与常见建筑技术相容,使其成为住宅和商业建筑中地板、墙体和屋顶结构的理想选择。预製建筑方法的持续普及也刺激了对直胶合樑的需求,因为它们为现代建筑提供了一种经济高效且可持续的替代方案。

住宅建筑领域在2024年创造了46.1亿美元的市场规模,占市场份额的59.05%,预计到2034年的复合年增长率为4.6%。这种主导地位主要归因于对绿色住宅解决方案和木质建筑系统日益增长的需求。胶合木因其耐用性、自然美观、易于安装和减少环境影响而越来越受到家庭的青睐。随着越来越多的消费者和开发商青睐环保的居住空间,胶合木在屋顶支撑、地板系统和装饰樑方面继续发挥至关重要的作用。随着城市扩张和永续城镇化成为重中之重,预计该应用领域将继续成为市场成长的核心力量。

2024年,美国胶合木市场规模达19.4亿美元,预计2025年至2034年期间的复合年增长率为4.9%。北美市场的发展动能与中高层建筑中大规模木造建筑的快速崛起息息相关。由于有利于替代建筑材料的法规变化(例如《国际建筑规范》(IBC)的更新),该地区的建筑业越来越多地采用胶合木。美国和加拿大越来越注重环保的建筑实践,这促进了胶合木在商业和机构项目中的作用不断扩大,其结构强度、美观度和可持续性等优势在这些项目中尤为明显。

塑造胶合木市场竞争格局的关键公司包括 Mayr-Melnhof Holz Holding AG、Boise Cascade Company、Structurlam Mass Timber Corporation、Stora Enso Oyj 和 Binderholz GmbH。胶合木产业的公司正专注于策略扩张和创新,以巩固其市场地位。他们正在投资现代化生产线,以提高产量并优化产品质量,尤其是针对更大、更复杂的结构部件。主要参与者正在加强其全球供应链,并与建筑公司建立合资企业或合作伙伴关係,以推广胶合木在备受瞩目的永续建筑专案中的应用。此外,製造商正在强调产品认证和符合绿色建筑标准,以吸引具有环保意识的开发商。针对预製和模组化建筑的客製化解决方案也越来越受欢迎。

目录

第一章:方法论

- 市场范围和定义

- 研究设计

- 研究方法

- 资料收集方法

- 资料探勘来源

- 全球的

- 地区/国家

- 基础估算与计算

- 基准年计算

- 市场评估的主要趋势

- 初步研究和验证

- 主要来源

- 预测模型

- 研究假设和局限性

第二章:执行摘要

第三章:行业洞察

- 产业生态系统分析

- 供应商概况

- 利润率

- 每个阶段的增值

- 影响价值链的因素

- 中断

- 产业衝击力

- 成长动力

- 产业陷阱与挑战

- 市场机会

- 成长潜力分析

- 监管格局

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- 中东和非洲

- 波特的分析

- PESTEL分析

- 价格趋势

- 按地区

- 按产品

- 未来市场趋势

- 科技与创新格局

- 当前的技术趋势

- 新兴技术

- 专利态势

- 贸易统计(HS编码)(註:仅提供重点国家的贸易统计资料)

- 主要进口国

- 主要出口国

- 永续性和环境方面

- 永续实践

- 减少废弃物的策略

- 生产中的能源效率

- 环保倡议

- 碳足迹考量

第四章:竞争格局

- 介绍

- 公司市占率分析

- 按地区

- 北美洲

- 欧洲

- 亚太地区

- 拉丁美洲

- MEA

- 按地区

- 公司矩阵分析

- 主要市场参与者的竞争分析

- 竞争定位矩阵

- 关键进展

- 併购

- 伙伴关係与合作

- 新产品发布

- 扩张计划

第五章:市场估计与预测、产品类型,2021-2034

- 主要趋势

- 直胶合樑

- 弯曲和拱形胶合木

- 胶合木柱和立柱

- 胶合木桁架和框架

- 合板和地板

- 特殊和客製化产品

第六章:市场估计与预测:依等级,2021-2034

- 主要趋势

- 结构等级

- 外观等级

- 工业级

- 特种和高性能等级

第七章:市场估计与预测:依木材种类,2021-2034

- 主要趋势

- 软木树种

- 花旗松

- 南方松

- 云杉-松树-冷杉(SPF)

- 西部铁杉与雪松

- 硬木树种

- 橡木和枫木

- 白蜡木和山核桃木

- 珍稀特种硬木

- 混合物种组合

第 8 章:市场估计与预测:按应用,2021 年至 2034 年

- 主要趋势

- 住宅建筑

- 单户住宅

- 多户住宅及公寓大楼

- 客製化豪华住宅

- 翻新和改造

- 商业建筑

- 办公大楼

- 零售和购物中心

- 旅馆及旅馆建设

- 混合用途开发

- 工业和仓库建设

- 製造工厂

- 配送和物流中心

- 农业和仓储建筑

- 大跨距结构要求

- 机构及公共建筑

- 教育设施建设

- 医疗保健和医院建筑

- 政府及市政项目

- 宗教和社区中心

- 基础设施和交通

- 桥樑建设

- 行人和自行车基础设施

- 交通车站及月台

- 海洋和水岸结构

- 专业和利基应用

- 体育和娱乐设施

- 娱乐和文化场所

- 临时和活动结构

- 修復和历史保护

第九章:市场估计与预测:按地区,2021-2034

- 主要趋势

- 北美洲

- 我们

- 加拿大

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 欧洲其他地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 拉丁美洲

- 巴西

- 墨西哥

- 阿根廷

- 拉丁美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 阿联酋

- 中东和非洲其他地区

第十章:公司简介

- Binderholz GmbH

- Boise Cascade Company

- Calvert Co. Inc.

- Element5 Co.

- Glulam Ltd (UK)

- Hasslacher Norica Timber

- Hundegger

- Martinsons Tra AB

- Mayr-Melnhof Holz Holding AG

- Rosboro

- Schilliger Holz AG

- Setra Group AB

- Stora Enso Oyj

- StructureCraft

- Structurlam Mass Timber Corporation

- Weinig Group

- Western Archrib

The Global Glulam Market was valued at USD 7.8 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 12.8 billion by 2034. Market momentum is being driven by a widespread shift toward sustainable construction practices. As both private and public sectors focus on lowering emissions and integrating renewable building materials, glulam-engineered from sustainably sourced timber-has emerged as a viable replacement for conventional materials like steel and concrete. Its low embodied energy and reduced carbon footprint align well with global climate targets. With the rise of mass timber techniques in multi-story structures, glulam is increasingly favored for its structural performance, long-span capabilities, and suitability for offsite prefabrication. Its use accelerates project timelines and reduces environmental disruption at job sites.

Additionally, growing interest in green building certifications is amplifying glulam's appeal as developers seek to meet environmental standards through high-performance, low-impact materials. Certifications such as LEED, BREEAM, and WELL increasingly influence design and material choices in both public and private construction projects. Glulam's renewable nature, coupled with its strength-to-weight ratio and low embodied carbon, makes it an ideal material to help projects achieve these rigorous environmental benchmarks. Architects and builders favor glulam not only for its sustainability but also for its aesthetic warmth and design flexibility, which aligns with biophilic and modern architectural trends.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.8 Billion |

| Forecast Value | $12.8 Billion |

| CAGR | 5.2% |

The straight glulam beams segment generated USD 4.42 billion in 2024 and is projected to grow at a CAGR of 4.6% from 2025 to 2034. These beams remain the go-to option in many construction projects due to their strength, adaptability, and affordability compared to other structural materials. Their design simplicity and compatibility with common building techniques make them ideal for widespread application in floors, walls, and roof structures in both residential and commercial settings. The continued popularity of prefab construction methods also fuels demand for straight glulam beams, as they offer a cost-effective and sustainable alternative in modern architecture.

The residential construction segment generated USD 4.61 billion and a 59.05% share in 2024, with an expected CAGR of 4.6% through 2034. This dominance is primarily attributed to the rising demand for green housing solutions and timber-based building systems. Glulam is increasingly preferred in homes due to its durability, natural aesthetic, ease of installation, and reduced environmental impact. As more consumers and developers embrace eco-friendly living spaces, glulam continues to play a crucial role in roof supports, flooring systems, and decorative beams. With cities expanding and sustainable urbanization becoming a top priority, this application segment is expected to remain a central force in market growth.

United States Glulam Market was valued at USD 1.94 billion in 2024 and is projected to grow at a CAGR of 4.9% between 2025 and 2034. North America's market momentum is tied to the rapid rise of mass timber construction in mid-rise and tall buildings. The region's building industry is increasingly adopting glulam due to changes in regulations that favor alternative construction materials, such as updates to the International Building Code (IBC). The trend toward more eco-conscious building practices in the U.S. and Canada has contributed to glulam's expanding role in commercial and institutional projects alike, where its structural strength, aesthetic appeal, and sustainability credentials offer clear advantages.

Key companies shaping the competitive landscape in the Glulam Market include Mayr-Melnhof Holz Holding AG, Boise Cascade Company, Structurlam Mass Timber Corporation, Stora Enso Oyj, and Binderholz GmbH. Companies in the glulam industry are focusing on strategic expansion and innovation to solidify their market presence. Investments are being made in modern production lines to boost output and optimize product quality, especially for larger and more complex structural components. Key players are strengthening their global supply chains and entering joint ventures or partnerships with construction firms to promote glulam use in high-profile sustainable building projects. Additionally, manufacturers are emphasizing product certifications and compliance with green building standards to appeal to eco-conscious developers. Customized solutions for prefabricated and modular buildings are also gaining traction.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product Type

- 2.2.3 Grade

- 2.2.4 Wood Species

- 2.2.5 Application

- 2.3 TAM Analysis, 2021-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Straight glulam beams

- 5.3 Curved and arched glulam

- 5.4 Glulam columns and posts

- 5.5 Glulam trusses and frames

- 5.6 Glulam panels and decking

- 5.7 Specialty and custom products

Chapter 6 Market Estimates & Forecast, By Grade, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Structural grade

- 6.3 Appearance grade

- 6.4 Industrial grade

- 6.5 Specialty and high-performance grades

Chapter 7 Market Estimates & Forecast, By Wood Species, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Softwood species

- 7.2.1 Douglas fir

- 7.2.2 Southern pine

- 7.2.3 Spruce-pine-fir (SPF)

- 7.2.4 Western hemlock and cedar

- 7.3 Hardwood species

- 7.3.1 Oak and maple

- 7.3.2 Ash and hickory

- 7.3.3 Exotic and specialty hardwoods

- 7.3.4 Mixed species combinations

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Residential construction

- 8.2.1 Single-family home

- 8.2.2 Multi-family and apartment buildings

- 8.2.3 Custom and luxury home

- 8.2.4 Renovation and remodeling

- 8.3 Commercial construction

- 8.3.1 Office building

- 8.3.2 Retail and shopping centers

- 8.3.3 Hospitality and hotel construction

- 8.3.4 Mixed-use development

- 8.4 Industrial and warehouse construction

- 8.4.1 Manufacturing facility

- 8.4.2 Distribution and logistics centers

- 8.4.3 Agricultural and storage buildings

- 8.4.4 Large span structure requirements

- 8.5 Institutional and public buildings

- 8.5.1 Educational facility construction

- 8.5.2 Healthcare and hospital buildings

- 8.5.3 Government and municipal projects

- 8.5.4 Religious and community centers

- 8.6 Infrastructure and transportation

- 8.6.1 Bridge construction

- 8.6.2 Pedestrian and cycling infrastructure

- 8.6.3 Transit station and platform

- 8.6.4 Marine and waterfront structures

- 8.7 Specialty and niche applications

- 8.7.1 Sports and recreation facilities

- 8.7.2 Entertainment and cultural venues

- 8.7.3 Temporary and event structures

- 8.7.4 Restoration and historic preservation

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Binderholz GmbH

- 10.2 Boise Cascade Company

- 10.3 Calvert Co. Inc.

- 10.4 Element5 Co.

- 10.5 Glulam Ltd (UK)

- 10.6 Hasslacher Norica Timber

- 10.7 Hundegger

- 10.8 Martinsons Tra AB

- 10.9 Mayr-Melnhof Holz Holding AG

- 10.10 Rosboro

- 10.11 Schilliger Holz AG

- 10.12 Setra Group AB

- 10.13 Stora Enso Oyj

- 10.14 StructureCraft

- 10.15 Structurlam Mass Timber Corporation

- 10.16 Weinig Group

- 10.17 Western Archrib

交叉复合板市场:按产品类型、材质等级、应用、最终用途和分销管道划分-2026年至2032年全球预测

交叉复合板市场:按产品类型、材质等级、应用、最终用途和分销管道划分-2026年至2032年全球预测 异形层压交叉层压板(CLT)市场规模、份额和成长分析:按产品类型、应用、最终用途产业、厚度和地区划分-2026-2033年产业预测

异形层压交叉层压板(CLT)市场规模、份额和成长分析:按产品类型、应用、最终用途产业、厚度和地区划分-2026-2033年产业预测 全球交叉层压木材(CLT)市场规模、份额、趋势和成长分析报告(2026-2034年)

全球交叉层压木材(CLT)市场规模、份额、趋势和成长分析报告(2026-2034年) 交叉层压材料市场规模、份额、趋势和预测(按应用、产品类型、元件类型、原材料类型、粘合方法、面板层数、黏合剂类型、压制类型、地板等级、应用类型和地区划分),2026-2034年

交叉层压材料市场规模、份额、趋势和预测(按应用、产品类型、元件类型、原材料类型、粘合方法、面板层数、黏合剂类型、压制类型、地板等级、应用类型和地区划分),2026-2034年 2026年全球交叉层积木材市场报告

2026年全球交叉层积木材市场报告 交叉层压木材市场-全球产业规模、份额、趋势、机会和预测:连接技术、应用、层类型、结构类型、地区和竞争格局,2021-2031年CLT酸市场按产品等级、产品形式、应用和分销管道划分-2026-2032年全球预测住宅交叉层压木材市场按产品、建筑类型、厚度、住宅类型和最终用户划分-2026年至2032年全球预测商用交叉层压木材(CLT)市场按板材类型、板材厚度、分销管道、最终用途和应用划分-2026年至2032年全球预测

交叉层压木材市场-全球产业规模、份额、趋势、机会和预测:连接技术、应用、层类型、结构类型、地区和竞争格局,2021-2031年CLT酸市场按产品等级、产品形式、应用和分销管道划分-2026-2032年全球预测住宅交叉层压木材市场按产品、建筑类型、厚度、住宅类型和最终用户划分-2026年至2032年全球预测商用交叉层压木材(CLT)市场按板材类型、板材厚度、分销管道、最终用途和应用划分-2026年至2032年全球预测 交叉层压木材(CLT)市场规模、份额和成长分析(按类型、应用、产业和地区划分)-2026-2033年产业预测

交叉层压木材(CLT)市场规模、份额和成长分析(按类型、应用、产业和地区划分)-2026-2033年产业预测